As equity investors, we want a more holistic view of a company's performance before we invest. That's why we prefer the compounded annual growth rate (CAGR) over the simple growth rate when evaluating a business's growth.

The simple growth rate only captures the percentage change in our investment value. In contrast, the CAGR gives us the average annual growth rate and, thus, is a better growth metric as it evens out the effects of short-term fluctuations.

Well, that's the assumption. The truth is while CAGR is indeed better for analysing growth, it can lead to false assumptions if there are drastic fluctuations in a company's performance over a given period.

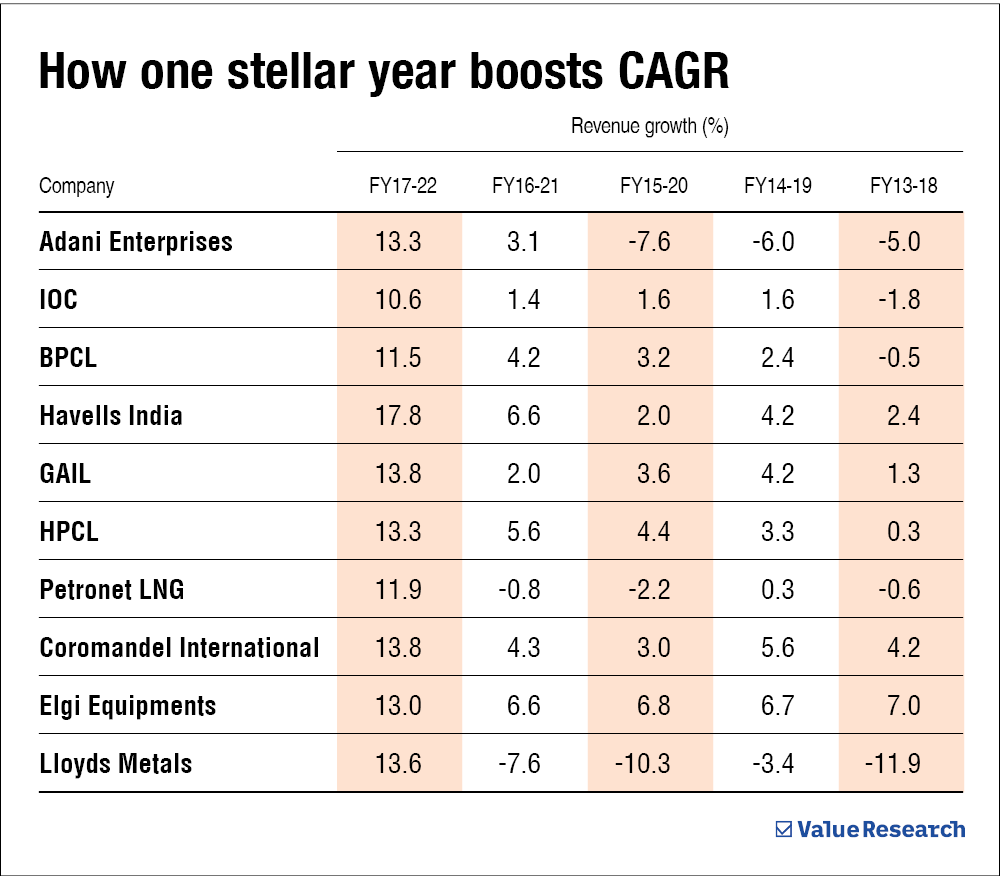

Take the example of Adani Enterprises. Its five-year revenue CAGR for FY17-22, FY16-21, FY15-20, FY14-19, and FY13-18 are 13.3, 3.1, -7.6, -6.0, and -5.0, respectively. See something odd here?

Adani Enterprises saw an unprecedented 76 per cent jump in revenue in FY22. And thus, its CAGR for FY17-22 is far higher than its CAGR for the other periods.

There's no foul play here. Pure data crunching. But this is the risk of blindly relying on growth numbers; it leads to false assumptions. If investors just looked at the CAGR of FY17-22 without looking at the data for other periods, they would believe that the company puts up double-digit topline growth every year on average. However, that is far from the truth.

And Adani Enterprises is just one example. Here are some other similar examples.

These companies (m-cap > Rs 500 crore) have posted a revenue CAGR of more than 10 per cent for the last five years but have recorded less than eight per cent growth in other five-year periods before that.

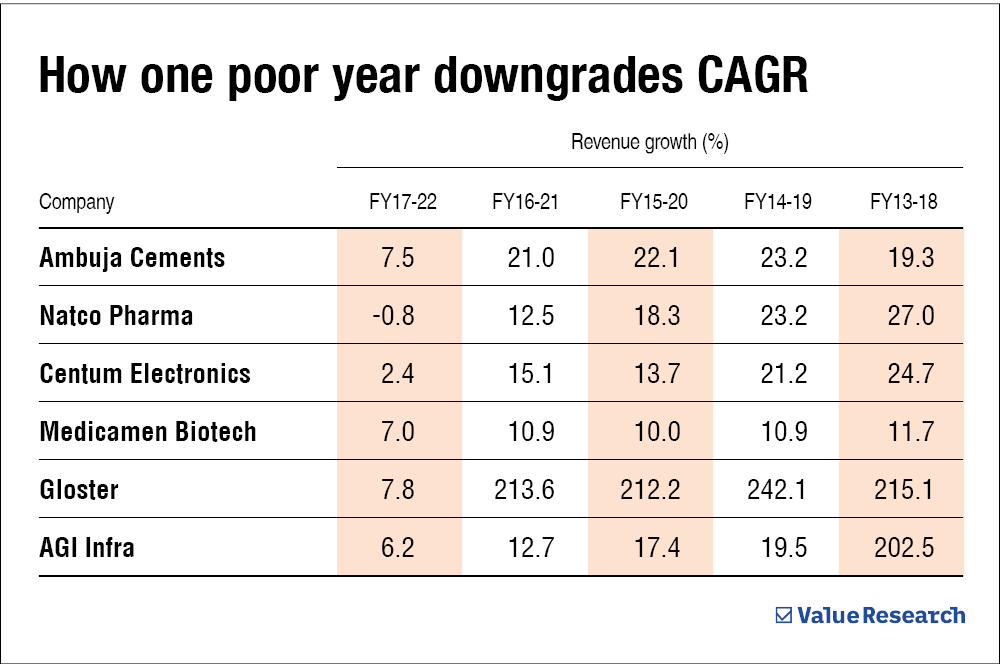

And the reverse is equally possible. A company might be performing well consistently but then have one or two bad years, and suddenly its CAGR figure starts telling a different story.

For instance, these companies have posted a revenue CAGR of less than eight per cent for the last five years but have recorded a revenue CAGR of more than 10 per cent for other five-year periods.

What you should do

Investors should note that in no way are we saying that there's something fundamentally wrong with using CAGR. In addition, the above tables are not an evaluation of how well these companies have performed.

The purpose of our exercise was to show that blindly following CAGR numbers is not a very sound investment strategy. Metrics are used to quantify a business's performance and growth. But they should never be the only triggers for you to invest.

Note: We have excluded banking, finance and insurance companies from our tables since their presentations differ from non-BFSI companies. More than growth rate, quality of growth should be the focus for BFSI companies.

Also read: When the fundamentals tell a different story

This article was originally published on March 27, 2023.

Ask Value Research ![]()