The price-to-earnings (P/E) ratio has always been the most common method to look for undervalued stocks. In this method, the price of a stock is divided by the company's earnings per share. The resultant shows the price paid for each rupee of the company's earnings. If the P/E ratio is low, the stock is perceived to be undervalued.

But the P/E ratio is a simplistic method to assess valuation and hence is not flawless. Frequently, stocks trade at high P/E multiples owing to factors such as earnings visibility, a strong track record of corporate governance, generation of high free cash flow and so on. In such cases, it is appropriate to look at the company's median P/E to gauge the valuation.

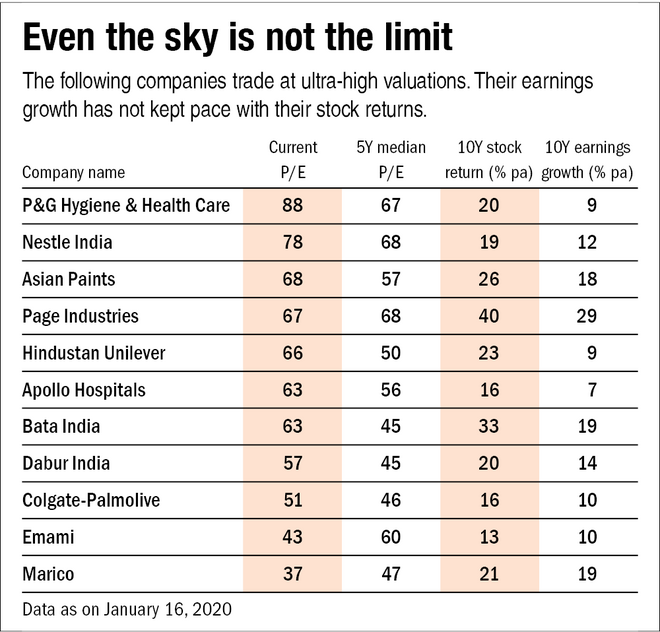

We delved into the BSE 500 companies trading above a P/E of 30 and came across a set of companies wherein the five-year median P/E on a rolling basis has been consistently rising over the last 10 years. In addition, they have never had a five-year median P/E (on a rolling basis) below 30 over the last 10 years. Even though these companies may seem overvalued based on the P/E they trade at, the market keeps pricing them at a premium. They even have positive price return year after year in at least eight out of the last 10 years.

This can attract you to these companies. So, a word of caution. In the September issue of this magazine, we carried a story that assessed the future return potential of such high P/E stocks. The analysis suggested that such stocks may not give good returns in the future if they are driven only by earnings. As one can see in the table, the 10-year price returns of the high P/E stocks have exceeded their 10-year earnings growth.

If any of the factors that are driving the valuations of these stocks change, they may see a significant correction.

Ask Value Research ![]()