Summary: The real secret to long-term wealth isn't a risky sprint; it's bulletproof consistency. New investors often overcommit to risk and panic at the first market dip. We reveal the ideal, balanced portfolio strategy you must adopt in your initial years. This article introduces two foundational portfolios, detailing their long-term performance and breaking down the specific pros and cons to ensure your money grows without you losing sleep.

If you are new to mutual funds, chances are your head is buzzing with questions. “Is equity investing just a lottery?” “Are mutual funds some kind of modern-day scam?” “I can’t put all my money in equity because they are risky”... On the other side, you’ll find investors saying, “Small-cap funds are on fire these days, which one should I buy right now?” or “Debt funds are boring. I’m aggressive and I want high returns!”

At Value Research, we like to keep things simple and balanced. Because investing isn’t about chasing what’s hot; it’s about building wealth without losing sleep.

Just like a T20 cricket team needs a mix of sloggers, stroke-players and dependable anchors, your portfolio also needs balance. That’s why we recommend most new investors start with a 75:25 asset allocation. 75 per cent in equity, and 25 per cent in debt.

Why? Because the equity portion helps your money grow in the long run, while the debt portion cushions the fall when markets turn rough. Think of it as your shock absorber. Many so-called “aggressive” investors panic and exit when markets crash, and that’s exactly when staying invested matters the most. This is where a little debt allocation helps you stay in the market, so that you can be consistent, stay patient, and let compounding do its job.

Two stress-free ways to build long-term wealth

Option 1: Start an SIP in a flexi-cap fund + short-duration debt fund

Put 75 per cent in a flexi-cap fund and 25 per cent in a short-duration debt fund.

- Flexi-cap funds invest across large-cap, mid-cap and small-cap companies, giving fund managers the flexibility to pick the best opportunities across the market.

- Short-duration debt funds invest in bonds and other fixed-income securities with maturities of one to three years. They offer stability and moderate returns with relatively low volatility.

This combination gives you growth (from equity) and safety (from debt).

Option 2: Start an SIP in an aggressive hybrid fund

An aggressive hybrid fund combines both equity and debt in a single portfolio, typically 65-80 per cent in equity and the rest in debt.

So, this fund automatically gives you a balanced exposure. The equity portion fuels growth, while the debt portion helps smooth out volatility.

Performance

Now let’s look at the numbers.

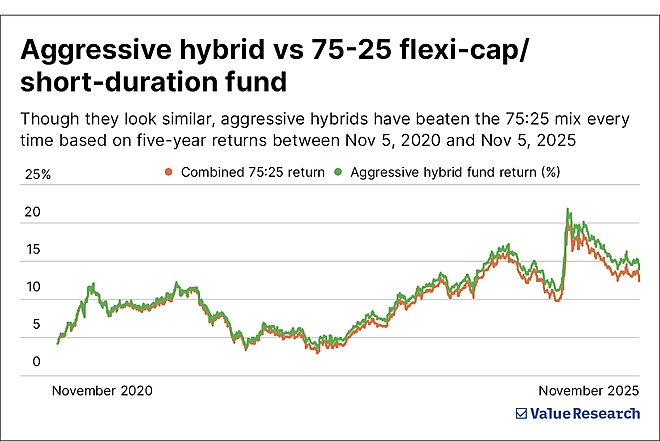

- The average five-year rolling return for Option 1 (75 per cent SIP in flexi-cap + 25 per cent in short-duration debt) is 12.9 per cent.

- The five-year rolling return for an average aggressive hybrid fund is 13.3 per cent.

That’s nearly neck and neck, with aggressive hybrid funds having their noses ahead.

However, when we dug deeper, we found something interesting. Aggressive hybrid funds have a huge edge over the 75-25 portfolio. In fact, their five-year returns were higher every single day during this period between November 6, 2020 and November 6, 2025.

The other advantages of aggressive hybrid funds

Sure, building your own 75-25 mix with a flexi-cap and a debt fund gives you control and customisation. But there’s a catch. You’ll have to rebalance regularly.

Let’s say your portfolio starts with Rs 75,000 in equity and Rs 25,000 in debt. After a year, equity rallies and your portfolio becomes Rs 90,000 in equity and Rs 26,000 in debt. Now, your allocation is 78-22, which is higher risk than your target. To revert to your 75-25 allocation, you’ll need to sell some equity and move it to debt to bring it back to 75-25.

That’s rebalancing. It’s essential but not always easy to do, especially for new investors.

Aggressive hybrid funds, on the other hand, do this automatically. Professional fund managers maintain the equity-debt balance for you, sparing you the emotional decisions and manual effort.

Secondly, aggressive hybrid funds are more tax-efficient.

When the fund manager buys or sells equity or debt within the fund, you don’t pay any tax because it happens internally. Plus, since these funds hold more than 65 per cent equity, they’re taxed like equity funds, meaning lower tax rates even on the debt portion of your investment.

In contrast, if you manage equity and debt funds separately, every rebalance or sale from a debt fund can trigger taxes, which can eat into your returns.

The bottom line

If you’re a conservative investor looking for a simple, tax-efficient and low-stress way to build wealth, aggressive hybrid funds deserve your attention.

They give you balanced exposure to both equity and debt, professional management, and automatic rebalancing, all wrapped in one fund. Because when it comes to wealth creation, simplicity isn’t boring. It’s powerful.

Want to start your SIP in an aggressive hybrid fund?

If you’re ready to take the first step towards stress-free wealth creation, start by exploring Value Research Fund Advisor.

Our team of experts has done the heavy lifting for you by analysing performance consistency, downside protection, fund manager strategy, and portfolio quality to curate a list of the best aggressive hybrid funds suited for long-term investors. These aren’t just top-performing names based on past returns; they’re funds with proven discipline across market cycles.

Visit Value Research Fund Advisor today

Also read: New investor? Here's the right way to pick mutual funds

Ask Value Research ![]()