Similar to the previous bull rallies, a lot of NFOs are being lined up by the fund houses this year by riding on the upheaving stock market. Historically the euphoria created around new schemes has failed to get justified in its returns when compared to old funds. We break down the odds against NFOs performance.

Demystifying poor NFO performance

Understanding why NFOs are in a disadvantageous position against the existing fund schemes is not a hard nut to crack. NFOs are like a golden goose for AMCs and distributors -a goose that has changed form, shape and size over the years - but one thing that has remained constant is that they don't have much of an investment case for retail investors. There are business reasons for launching new funds which do not find a place in the AMC's pitch documents or your distributor's enticing theory about why that NFO is the best investment you would ever make. Fund houses have an agenda to gather more money from investors' pocket, thereby increasing their AUM. A higher AUM means a higher management fee that they can earn.

One can argue why they need to bring in new schemes as they can market their existing funds as well to fulfill that purpose. Well, it's not that easy and also not always desirable. For instance, SEBI has mandated AMCs to charge expense ratio within the maximum upper limit that decreases in tandem with a rising AUM. So, if an old fund grows bigger, it fetches lower fee for the fund house and lower commission for the distributors. Also, the storytelling that goes behind making the new fund look lucrative is far too difficult to position for an existing one. So, NFO is comparatively an easy money-minting tool for AMCs. In fact, for the same reasons, distributors often make investors churn from their existing scheme to a new one.

Another factor that comes at play is lack of history in the case of NFOs. It's a no brainer that within the entire universe of mutual funds, some perform well and others lag behind. Choosing a new fund when there is a plethora of other good options to invest in is avoidable on the part of investors. No reasonable judgment can be made about how a new fund would perform as compared to its peers. It is simply equivalent to betting.

Then raising funds is one task but building portfolio out of it is another and more important one. Most of the time NFO boom arises when stock market seems to be overvalued. Deploying large amounts of money at such high valuations counter-intuitively leads to poor performance as compared to existing schemes. Currently, the Sensex is trading at an all-time high price-to-earnings ratio (P/E) of about 32.

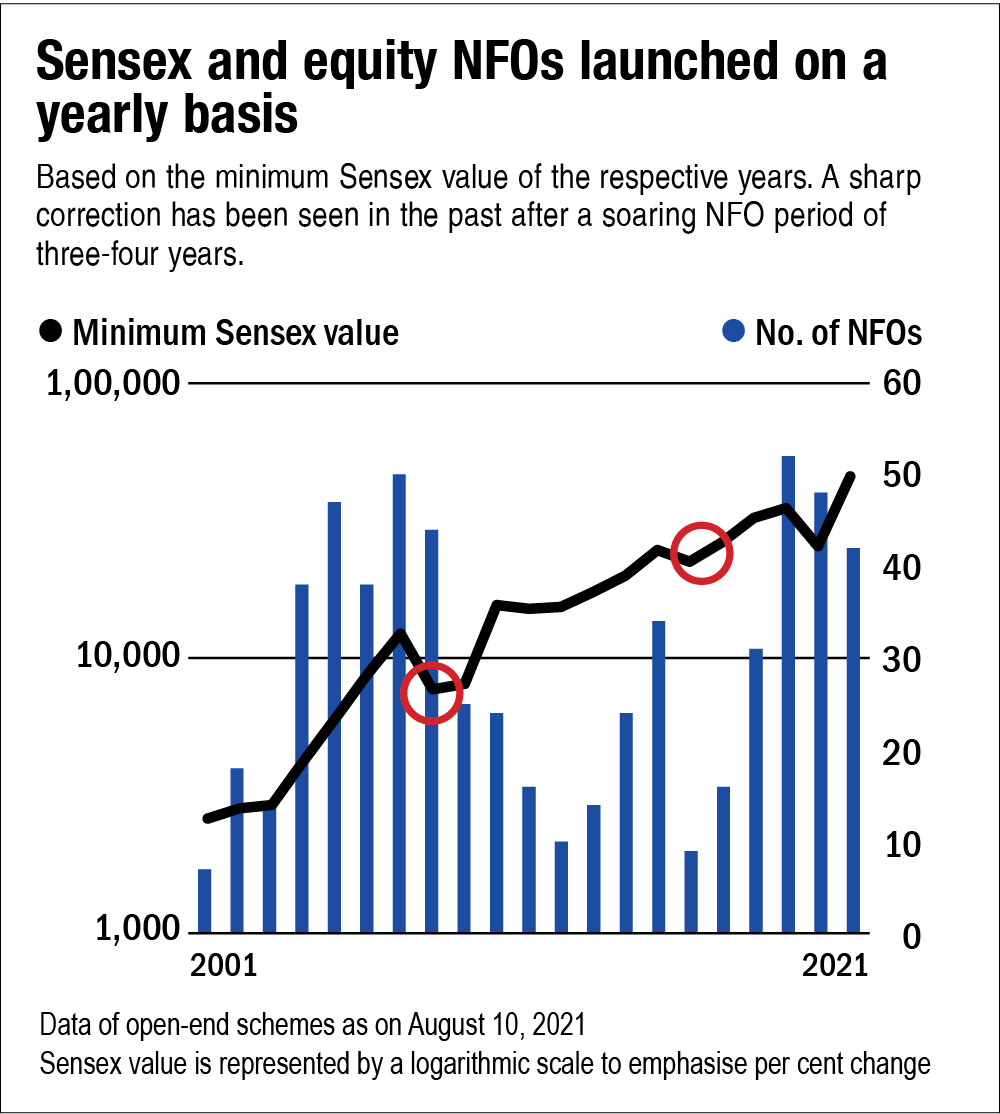

Highs and lows of NFOs and Sensex

Generally, it has been observed that the NFO euphoria hits its crescendo when the markets are peaking. Subsequently, such periods are followed by a deep market correction. There have been two such instances - 2008 and 2016 - apart from the COVID-led crash in March 2020.

This tends to be more painful for NFO investors as they end up investing lump-sum amount in equity, that too at overheated market levels, violating the principle of systematic investing.

Also in this series:

NFO mania is back: Old vs new funds

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()