In the first part of the story, we studied the correlation between the rate of compounding of share prices with the amount of benefit derived from a perfectly timed purchase of such equities on an ongoing basis. In this story, let us continue further and see how timing the market turns out for quality stocks.

Investment implication #1: Mean reversion and high-quality stocks

Given that the last 18 months have witnessed a strong rally in the broader market and in share prices of most companies, investors might have a temptation to wait for some 'mean reversion' before making an incremental investment. This approach might make sense for the broader market, but it has a very high probability of failure for Consistent Compounders.

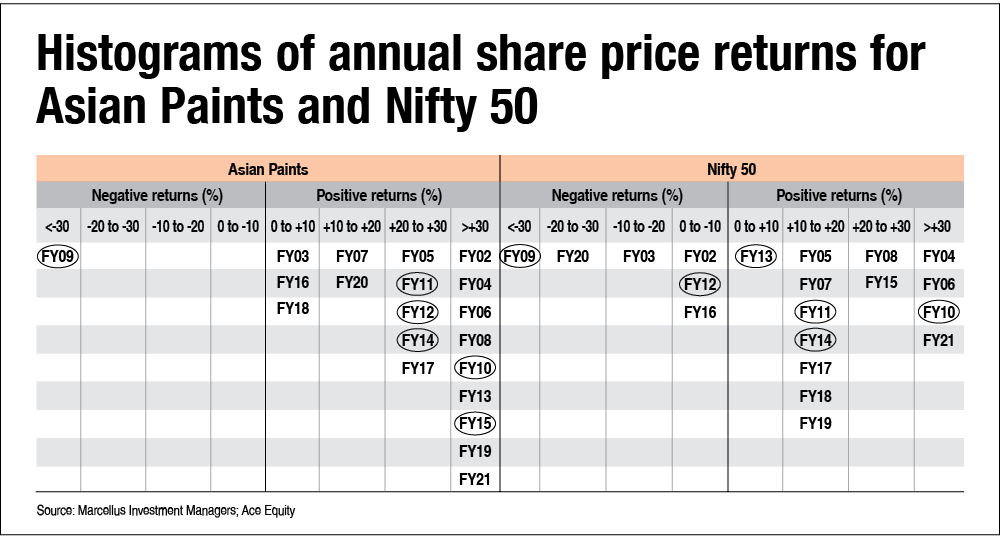

To understand this from empirical evidence, consider the two histograms shown in table 'Histograms of annual share price returns for Asian Paints and Nifty 50' and observe what happens after the drawdown related to the Global Financial Crisis and the very sharp stock market recovery thereafter:

- Both Nifty 50 as well as Asian Paints delivered less than -30 per cent performance during FY09.

- Both Nifty 50 as well as Asian Paints delivered more than +30 per cent performance during FY10.

- Asian Paints consistently delivered high share-price performance in the years after the FY10 recovery, i.e., +20 to +30 per cent in FY11, FY12 and FY14, and more than +30 per cent in FY13 and FY15.

- Nifty 50 demonstrated the concept of 'mean reversion' as it delivered weak returns in the aftermath of the recovery witnessed in FY10, i.e., +10 to +20 per cent in FY11 and FY14; 0 to +10 per cent in FY13 and negative returns (0 to -10 per cent) in FY12.

Replacing Asian Paints with any other company possessing high-quality fundamentals would produce the same conclusions as highlighted above.

Hence, even though FY21 and H1 FY22 have seen a strong recovery in share prices of several companies in the stock market, the concept of mean reversion will not apply to companies with high-quality fundamentals that are expected to continue delivering strong fundamentals which are likely to support their share-price performance in the years to come.

Investment implication #2: Top-ups in high-quality stocks

Investors who wait for a market correction before deploying top-ups from their recurring income (salary, rental, dividends) into high-quality stocks are likely to experience a significant drag in their portfolios vs SIP-based investments, i.e., systematic monthly or quarterly top-up investments. This is due to a combination of three factors: (a) low correlation between high-quality stocks with the Nifty 50 during periods of weakness in the broader market; (b) difficulty of predicting short-term share price movements based on the expected outcome of a looming uncertainty; and (c) the various psychological challenges around investing at a level higher than that of previous top-ups (for example, investing at 52-week high share prices, high P/E multiples, the boring aspect of investing in the same set of stocks repeatedly, whilst all your friends are investing in the hottest IPOs/crypto/start-ups, etc). An SIP in high-quality stocks addresses these three challenges by taking away the need for the investor to make judgement-based calls around market timing.

Note: The following stocks are part of most of Marcellus' portfolios: Asian Paints, Berger Paints, Bajaj Finance, Divis Labs, Pidilite and TCS.

This article was originally published on February 15, 2022.

Ask Value Research ![]()