Aman Singhal/AI-Generated Image

Aman Singhal/AI-Generated Image

Summary: Your 20s give you a rare investing edge: time. But using it well depends less on theory and more on behaviour. This article looks at how young investors can start smartly without setting themselves up to quit midway.

Your first salary feels like freedom. Better phones. Better trips. More nights out. And somewhere in the background, a thought: I should probably start investing. Most people in their 20s don’t struggle with the idea of investing. They struggle with how to begin. There’s advice everywhere, markets move daily, and every option seems to come with risk. This guide simplifies the decision, showing how to invest smartly at a young age in a way that fits real life, not just theory.

The unfair advantages of starting early

Before talking about products or allocations, it helps to recognise the edge young investors already have.

Time, compounding’s best friend: Compounding is often described as magical, but it can feel underwhelming at first. In the early years, portfolio growth comes more from what you invest than from what markets deliver. Returns look modest. Progress feels slow.

But compounding doesn’t move in a straight line. Once it gathers momentum, it accelerates sharply. Starting early means you get more of these powerful years. A Rs 20,000 monthly SIP earning 12 per cent annually takes about 15.5 years to reach the first Rs 1 crore. The second crore will arrive in just over the next five years. The third takes barely three more years. Time does most of the heavy lifting.

Higher capacity to take risks: Most investors in their 20s have fewer financial responsibilities. There are no school fees to worry about, no EMIs eating into cash flows, and retirement is decades away. That gives young investors the ability to hold a higher allocation to equity and ride out temporary market declines.

A fall in markets hurts far less when your goal is 25 years away than when it’s five.

But advantages alone don’t guarantee success. How you behave when markets test you matters just as much.

Why behaviour matters more than theory

On paper, a young investor with a long-term horizon should invest entirely in equity. In real life, investing doesn’t happen on spreadsheets. It happens in bull markets filled with excitement and in corrections that test patience and nerves.

Panic during market falls, the urge to ‘do something’, or pausing SIPs at the wrong time can undo the benefit of starting early. Returns depend not just on what you invest in, but on whether you stay invested.

Suggested read: How SIP pause during Covid boosted returns but cut my wealth

That’s why there is no one-size-fits-all solution. The right portfolio depends on how much volatility you can truly live with. To keep things practical, it helps to think in three broad buckets: conservative, moderate and aggressive.

Conservative: Easing into equity

Many investors in their 20s are first-timers. They may understand markets in theory, but have never seen their portfolio fall meaningfully. When the first sharp correction hits, panic is common. SIPs get paused. Long-term plans are questioned. Compounding walks out the door.

If seeing your portfolio turn red keeps you up at night, starting with 100 per cent equity may do more harm than good.

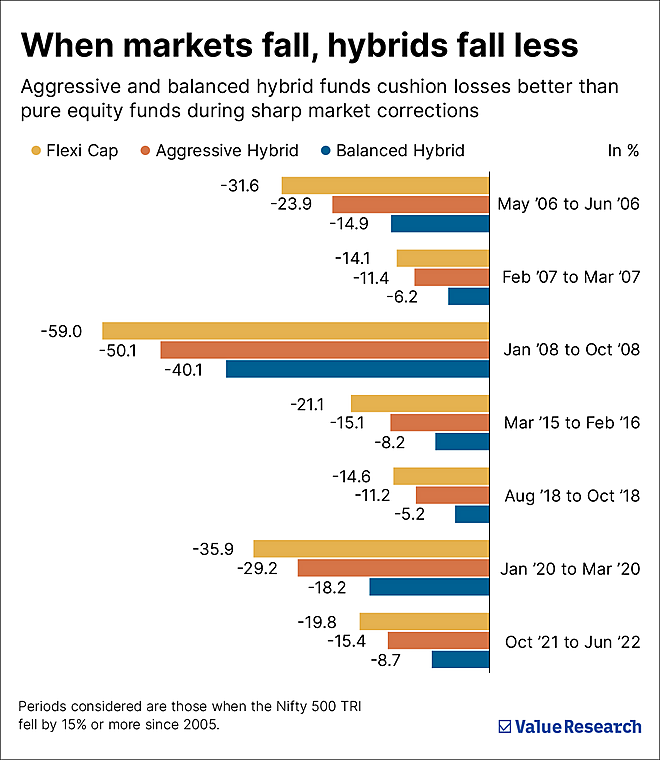

Hybrid funds offer a softer entry point. By combining equity with debt, they reduce volatility and cushion downside during market corrections. Over the past three years, aggressive hybrid funds have held about 22 per cent in debt on average, while balanced hybrids have had closer to 55 per cent. That debt component smoothens the ride.

During periods when the Nifty 500 TRI fell 15 per cent or more since 2005, hybrid funds consistently declined less than pure equity funds such as flexi caps. The message is simple: some debt in the portfolio helps investors stay invested when markets get uncomfortable.

Think of hybrids as training wheels. They help new investors experience market cycles, build confidence and develop discipline. As comfort with volatility grows, equity exposure can be increased gradually without disrupting the compounding journey.

Moderate: Equity, but with balance

Some young investors are better prepared. They may be investing for the first time, but they understand that volatility is part of the process and don’t panic when markets correct. For them, a fully equity portfolio can make sense.

That said, not all equity carries the same level of risk.

Large-cap stocks tend to be more stable, backed by established businesses. Mid- and small-cap stocks, while offering higher return potential, come with sharper volatility and deeper drawdowns. Index-level data since 2005 makes this clear. Mid- and small-cap indices have shown higher volatility, steeper peak-to-trough falls, and significantly longer recovery periods compared with large caps. In some cases, it has taken over six years to reclaim previous highs.

Not all equity are the same

Mid- and small-cap indices show higher volatility, deeper drawdowns and longer recovery periods than large-caps

| Parameter | Nifty 100 | Nifty Midcap 150 | Nifty Smallcap 250 |

|---|---|---|---|

| 3Y standard deviation (%) | 12.5 | 15.8 | 19.4 |

| Maximum drawdown (%)* | -61.1 | -72.9 | -75.6 |

| Average recovery time (days)* | 484 | 647 | 620 |

| Longest recovery (days)* | 998 (2.7 yrs) | 2325 (6.4 yrs) | 2346 (6.4 yrs) |

| *Data based on correction of 15 per cent or more for each index since 2005. Total Return Index (TRI) considered. | |||

For moderate investors, this means volatility needs to be managed, not eliminated. A sensible approach is to build the core of the portfolio around large-cap–oriented funds, while being selective with exposure to riskier segments.

Fund categories such as flexi-cap, large-cap, ELSS, value-oriented and large & mid-cap funds typically hold about half to two-thirds of their portfolios in large-cap stocks. This makes them well-suited for investors who want equity growth without excessive turbulence.

Fund categories with a large-cap focus

These fund categories keep half to two-thirds of their portfolios in large-cap stocks

| Category | Large cap (%) | Mid cap (%) | Small cap (%) |

|---|---|---|---|

| ELSS | 64.9 | 19.4 | 16.8 |

| Flexi cap | 64.5 | 19.6 | 16.4 |

| Value oriented | 62.2 | 15.9 | 22 |

| Large & mid-cap | 50.1 | 39 | 11.5 |

| Data represents the three-year average allocation of an average active fund in each category | |||

Aggressive: Embracing volatility for higher returns

Then there are investors who actively seek higher returns and have the temperament to handle sharp ups and downs. For them, mid- and small-cap funds can play a much larger role.

Historically, these segments have delivered higher long-term returns than large caps. But the journey is anything but smooth. As data shows, these funds can go through long stretches of underperformance and take years to recover after deep corrections.

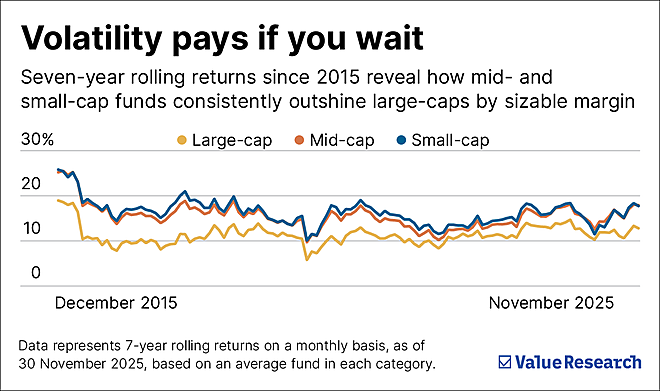

That’s why at Value Research, mid- and small-cap funds are recommended only when the investment horizon exceeds seven years.

Over such long periods, the odds of losing money fall sharply, while the return potential improves meaningfully. Seven-year rolling return data since 2015 illustrates this clearly. Large-cap funds have delivered average rolling returns of around 11.4 per cent. Mid-cap funds have stepped up to about 15.6 per cent, while small-cap funds have averaged roughly 16.3 per cent.

Those percentage differences may look modest, but time magnifies them dramatically. A Rs 10,000 monthly SIP invested for 20 years would grow to about Rs 85 lakh in a large-cap fund. The same SIP could reach around Rs 1.4 crore in a mid-cap fund and nearly Rs 1.6 crore in a small-cap fund. That is compounding rewarding patience and the ability to endure volatility.

The takeaway

Investing in your 20s is often mistaken for a race to take maximum risk. In reality, your biggest edge isn’t aggression. It’s time and flexibility.

You have the freedom to learn, make mistakes, adjust course and still let compounding work in your favour. The data throughout this piece points to a simple truth: the best strategy isn’t the one with the highest return on paper, but the one you can stick with through booms, crashes and long periods of disappointment.

A portfolio abandoned mid-way compounds nothing.

Start with a level of risk that allows you to sleep well at night. As experience grows and volatility becomes familiar rather than frightening, you can gradually take on more risk. Getting this progression right matters far more than achieving a ‘perfect’ allocation on day one.

Markets will test patience repeatedly. But for those who stay invested and behave sensibly, the decisions made in your 20s don’t demand attention. They work quietly, steadily and powerfully in the background.

Starting your investment journey but don’t know where to invest?

Subscribe to Value Research Fund Advisor and get a list of mutual funds tailored to your financial goals. What’s more, you can also evaluate your risk appetite, invest or sell funds directly through the platform and get real-time updates on your portfolio.

Also read: In your 20s? Here's where you can invest to maximise your returns

This article was originally published on December 17, 2025.

Ask Value Research ![]()