Now that investors have become familiar with the first two sections of the cash flow statement, i.e., the cash flow from operations (CFO) and the cash flow from investments (CFI), it is time to focus on the third and the final part of the cash flows statement, i.e., the cash flow from financing (CFF).

Meaning of cash flow from financing

The cash flow from financing covers all cash transactions with respect to the capital of the company. Since equity and debt are the two sources of capital for any entity, all transactions involving changes in the total quantity of capital available with the company are covered under cash flow from financing. These cash flows are grouped together so that readers can get the total amounts in each category.

Some examples of cash flows arising from financing activities are:

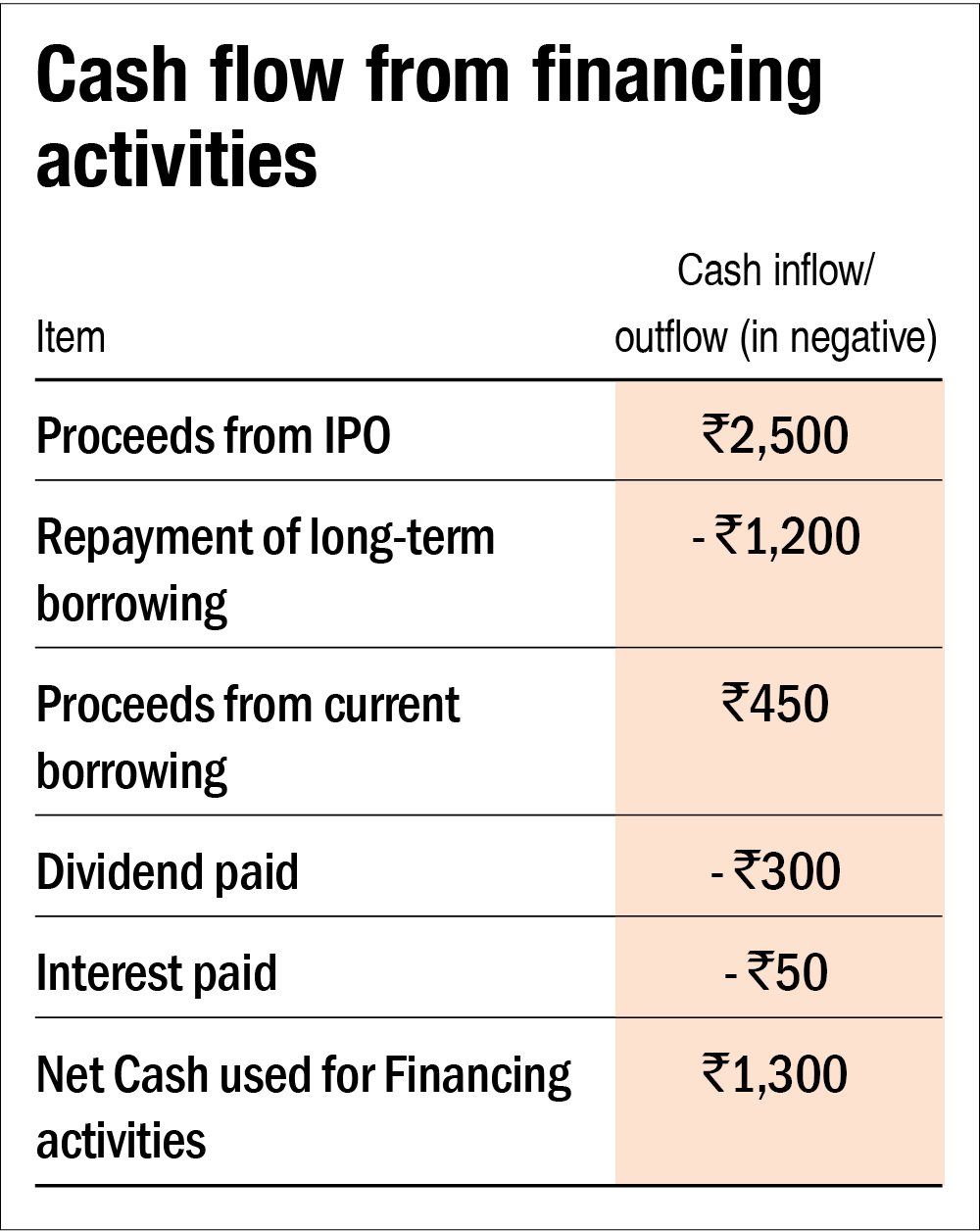

1. Cash proceeds from issuing shares

2. Cash paid to buyback shares

3. Cash proceeds from issuing debentures, loans, notes, bonds, and other short-term or long-term borrowings

4. Cash repayments of amounts borrowed;

5. Cash interest paid; and

6. Cash dividend paid

As always, the gross cash flows are added to give investors the net cash flow from financing. This is added to the cash flows from operations and cash flows from investments to give investors the net cash flows, which is the final amount by which the company's cash has been changed. Negative numbers represent a cash outflow while positive numbers represent cash inflows.

An illustration of a hypothetical company's cash flows from financing would look like this:

Exceptions

Similar to the exceptions found in the cash flow from investing section, the cash flow from financing also has different rules based on the nature of business being conducted by the entity. If the entity is a financial institution (which is in the business of giving out loans), transactions concerning the interest paid and dividends received are usually classified in the cash flow from operations. But for non-financial entities (all other entities), these transactions are classified under cash flows from financing activities because they represent the cost of capital. In other words, given that these transactions represent the price of obtaining the financial resources in order to fund the business, they are classified under cash flow from financing activities.

Another point to keep in mind is that the cash flow from financing discloses only direct borrowing transactions. This means that any indirect borrowing, such as an increase in accounts payable, will not be reflected here.

How is it useful?

While the cash flow from operations gives information about the core set of cash flows that are generated by the business and the cash flow from investing represents how excess cash of the business is invested, the cash flow from financing gives investors insights into how the business itself is funded. An analysis of a historical cash flow from financing activities is useful in understanding the context in which the business has been operating.

Mature companies are likely to have a negative cash flow from financing since they generally have no need for additional capital and therefore tend to return money to capital providers. On the other hand, young and upcoming companies may require a lot of additional capital (both equity and debt) in order to fund either their existing cash-guzzling business operations or to finance future expansions. Even mature companies, when they embark on a major expansion drive, are likely to see their cash flow from financing turn positive as they normally raise external capital to fund the expansion plans.

It is also useful in distinguishing between cash-based dividends (which are actually meaningful) and non-cash-based dividends such as stock splits, stock dividends and bonus issues, etc. (which are not meaningful: Read this) that do not show up on the cash-flow statement (they constitute accounting jugglery).

Conclusion

The proper examination of all the sections of the cash flow statement is a cardinal requirement in every investment decision. All three sections of the cash flow statement, when combined together give a holistic view of the cash transactions in a company. No matter how attractive a company's profit & loss statement and balance sheet are, investors should check if there is a strong correlation with the cash flow statement. Cash flow statements of all the listed companies are available on Value Research's website. Just go to any company's stock page and click on the 'Financials' tab. It is in readers' own interest that they use it to their best advantage.

Also in the series:

Cash flows: Investing activities

Cash flows: Operating activities

This article was originally published on February 08, 2022.

Ask Value Research ![]()