ULIPs and endowment plans are very popular in India. Knowingly or unknowingly, most people end up buying these two types of policy. They appear to be simple, transparent and highly beneficial. This article is an earnest attempt by us to dispel the myth (or shall we say hype?) around ULIPs and endowment plans. We will also tell you what are the best alternatives.

What are ULIPs and Endowment plans?

They are both insurance cum investment products. Neither of them is recommended as they offer a sub-optimal combination of insurance and investment.

ULIP is a market-linked insurance scheme where the scheme invests in equity or debt oriented schemes, whereas endowment plans offer a guaranteed benefit called the sum assured.

Why are they so popular?

Three reasons came to our mind and we think you will agree with at least one of the reasons.

- A lot of Indians buy insurance in haste and that too for the sole purpose of saving tax and they do so without fully understanding the products.

- Often the insurance agent is a neighbour, or a friend or, even worse, a relative. It’s kind of difficult to turn them down. So, we end up buying an endowment or an ULIP without giving it much thought. Also, these policies are pushed hard by agents as they involve attractive commissions.

- Many people see insurance as an useless expense and hence they think it’s better to just buy a product that will give some return as well. Just like they fail to see the effect of inflation, they fail to see the sub-optimal returns from these products.

To develop a deeper understanding of why people opt for these policies, you should definitely read this interesting article by Vivek Kaul.

What’s wrong with them?

Neither do they provide adequate insurance, nor a good investment solution. Let’s explore the point by looking at the two purposes separately.

Insurance

Most often, people fail to fathom what kind of insurance coverage they need. For instance, in a family of four where you are the only earning member, a life insurance coverage of Rs 5 lakh (see example below) is simply not enough in the event of your untimely death. The effect is more pronounced if you haven’t left them much inheritance and/or if you had loans running. And, then there’s inflation, which will eat away your wealth. To put things in perspective, if a term plan cover of Rs 50 lakh costs you Rs 7000 per annum, it will cost you Rs 5 lakh per annum in case of an ULIP.

Investment

The biggest factor that goes against them are the exorbitant charges. A significant percentage of the premium you pay, particularly in the initial years, are deducted in the form of various fees and charges, the biggest component being distributor commissions. This reduces the amount of your premium that is actually invested to generate returns. Over a long period, that makes a huge impact on the total wealth you are able to accumulate. Below we have presented one aspect of ULIP, its numerous charges.

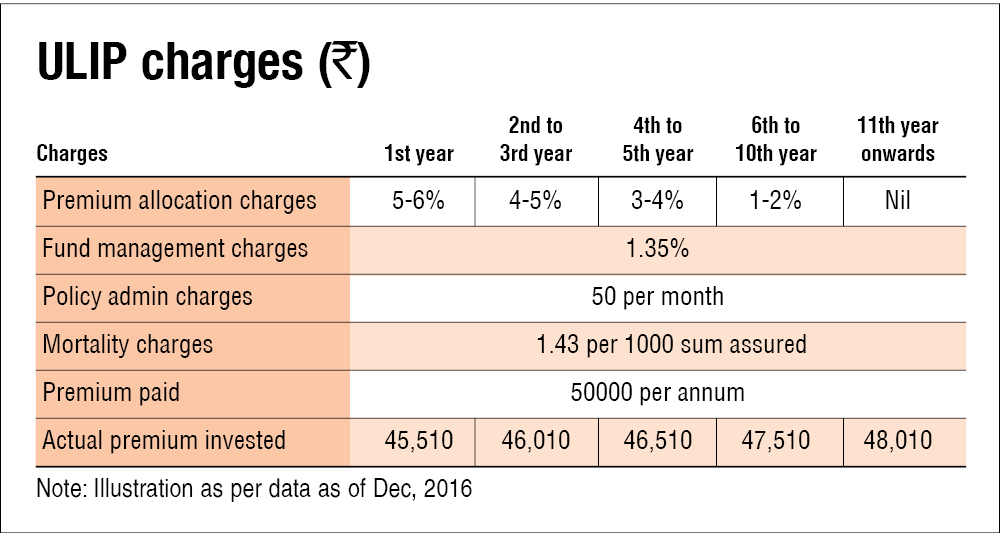

ULIP

Age: 35

Annual premium: Rs 50,000

Sum Assured: Rs 5,00,000

The table below enlists a set of charges that are levied by ULIPs. Now, mind you that these charges aren’t exactly hidden. You will find them on your policy papers but probably wouldn’t give it much importance. The actual invested amount is after deducting the following charges which make up almost 7% of the total invested amount.

So, in 10 years you have paid Rs 5 lakh. However, the actual invested amount, after deducting all the aforementioned charges, will be around Rs 4.68 lakh.

So what are the alternatives?

It is always better to keep insurance and investment separate. If you have financial dependents, the first thing that you should do is to buy a term insurance with an adequate cover. Put the rest of the money in one or two good diversified equity funds. But, what if you are risk averse? In that case, we would suggest you to stick to a term plan & good old PPF. It will still give you better returns than an endowment plan.

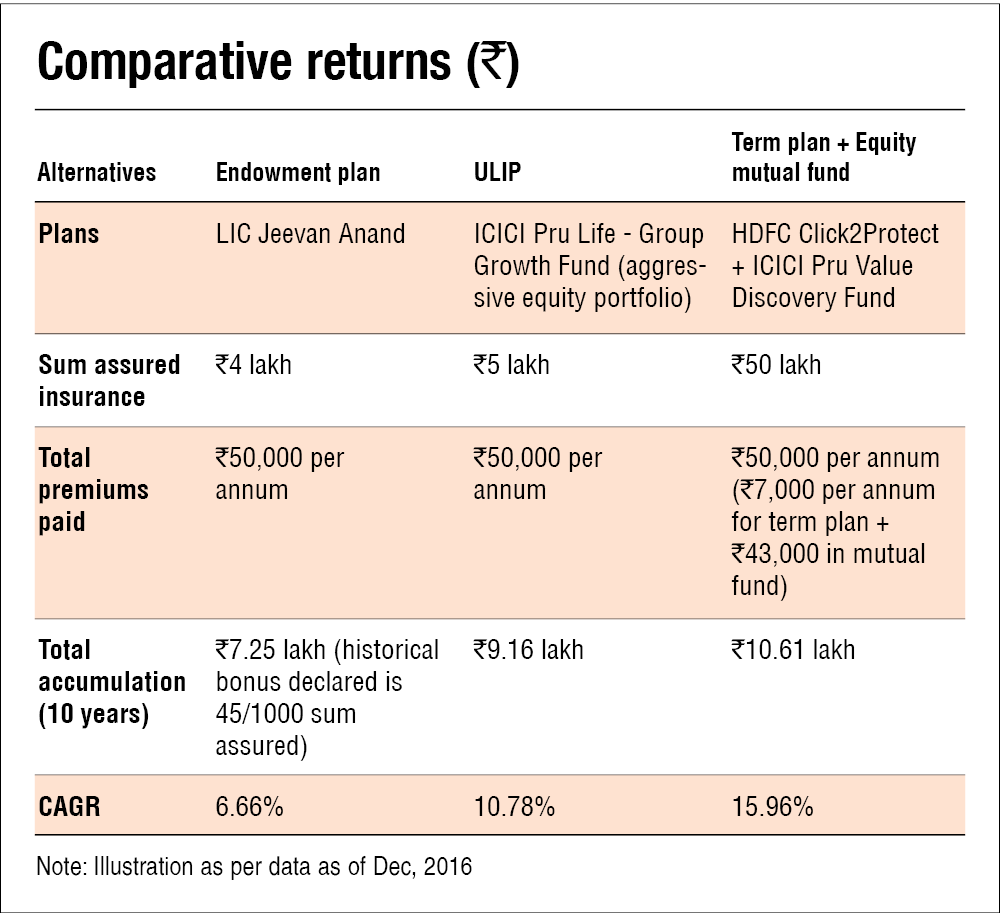

A number is worth a thousand words

We don’t want you to take our word (or anyone else’s for that matter) for it. So, let’s examine the shortcomings through an illustration.

In the table , we have taken the 3 possible options - buying a ULIP, buying an endowment plan, and buying a term plan+equity mutual fund. The table illustrates what kind of returns you would get on each in the last 10 years (based on historical data). For the sake of parity and returns, we have considered the best performing products from each category.

Inference

The table above is pretty self-explanatory. Firstly, in the third option, you get an insurance coverage that is ten times more (50 lakhs) than that of an ULIP. Secondly, the return is significantly better in the third option. So, the verdict seems quite clear.

Advice

Insurance is an expense and it should be treated like an expense. Don’t mix insurance with investment. Mixing the two will give you less than moderate returns from both.

What can you do now?

- There is something called the free-look period that is valid for 15 days. If you are not satisfied with the insurance you bought, you can return it within 15 days of buying and get a refund. Click here for more details.

- If your policy is older than 15 days, we would suggest you to return it, bear the corresponding loss and buy a term plan immediately. Rest of the money, as we said earlier, you should invest in well-diversified equity mutual funds.

This article was originally published in February 2017.

This article was originally published on June 15, 2020, and last updated on September 29, 2022.

Ask Value Research ![]()