Krishna Institute of Medical Sciences (KIMS) operates multi-speciality hospitals in Andhra Pradesh (AP) and Telangana. Under Dr B Bhaskara Rao, its founder-promoter, the company has grown from a single hospital in Nellore, AP, with a capacity of 200 beds to nine hospitals across AP and Telangana, with a combined capacity of 3064 beds within two decades.

The company offers services across 25 specialities and super specialities and focuses on tier-II and tier-III cities. The company has historically adopted a very calibrated approach while expanding its operations and is now looking to expand to Chennai and Bangalore. It has made a conscious decision to provide services at relatively affordable prices and is able to do so without sacrificing margins, owing to various reasons such as high operating leverage, lower capital and operating costs and the focus on high patient volume.

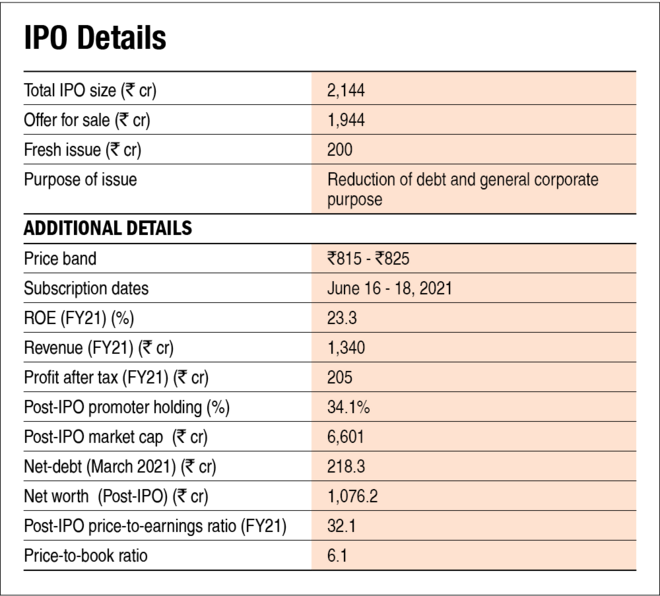

This is the company's second attempt to come out with an IPO after a failed attempt in 2018. During the financial year 2020-21, its revenue was pegged at Rs 1340 crore, while its profit at Rs 279 crore.

Strengths

Operations in the healthcare sector: Healthcare in India is an underpenetrated sector. Poor ranking on metrics like the patient-to-bed ratio, healthcare spends as a percentage of GDP and costs paid out of pocket mean that there is a long runway for growth.

Superior financials: From a financial standpoint, the company boasts of strong metrics such as a high RoCE (28 per cent), low working-capital cycle and negligible debt.

Diversification across specialities: The company offers treatment across multiple specialities. Its revenues are fairly distributed across specialities such as cardiac, neuro, renal, ortho, oncology, etc. The company is well-diversified and not much dependent on any particular speciality.

Risks and weaknesses

High concentration: All the company's hospitals are located in just two neighbouring states. Even among all these hospitals, the company derives almost 65 per cent of its revenue from just one hospital in Secunderabad. Therefore, any adverse circumstances affecting these practice areas could pose a challenge to the company's operations.

Regulatory risk: Healthcare, being crucially important for the life and health of human beings, is a politically sensitive topic and hence, subject to various risks. The company faces risks in the forms of unsatisfied patients filing claims for seeking compensation, criminal proceedings for investigating alleged medical negligence and the government's restrictions which have a direct impact on profits. Additionally, the CBI is currently investigating the company for insurance fraud.

Impact of COVID: The latest financial year saw a precipitous drop in the volume of in-patient and out-patient numbers. The pandemic has reduced patients' willingness to visit hospitals, thereby reducing the revenue from elective surgeries and medical tourism, which tend to be a high-margin business. Any future outbreak may result in a similar situation.

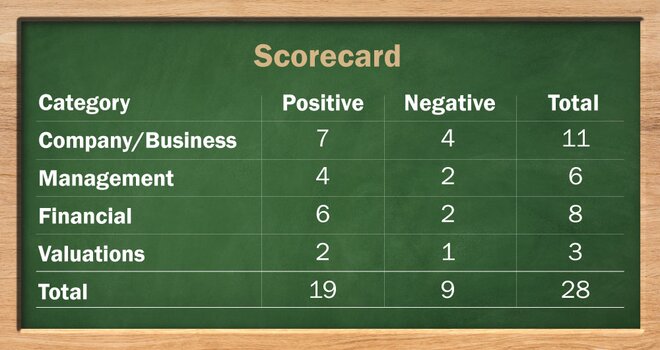

IPO Questions

Company/Business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

Yes. For the financial year ended in March 2021, the company made a profit before tax of Rs 279 crore.

2. Will the company be able to scale up its business?

Yes. Although the company's operations are limited to just two states, it is now planning to expand its operations to two other states. But it is not an easy task and involves a high amount of capital expenditure.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, the 'KIMS' brand is fairly well recognised in Andhra Pradesh and Telangana.

4. Does the company have high repeat customer usage?

No. But in the healthcare segment, repeat customer usage is not necessarily a good thing.

5. Does the company have a credible moat?

No. While it is not an easy task to set up a new hospital and establish the credibility required to attract patients, the fact remains that there exists absolutely no moat for the company.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. Since the company has navigated the inherent regulatory risks for the past two decades, we have no reason to believe otherwise.

7. Is the business of the company immune from easy replication by new players?

Yes. While new players can theoretically set up hospitals, it would certainly not be an easy task.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes. Medical treatment cannot be either substituted or outdated. It will always stay relevant.

9. Are the customers of the company devoid of significant bargaining power?

Yes. Since the company operates in the multi-speciality segment, there wouldn't be too many players.

10. Are the suppliers of the company devoid of significant bargaining power?

No, its main suppliers - doctors, medical-equipment manufacturers and pharmaceutical companies - generally have many options to choose from.

11. Is the level of competition the company faces relatively low?

No. While there may be less competition in any particular micro-markets, on an overall basis, there are quite a few players and hence, high competition.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than a 25 per cent stake in the company?

Yes. The promoters will hold approximately a 34 per cent stake in the company after the IPO.

13. Do the top three managers have more than 15 years of combined leadership experience at the company?

Yes. The managing director has been associated with the company for more than 15 years.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes, we have no reason to believe otherwise.

15. Is the company free of any litigation in court or with the regulator that casts doubts on the intention of the management?

No. While there may not be a high number of cases, a CBI case for alleged insurance fraud is a question mark.

16. Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise.

17. Is the company free of promoter pledging of its shares?

No. Mr Bhaskara Rao has pledged almost 52 per cent of his shares for availing various credit facilities.

Financials

18. Did the company generate the current and five-year average return on equity (ROE) of more than 15 per cent and return on capital employed (ROCE) of more than 18 per cent?

No. While the latest ROE was 28 per cent, its five-year average is well below 15 per cent. The company had negative equity for FY17 and FY18. Also, its five-year average return on capital employed is around 15 per cent.

19. Was the company's operating cash flow positive during the previous year and at least four out of the last five years?

Yes. The company's cash flow from operations was positive for the last five years.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes. The company's revenue from operations increased from Rs 663 crore in FY18 to Rs 1,330 crore in FY21, registering a CAGR of 26 per cent.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes. The company's net debt-to-equity ratio was just 0.02 times and its interest-coverage ratio for FY21 was 8.47.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes. While the quantum of working capital required is not huge, it is also not insignificant.

23. Can the company run its business without relying on external funding in the next three years?

Yes. While the company does not need any external funding for its current operation, it may need money for future expansion.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No. The company's current borrowings increased from Rs 175 crore in FY19 to Rs 552 crore as on March 31, 2021.

25. Is the company free from meaningful contingent liabilities?

Yes. At Rs 23.9 crore, the company does not have any meaningful amount of contingent liabilities.

Stock/Valuation

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No. The operating-earnings yield as of March 2021 was 5.71 per cent.

27. Is the stock's price-to-earnings less than its peers' median level?

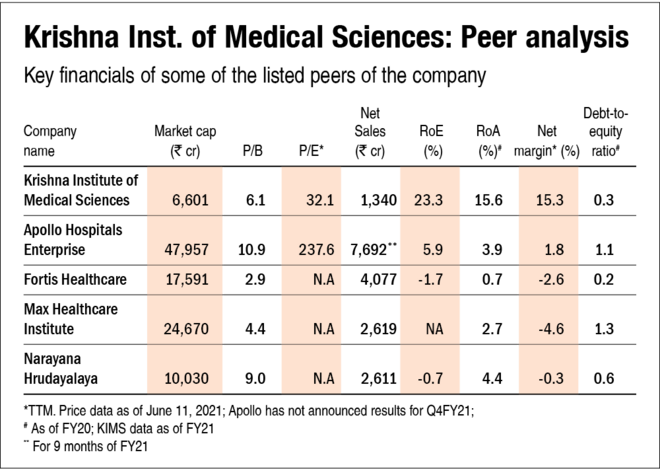

Yes. At about 32 times, the company's P/E would be lower than that of Apollo Hospitals. Most other listed hospital companies are making losses and therefore, don't have a P/E ratio.

28. Is the stock's price-to-book value less than its peers' average level?

Yes. The company's P/B of 6.1 is less than the competitors' average of 6.8.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()