"Mutual funds are simply not working for me," Samarth tells us ruefully over the phone. "I have been a patient mutual investor for several years now. But my returns neither match my expectations nor the time I put in for research."

There was a slight pause over the phone before the 42-year-old business-development professional at a pharmaceutical company continues, "For that matter, I keep finding the 'best-performing fund' of that particular year and invest my money there and yet..." His voice trails off.

Theoretically, his strategy makes perfect sense - except that it can backfire if one ignores a few ground rules.

Theory-practice gap

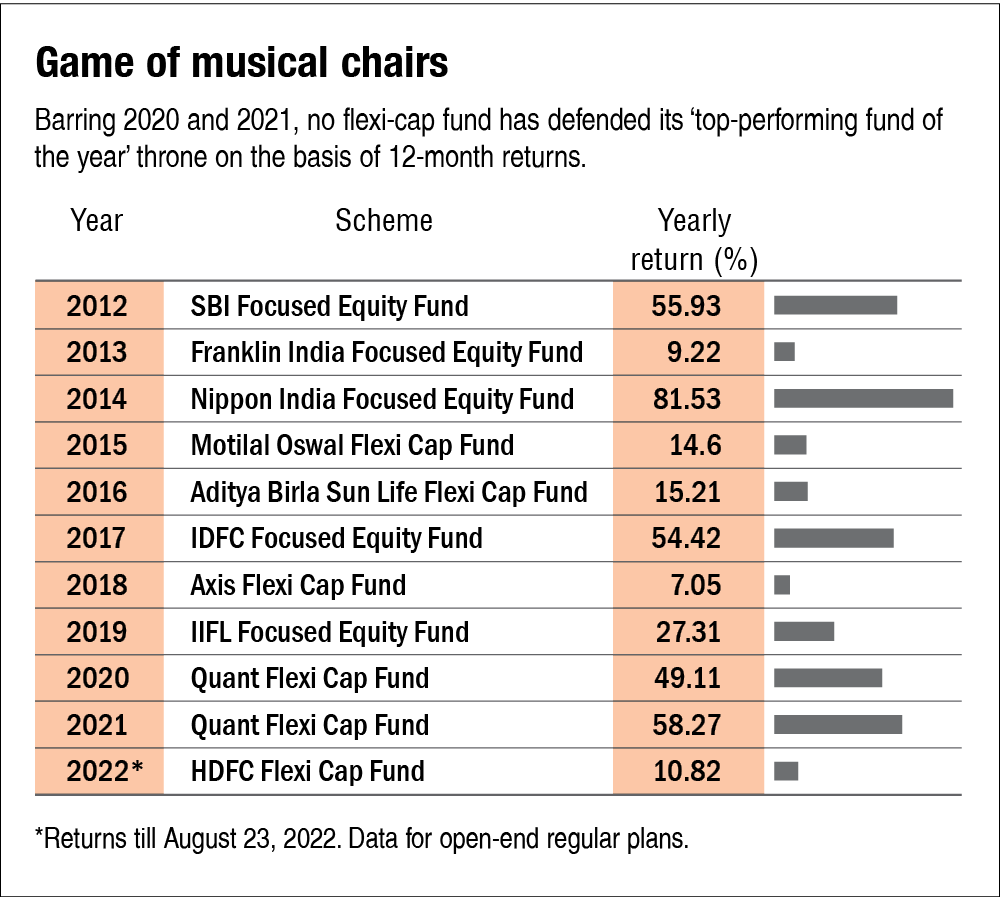

- Samarth didn't realise that no fund remains a 'top performer' on a consistent basis. They have good years and bad.

- Past performance has no bearing on a fund's future performance.

- By buying a new 'top-performing fund' each year, he is actually playing the quantity game, not quality.

Why too many is too bad

Portfolio overlap: There are only those many good stocks in the stock market. And if one buys multiple mutual funds that fall under the same category, there is a strong likelihood that a part of their portfolio is the same. So, the returns one earns might be on similar lines.

Difficult to monitor: Investing in a mutual fund is the first step for an investor. One must track the performance of one's schemes once or twice a year and take necessary decisions, if required. Needless to say, tracking too many funds' performance can be a head-scratching affair.

Dilutes returns: When you have too many funds in your portfolio, on an aggregate level, your portfolio may behave like an index. That defeats the ultimate purpose of investing in active funds.

Loss of interest over small investments: Investing in too many funds often results in allocating a small portion of your portfolio to each fund. This can demotivate an investor to monitor their investment.

How to declutter your portfolio

Back to Samarth, it's as clear as day he needs to reorganise his strategy and take a second bite at mutual fund investing. This time, less scattergun and more deliberate, more measured. Like him, you too can take similar steps to detox your portfolio.

Exit the underperformers: Redeem funds that have underwhelmed for a long time, i.e., minimum two-three years. Take into account the fund's long-term performance, compare it with other funds in the category and the benchmark. Additionally, it would be ideal to assess the performance across market cycles.

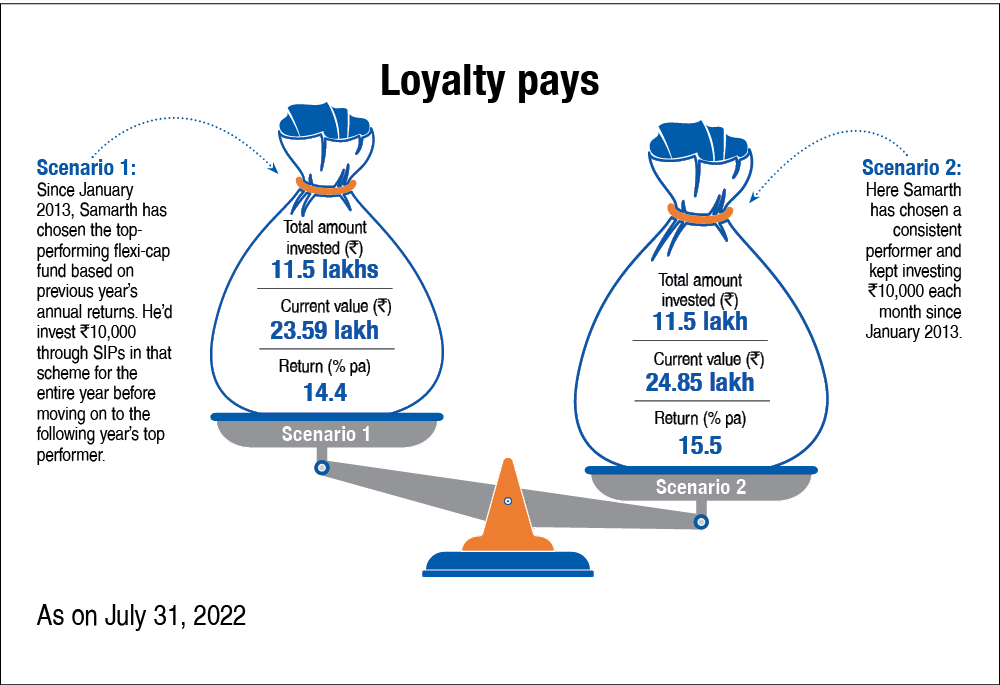

Choose consistent performers: It's futile to chase the buzz, the fad of the season. Instead, you should choose a fund that has consistently performed well in the last three to five years. Let's assume Samarth had started investing in SBI Focused Equity Fund in 2013 and stuck to it. His investments would have grown by 15.5 per cent each year. Why SBI Focused Equity Fund? That's because this mutual fund consistently appeared in the top quartile in the four years preceding 2013. On the other hand, his strategy of cherry-picking the 'top-performing fund' of each year would have yielded 14.4 per cent. Now, the difference in returns may not stand out immediately but if you look at the current value, the stick-to-quality-fund strategy (as shown in Scenario 2) would have added a further Rs 1.26 lakh to his kitty.

Sell the fancy ones: Have you loaded up on thematic or sectoral funds? Give it a second thought. Such funds ride high on short-term trends but as the enthusiasm fizzles, so does their outperformance. These also provide limited diversification as they focus on a particular sector or theme. For most investors, plain vanilla mutual funds are good enough.

Cull the duplicates: If you have multiple funds of the same kind, you may want to keep just one of each type. For instance, if you have several mid-cap funds in your portfolio, you may want to stick to just one or two and channel the rest of your investments in different fund categories.

Follow the core-satellite approach: Have two to three flexi-cap funds as your core holdings. The other funds, such as mid- or small-cap funds, tax-saving funds (ELSS) and international funds, can be supplementary. The core holdings can command most of the capital, while the satellite holdings can be held to give your returns a kicker.

Cut the tail: If you have funds where you have small investments, you may want to exit them and direct that money to your core funds.

Things to be mindful of

Capital-gains tax: Reorganising your portfolio would entail redemption from one scheme and investment in another. The realised capital gains on redemption are subject to 15 per cent tax if your investment is less than 12 months and 10 per cent for funds that are older than a year. However, if the gains from equities are less than Rs 1 lakh, you incur no tax liability. You can plan the changes in your portfolio accordingly.

Exit load: While most equity funds do not charge exit load after a year, it differs from scheme to scheme. So, do check before redeeming a fund.

You can move your money in one shot: If you are investing in an equity fund for the first time, it is essential to stagger your investments. But since you are simply moving your money from one equity fund to another and are already exposed to equities, the shift can be made in a lump sum.

Don't ignore these

- Maintain a contingency fund equivalent to at least six months of your expenses. As per your requirement, you can keep some of the money at home, some in a savings bank account or a sweep-in deposit which is readily withdrawable and the remaining in liquid funds to optimise returns.

- Having a pure term plan is a must for anyone with financial dependents.

- Have adequate health insurance for all family members.

This article was originally published on September 21, 2022.

Ask Value Research ![]()