In our story, MedPlus Health Services IPO: Information analysis, we shed light on the critical details of the IPO, along with important information about the company. Here we will answer some questions about the pharmacy retailer and evaluate it on parameters like management, financials, valuations, etc.

IPO questions

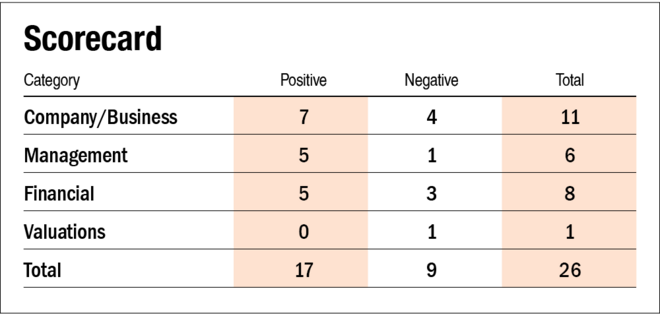

The company/business

1) Are the company's earnings before tax more than Rs 50 crore in the last 12 months?

Yes. The company reported a profit before tax of Rs 141 crore in the last twelve months ending September 30, 2021.

2) Will the company be able to scale up its business?

Yes. Healthcare has been one of the key focus areas since the onset of the pandemic. The Indian pharmacy retail market is expected to grow at a CAGR of approximately 11 per cent in the next five years. Moreover, penetration of organised retail, which includes Brick and Mortar chains and E-commerce, is expected to increase from 10 per cent in FY20 to 20 per cent in FY25, implying a CAGR of 25 per cent.

3) Does the company have recognizable brands truly valued by its customers?

Yes. The company is the second-largest pharmacy retailer in India in terms of revenues and number of stores in FY21.

4) Does the company have high repeat customer usage?

Yes. The company tends to open stores in densely populated areas of the target city to ensure a catchment area serving at least 10,000 to 15,000, thus leading to repeat customer purchases. Also, the company provides discounts and offers through its loyalty program for customer retention.

5) Does the company have a credible moat?

No. Though the company is the second-largest retailer, it does not have any particular moat to safeguard its business.

6) Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. The company does not face any geopolitical risks but has to adhere to major applicable drug laws in India.

7) Is the company's business immune from easy replication by new players?

Yes. The company has a total store count of 2,326, which a new player might not easily replicate.

8) Can the company's product withstand being easily substituted or outdated?

Yes. The company's product mostly includes pharmaceutical and wellness products, which cannot be substituted or outdated.

9) Are the customers of the company devoid of significant bargaining power?

No. The company's customers include individuals who have plenty of other options apart from the company.

10) Are the suppliers of the company devoid of significant bargaining power?

No. The company's suppliers include pharmaceutical manufacturers and FMCG companies, which also have large distribution channels and do not solely rely on MedPlus.

11) Is the level of competition the company faces relatively low?

No. The company faces stiff competition from the unorganised retailers, which constitute the largest market share in pharma retailing and other physical retail chains and e-commerce pharmacies.

Management

12) Do any of the company's founders still hold at least a 5 per cent stake in the company? Or do promoters hold more than a 25 per cent stake in the company?

Yes. Post-IPO, the promoter and promoter group will hold about a 40.4 per cent stake in the company.

13) Do the top three managers have more than 15 years of combined leadership at the company?

Yes. The managing director and CEO, Gangadi Madhukar Reddy, has been associated with the company since its inception in 2006.

14) Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes, we have no reason to believe otherwise.

15) Is the company free of litigation in court or with the regulator that casts doubts on the management's intention?

Yes. Though there are many pending cases against one of the subsidiaries, that does not cast doubt on the management's intention.

16) Is the company's accounting policy stable?

Yes. As per the auditors' report, the accounting policy is stable.

17) Is the company free of promoter pledging of its shares?

No. The company's promoters have pledged 17.7 per cent of their stake in the company.

Financials

18) Did the company generate a current and three-year average return on equity of more than 15 per cent and return on capital employed of more than 18 per cent?

No, the company's three-year (FY19-21) average return on equity was 4.8 per cent and a return on capital employed of 22.1 per cent. For FY21, the company generated a return on equity of 10.1 per cent and a return on capital employed of 22.1 per cent.

19) Was the company's operating cash flow positive during the last three years?

No. The company reported negative cash flows from operations in the fiscal year 2020.

20) Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes. The company's revenue grew at a CAGR of 16.2 per cent from Rs 2,272 crore in FY19 to Rs 3,069 crore in FY21.

21) Is the company's net debt-to-equity ratio less than one, or is its interest-coverage ratio more than two?

Yes. The company is net-debt free. However, it has total lease liabilities of Rs 542 crore as on September 30, 2021.

22) Is the company free from reliance on huge working capital for day-to-day affairs?

No. The company's business is working capital intensive, primarily required to finance inventories for the stores.

23) Can the company run its business without relying on external funding in the next three years?

Yes. The company expects to use the net proceeds from the IPO to fund the working capital, limiting its requirement to rely on external funding.

24) Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. The company's short-term borrowing has decreased from Rs 104 crore in FY19 to Rs 57 crore in FY21.

25) Is the company free from meaningful contingent liabilities?

Yes, the company has contingent liabilities of Rs 12 crore as of March 31, 2021, which accounts for 1.5 per cent of its equity.

Stock/valuations

26) Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the company's stock offers a yield of 2.0 per cent as of September 30, 2021.

27) Is the stock's price-to-earnings less than its peers' median level?

Not applicable. There is no other listed company engaged in a similar business. Post-IPO, the company's stock will trade at a P/E of 88.5 times.

28) Is the stock's price-to-book value less than its peers' median level?

Not applicable. The company does not have any listed peers. Post IPO, the company's stock will trade at a P/B of 6.8 times.

Also read MedPlus Health Services IPO: Information analysis to learn about key IPO details and important information about the company.

Disclaimer: The author may be an applicant in this Initial Public Offering

Ask Value Research ![]()