You have two options if you are looking to invest in a mutual fund.

Option 1: You want a portion of your mutual fund gains to be handed over to you from time to time

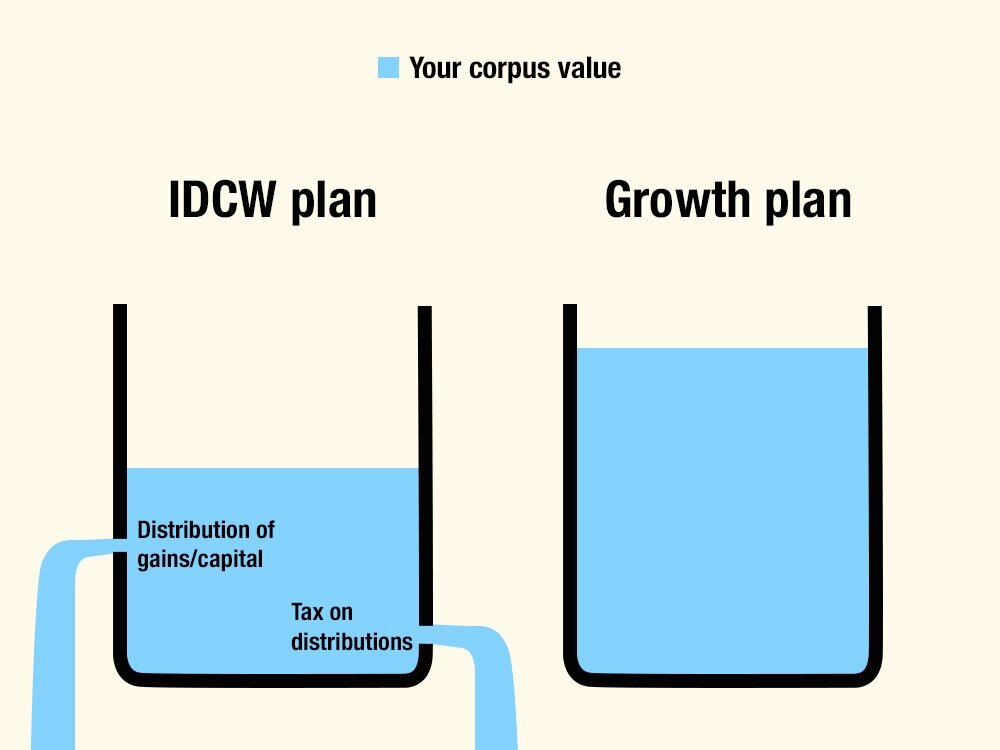

In this case, you should opt for Income Distribution cum Capital Withdrawal (IDCW) plans.

However, they aren't very popular due to the following reasons:

- The quantum of payout and timing is as per the choice of the AMC (the fund house).

- After the payout, the fund's NAV drops by the amount distributed. Hence, you should note that these distributions are not over and above the gains made by the fund.

- The amount paid out is subject to income tax because financially, it's similar to withdrawing money from the fund.

- The biggest pain point is that you lose the advantage of compounding. Since your returns are periodically paid out and, on top of that, they are subject to tax as per your slab rate, a portion of your investment doesn't participate in the future gains made by the fund.

- Lastly, if you do not wish to use the money you get, you will have to figure out where to invest it.

Option 2: You want your investment gains or dividends to be reinvested further

Before that, let's explain why people even choose to reinvest the money they earn from their mutual fund investment? In one line: to allow their money to grow faster.

This is why growth plans are very popular.

Since these plans reinvest all the proceeds (such as dividends received from stocks and realised gains) back into the fund, its NAV keeps growing. Since they give your investments the best chance to grow at a faster pace, growth plans are considered better than IDCW plans.

But what if you are looking for a regular income?

On paper, IDCW plan looks the better choice as these funds hand out your gains from time to time.

However, growth plans are actually the smarter option. Here's why:

- The IDCW option is not dependable because you have no control over when you receive the money. As mentioned earlier, the fund house decides the timing and amount of distribution.

- However, the growth option offers the systematic withdrawal plan (SWP) feature. This gives you total power over the periodic payout.

Therefore, we suggest you keep it simple and always opt for a growth plan. It is more tax-efficient and gives you more control over when and how much you want to redeem.

This article was originally published on May 17, 2022, and last updated on October 18, 2022.

Ask Value Research ![]()