In our story, Anand Rathi Wealth IPO: Information analysis, we have shared the key details of the IPO, along with important information about the company. Here we will answer some questions about Anand Rathi Wealth and evaluate it on parameters like management, financials, valuations, etc.

IPO questions

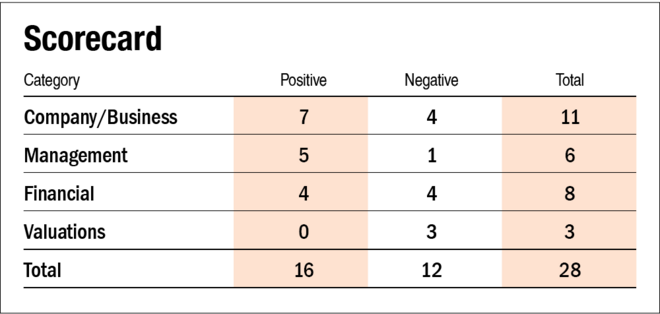

The company/business

1) Are the company's earnings before tax more than Rs 50 crore in the last 12 months?

Yes. The company reported earnings before tax of Rs 64 crore for FY21.

2) Will the company be able to scale up its business?

Yes. Mutual fund penetration and individual wealth is expected to increase rapidly in the next few years, which will help the company expand its business comfortably.

3) Does the company have recognisable brands truly valued by its customers?

Yes. Anand Rathi wealth management is a reputed company among high net worth individuals, and the company has been able to increase its number of clients consistently.

4) Does the company have high repeat customer usage?

Yes. Around 55 per cent of the company's clients have been with it for the last three years.

5) Does the company have a credible moat?

No. Even though the company has a recognised reputation, it does not offer anything unique that other companies cannot provide.

6) Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. Even though the company exists in a highly regulated environment, it has adhered to all the regulations. This includes the issue regarding whether the company should be declared an NBFC, where the management has sufficient reasons to defend itself.

7) Is the business of the company immune from easy replication by new players?

No. There are many players, both Indian and foreign, that are launching their wealth management services every year. They can easily replicate the business.

8) Is the company's product able to withstand being easily substituted or outdated?

No. Due to the presence of many competitors and identical services launched by them, the company's services can be easily substituted.

9) Are the customers of the company devoid of significant bargaining power?

Yes. Since the customers are generally high net worth individuals and families, they do not have bargaining power. Also, the company operates in a regulated environment under which it can charge specific commissions from its clients, which does not leave any room for bargaining power to its customers.

10) Are the suppliers of the company devoid of significant bargaining power?

Yes. The commissions paid by AMCs to wealth management companies are part of expense ratios which are fixed. So the suppliers do not have any bargaining power on that front.

11) Is the level of competition the company faces relatively low?

No. Several Indian and foreign wealth management companies compete against Anand Rathi Wealth.

Management

12) Do any of the company's founders still hold at least a 5 per cent stake in the company? Or do promoters hold more than a 25 per cent stake in the company?

Yes. The chairman, Anand Rathi, would continue to hold a 12 per cent stake post issue, and promoters, including the promoter group, would have a 48.8 per cent stake post issue.

13) Do the top three managers have more than 15 years of combined leadership at the company?

Yes. The top three managers have more than 15 years of combined experience. Chairman Anand Rathi, CEO Rakesh Rawal, and non-executive director Pradeep Gupta have been with the company since 2005.

14) Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes. We have no reason to believe otherwise.

15) Is the company free of litigation in court or with the regulator that casts doubts on the management's intention?

No. There are three litigations against the company and seven criminal proceedings against the directors. The minority shareholders of ARDWPL have filed a petition regarding oppression and mismanagement. This casts some doubts on the management.

16) Is the company's accounting policy stable?

Yes. We have no reason to believe otherwise.

17) Is the company free of promoter pledging of its shares?

Yes. The promoters have not pledged their stake.

Financials

18) Did the company generate a current and three-year average return on equity of more than 15 per cent and return on capital employed of more than 18 per cent?

Yes. The company managed to generate a three-year average return on equity of 40 per cent and a return on capital employed of 51 per cent. It managed to generate a return on equity of 21 per cent and a return on capital employed of 28 per cent in FY21. However, we would like to mention that both return on equity and return on capital employed have decreased during the last three years. Return on equity for FY19, FY20, and FY21 was 58, 40, and 21 per cent, respectively. Return on capital employed for FY19, FY20, and FY21 was 78, 48, and 28 per cent, respectively.

19) Was the company's operating cash flow positive during the last three years?

No. The company reported a negative operating cash flow of Rs 21 crore for FY21. This was mainly due to a decrease in advance from customers.

20) Did the company increase its revenue earned by 10 per cent CAGR in the last three years?

No. The company's revenue from operations decreased by 2 per cent CAGR in the last three years.

21) Is the company's net debt-to-equity ratio less than one, or is its interest-coverage ratio more than two?

Yes. The company's debt-to-equity ratio is 0.11 as of August 31, 2021, and the interest-coverage ratio is 23 times for FY21.

22) Is the company free from reliance on huge working capital for day-to-day affairs?

Yes. The company does not need huge working capital for day-to-day operations.

23) Can the company run its business without relying on external funding in the next three years?

No. As the company does not receive any proceeds from the issue, it may need external funding for potential future expansion plans.

24) Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No. The company's short-term borrowings increased at 507 per cent CAGR in the last three years, with Rs 22 lakhs in FY19 to Rs 8.4 crore in FY21.

25) Is the company free from meaningful contingent liabilities?

Yes. The company does not have any meaningful contingent liabilities.

Stock/valuations

26) Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No. The stock will only offer a 3 per cent operating-earnings yield (based on FY21 figures) on its enterprise value.

27) Is the stock's price-to-earnings less than its peers' median level?

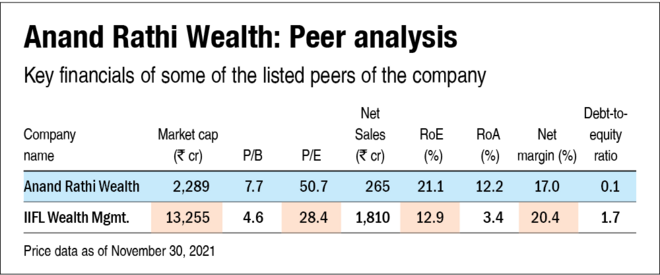

No. The stock would be listed at a P/E of 50.7 times (based on FY21 earnings) against IIFL wealth management's P/E of 28.4 times.

28) Is the stock's price-to-book value less than its peers' average level?

No. The stock would trade at a P/B value of 7.7 times against IIFL wealth management's P/B of 4.6 times. Book value calculated using balances as of August 31, 2021.

Also read Anand Rathi Wealth IPO: Information analysis to learn about the company's key IPO details and important information.

Disclaimer: The authors may be an applicant in this Initial Public Offering.

Ask Value Research ![]()