Starting its journey in 1993 from a single showroom in Thrissur, Kerala, Kalyan Jewellers has established itself as a large pan-Indian jewellery retailer. Promoted by Mr T S Kalyanaraman, it now operates 107 showrooms across 21 states and also has 30 showrooms in the Middle East.

Over the years, the company has built its business through increased transparency and highly customised offerings for different regions it operates in. It has created a wide array of sub-brands (12) to cater to various segments, such as 'Muhurat' for wedding jewellery; 'Mudhra' for antique (non-yellow gold finish); 'Glo' for casual diamond jewellery, etc. This has enabled the company to address specific customer niches at various price points.

Also, Kalyan Jewellers employs a marketing strategy to set up dedicated centres (called 'My Kalyan'), which are solely focussed on channelising customers to their various stores. Since a significant proportion of the demand for gold jewellery originates from rural and semi-urban locations, where the presence of organised jewellery is low, the staff (numbering almost 2700) at these centres also play an active role in door-to-door marketing efforts and customer engagement. Barring a brief misadventure in FY2019, when an attempt to convert these promotional centres into points of sale for small-ticket items backfired (resulting in reduced marketing and overall sales), these centres have served the company well (it contributed a fifth to the company's top line in the current fiscal).

Strengths

The company has disrupted the unorganised market by adopting higher transparency methods, such as hallmarking, price disaggregation, etc., and offering higher quality products. Customer awareness and education campaigns have also helped increase the trust factor.

Risks & concerns

The company's business model is characterised by high operating leverage and a very low margin. This combination makes it vulnerable to any fluctuations in the business cycle. For example, during the nine months of the current fiscal, although the top line decreased by only about 30 per cent (due to the impact of the pandemic-induced lockdown) as compared to the year-ago, the company's bottom line swung from a profit of around97 crore to a loss of 81 crore.

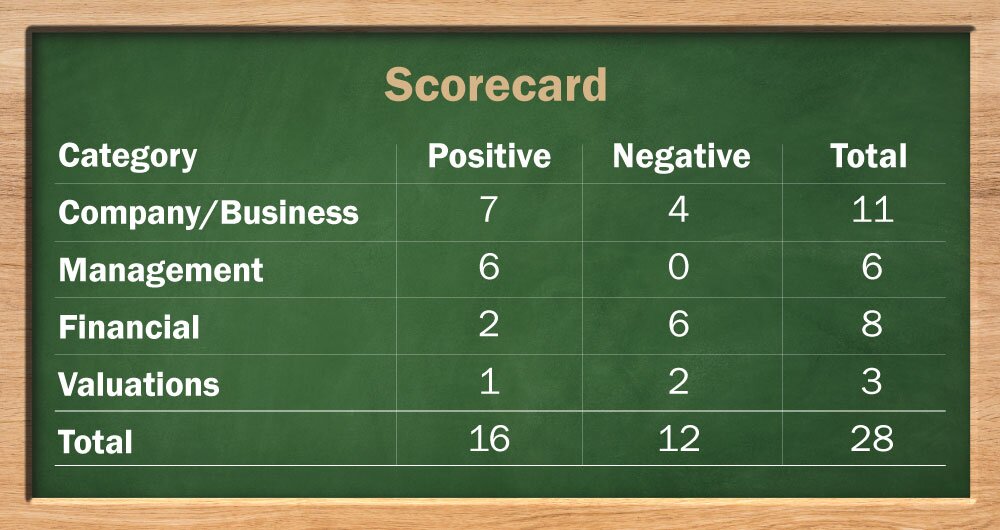

IPO Questions

The company/business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

No. The profit before tax during the previous 12 months (from January 2020 to December 2020) was only Rs 7.9 crore. But this was because of the impact of the pandemic-led lockdown. Earnings before tax for FY2020 was Rs. 220.89 crore.

2. Will the company be able to scale up its business?

Yes. The company can increase its branch network, as well as its same-store sales. But it would depend on whether the demand for gold jewellery bounces back and the company's ability to deleverage its balance sheet.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes. The company has built the 'Kalyan' brand over the years, which is recognised and valued by its customers.

4. Does the company have high repeat customer usage?

Yes. Customers who are satisfied go back to the same store for the purchase of gold jewellery in the future.

5. Does the company have a credible moat?

No. The company does not register its designs which it keeps updating on a regular basis. But, it is not an easy task to scale up and establish a pan-India presence. Establishing a trustworthy brand is also a very challenging process.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. It is an organised player and has handled regulatory challenges in the past.

7. Is the business of the company immune from easy replication by new players?

No. There is a lot of competition in this space from both organised and unorganised players. And competitors can simply copy the jewellery designs.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes. Gold and jewellery have certain characteristics that have made them very desirable. They are unlikely to be substituted or outdated.

9. Are the customers of the company devoid of significant bargaining power?

Yes. Since the company operates in the B2C space, no single customer can exert any bargaining power.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes. Gold is a widely available precious metal and no single supplier can exert any bargaining power.

11. Is the level of competition the company faces relatively low?

No. Since there are a large number of players in the market, the level of competition is quite high.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes. The founding promoters will continue to hold more than 60 per cent stake in the company, post IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes. The founding promoter, who is the current managing director of the company, has been associated with the company since 1993.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes. We have no reason to believe otherwise.

15. Is the company free of any litigation in court or with the regulator that casts doubts on the intention of the management?

Yes. Although there are ongoing disputes, the nature of the litigation does not cast any doubt on the intention of the management.

16. Is the company's accounting policy stable?

Yes. The company has been following a stable accounting policy.

17. Is the company free of promoter-pledging of its shares?

Yes. None of the shares of the promoter is pledged.

Financials

18. Did the company generate the current and three-year average return on equity (ROE) of more than 15 per cent and return on capital employed (ROCE) of more than 18 per cent?

No. The average three-year RoE and RoCE for the period between FY18 and FY21 were 5.4 per cent and 11.1 per cent, respectively. The RoE and RoCE for FY 20 were 7.25 per cent and 11.05 per cent, respectively.

19. Was the company's operating cash flow positive during the previous three years?

No. Although cash flows from operations for FY18, FY19 and FY20 were 1057 crore, 428 crore and 326 crore, respectively, it was -210.9 crore for the nine months ended December 2020.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

No. The company's revenue declined from 10,547 crore in FY 2018 to 10,100 crore in FY 2020.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

No. The company's interest-coverage ratio for FY20 was 1.53 and its debt-to-equity ratio was 1.12 as of December 2020.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No. Given the expensive nature of the company's raw material, the company relies on huge amounts of working capital in its day-to-day affairs.

23. Can the company run its business without relying on external funding in the next three years?

Yes. Post-IPO, the company should be able to run its business without relying on external funding needs. However, it may be a bit challenging to expand the current business.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. The company's short-term borrowings have declined from Rs 3,796 crore in FY2018 to Rs 3,439 crore as of December 2020.

25. Is the company free from meaningful contingent liabilities?

No. The company reported contingent liabilities worth Rs 1208.84 crore as on December 31, 2020, which amounted to 58.7 per cent of its net worth.

Valuations

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No. Based on a post-IPO enterprise value of Rs 11,001 crore and FY20 operating earnings of Rs 799 crore, the operating-earnings yield is about 7.3 per cent.

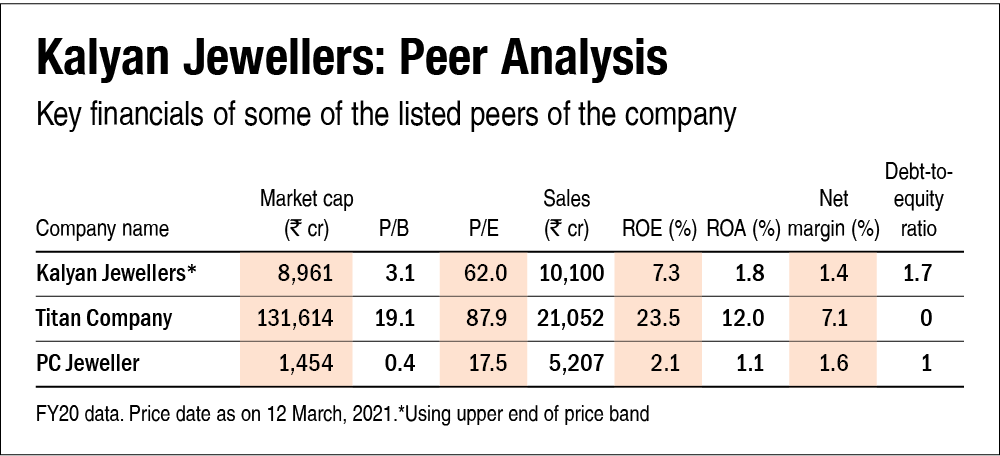

27. Is the stock's price-to-earnings less than its peers' median level?

No. As per the FY20 data, the stock would trade at a P/E of around 62, which is higher than its peers' median P/E of 53.

28. Is the stock's price-to-book value less than its peers' average level?

Yes. At the upper end of its price band, the stock's P/B ratio, on a post-IPO basis, is 5.7, which is lower than its peers' average P/B of 9.7.

Disclaimer: Author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()