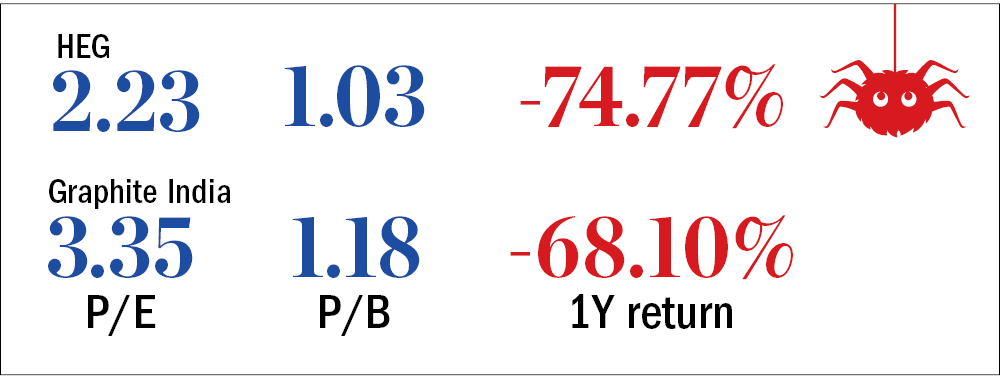

HEG, Graphite India

HEG and Graphite India manufacture graphite electrode, which is used in steel-making. They hit the jackpot when China introduced stringent pollution-control norms and as a result, the production of electrodes decreased. Electrode prices went all the way from $3,000 to $15,000/metric tonne. This caused many steel companies to over-stock electrodes. Hence, the demand and the price of electrodes went down, causing the stock prices of these two companies to crash up to 81 per cent after having gone up 10 times in the last couple of years.

While the managements of these companies are still optimistic about their future prospects, investors should be cautious. Don't go just by the cheap valuations of these stocks.

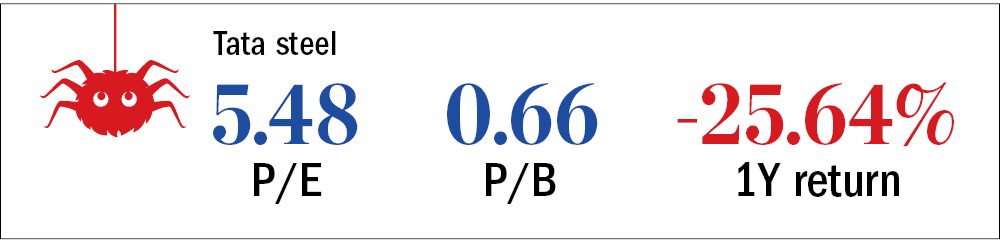

Tata Steel

With a consolidated installed steel capacity of 34 million tonnes (MT), Tata Steel is one of the largest steel manufacturers globally. Of the 34 million tonnes, 19.6 million tonnes is domestic production and this is the segment that actually does well and is a higher margin business. This results in the domestic business commanding a lion's share in the company's operating numbers and net profits.

Even though the company seems to be at an attractive price point, it is probably there due to several headwinds. Steel prices have been muted due to weak demand both domestically and globally. The automobile sector, which is a major buyer of steel, has been going through a slowdown of its own.

Tata Steel's European operations (Tata Corus) are another major drag on the company's financials due to the sustained weakness in that market. The company's consolidated gross debt stands at 17,864 crore, which the management is trying to reduce by monetising assets. This is another factor weighing in on the stock.

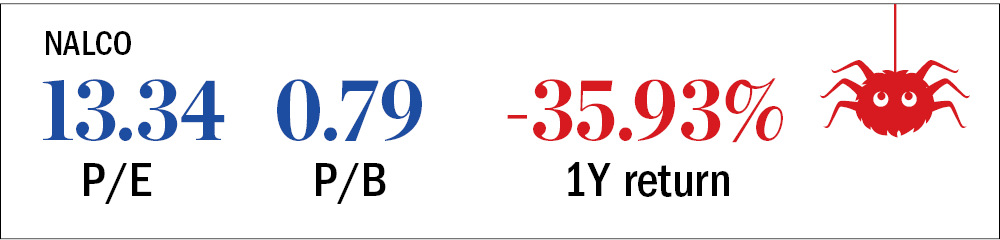

NALCO

NALCO is the world's lowest-cost producer of alumina and bauxite. It has a 24 per cent domestic aluminium market share. However, the prices of alumina and aluminium have fallen globally, putting pressure on aluminium producers. The US-China trade war has caused metal prices to be on a continued downtrend. This is in addition to the threat of increasing aluminium imports, which stood at 59 per cent of the total FY19 consumption. However, the management is positive about higher demand in the future from sectors like automobiles, construction and power.

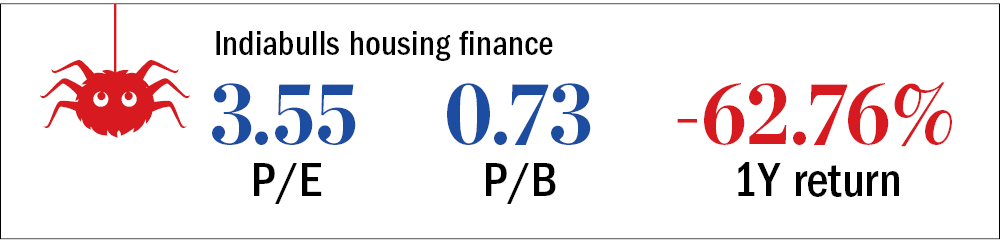

Indiabulls Housing Finance

Indiabulls Housing is one of the biggest wealth destroyers of 2019. In the last one year, the stock has lost 80 per cent. The company has been hit due to the woes in the NBFC space. Its June 2019 quarterly numbers painted a grim picture, with its net profit collapsing about 24 per cent YoY. There have been fund-diversion allegations against the promoters as well. The company's proposed merger with Lakshmi Vilas Bank has been turned down by the RBI. The company's credit rating has also been downgraded. Given all these uncertainties, the stock may prove to be a value trap.

Ask Value Research ![]()