Our regular readers know the importance we attach to life insurance and buying an adequate term plan for that. But what about making a claim when the need arises? Traditionally, in such cases, people have turned to their insurance agents. However, that option isn't available to those buying insurance online. Therefore, one should understand how to file an insurance claim if the need arises. So, here we go.

The websites of almost all life insurance companies have a dedicated 'Claims' section. The section provides detailed information about the process that a nominee needs to go through after the demise of the insured. You can access a collated list of the links to the 'Claims' section of all life insurance companies from the website of the Life Insurance Council.

Even though the insurance claim procedure may differ from insurer to insurer, the broad steps and requirements remain the same. Let's walk you through them.

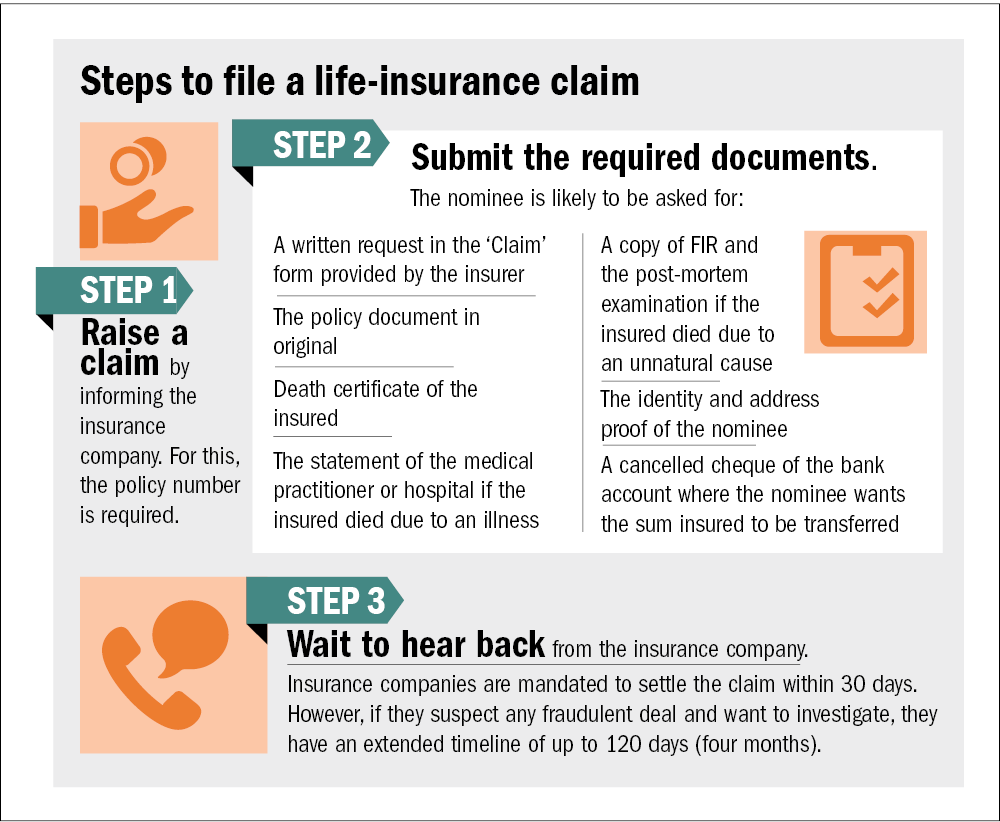

Informing the insurance company

While there is no prescribed time limit for filing the life insurance claim, it is recommended to inform the insurance company at the earliest. In life insurance terminology, this process is usually known as 'raising a claim' or 'intimating a claim'. The nominee needs to provide the policy number and some of their and the insured's basic details. These include name, contact details, date of birth, date of death, etc. Apart from online, one can raise a claim by contacting the customer care of the insurance company through email, text message or phone.

Submitting documents

Once the nominee raises the life insurance claim, the insurance company informs them about the list of documents required to be submitted along with the claim form. While these documents can be submitted online, insurance companies often insist on nominees submitting physical copies as well. One can drop the documents at the company's nearest branch or dispatch them through a courier. Just look for the 'Locate a branch' section on the company's website or call its helpline to locate the nearest branch. Here is a list of documents that a nominee may need to submit in addition to the original policy document:

A claim form: It's a written application intimating about the unfortunate event and requesting the assured sum. In most cases, the insurance company will email the form after being intimated. Alternatively, the form can be downloaded from the 'Downloads' or 'Forms' section of the website. The form is fairly straightforward, and the nominee needs to provide basic information, like their contact details, the policy number, the date of death of the insured, the cause of death, etc.

Death certificate of the insured: The insurance company will generally ask for the original death certificate issued by the local municipal authority. But some insurers may also settle for an attested copy on providing a valid reason.

Statement of the medical practitioner/hospital: The nominee needs to submit a copy of the statement or the certificate issued by the hospital or a medical practitioner who treated the insured if the death was due to an illness.

Identity proof, address proof and a photograph of the nominee: Usual documents like Aadhaar, PAN, driving licence, etc., are sufficient.

A cancelled cheque of the account: The nominee needs to submit a cancelled cheque of the bank account where they want to get the claim amount transferred. As per the law, the benefit amount needs to be transferred electronically to the claimant's bank account.

In addition to the documents mentioned above, the insurance company may ask for additional documents if the insured dies within three years of buying the insurance policy.

Life insurance companies treat such cases as an 'early death' and may process the claim after greater scrutiny to avoid fraudulent deals.

Further, if the cause of death is an accident or is unnatural, the insurance company requires an FIR copy and a post-mortem report.

The turnaround time

As per the regulations set by the Insurance Regulatory and Development Authority of India (IRDAI), a life insurance company must settle the claim within 30 days. However, it may take up to four months for the benefit money to hit the nominee's bank account if the company suspects any fraudulent activity and prefers to investigate the claim before passing the benefit.

What if there is no nominee?

Things get pretty complicated if the policyholder doesn't nominate anyone. In such a scenario, the insurance company is likely to ask for a copy of the will or a succession certificate from the court. In the absence of the same, the claimant will have to prove themself as the sole beneficiary and may need to hire a legal representative.

What if the claim is rejected?

While a legitimate claim should get honoured in the normal course, one cannot completely rule out the possibility of the claim rejection for whatever reason. In such cases, one can opt for the grievance redressal mechanism. We'll cover this topic in detail in one of our forthcoming issues.

This article was originally published on April 05, 2022.

Ask Value Research ![]()