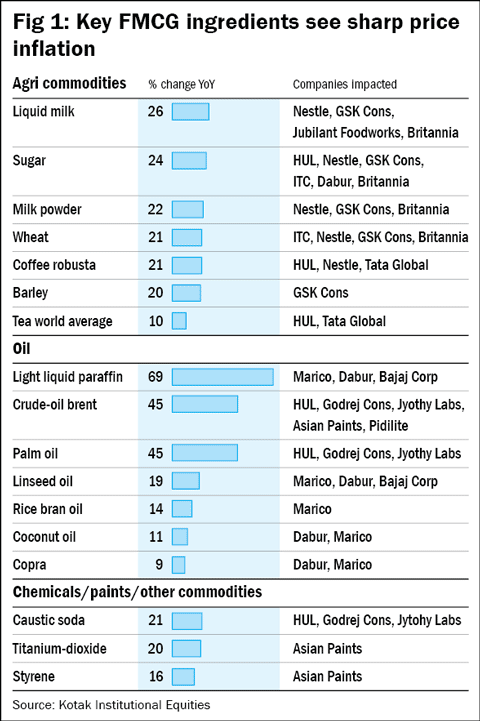

About 65 per cent of the 40 commonly used raw materials of the FMCG industry are witnessing price inflation. That's the alarming analysis by Kotak Institutional Equities. Agri commodities have witnessed high levels of inflation: milk is up 26 per cent (YoY); sugar, 24 per cent; wheat, 21 per cent; and barley, 20 per cent. Coffee is also up 21 per cent.

Then there are non-food inputs. Crude is up 45 per cent (YoY). Palm oil is up 45 per cent, too. And titanium-dioxide is up 20 per cent.

Figure 1 mentions some key FMCG ingredients that have gone up in the last one year, along with the names of the companies that could be impacted by this price rise.

The impact on companies

The inflation in agri commodities is expected to hit companies like Nestle (milk powder is a key ingredient, as is coffee, in Nescafe), GSK Consumer (Horlicks uses barley), Jubilant Foodworks (wheat), Britannia (wheat, sugar, milk) and Tata Global Beverages (coffee).

If sustained, higher input costs will hurt the margins of FMCG companies. Of course, there is the matter of forward covers, level of inventory and timing of purchases that will determine how each company is affected differently.

What is different now from the other usual times when input prices go up (as they have gone up in the past) is that whereas most companies have passed on the price rise to consumers in the past, the same strategy may be a tad difficult to execute today. This is because the demand environment for FMCG products has started to show signs of weakness on account of the demonetisation drive. Taking a price hike to pass on higher input prices at this point in time is something that FMCG companies may find extremely difficult to do.

Companies that are expected to take the maximum brunt of the input-price inflation include Jyothy Laboratories, Pidilite Industries, Marico, Manpasand Beverages, Asian Paints, Britannia and Jubilant Foodworks. Jyothy, for instance, is expected to see its margins dip from 15.7 per cent for FY18 to 13.5 per cent in the same year after input-price inflation. Pidilite could see its margins decline from the earlier estimates of 22 per cent for FY18 to 19 per cent.

Other companies that are not expected to be hit as much include Nestle, Page Industries, ITC, Titan, HUL and Dabur. The table highlights the risk to the margins and earnings per share of FMCG companies as a result of input-price inflation.

The weakness in demand and the inability of FMCG firms to pass on higher costs to consumers could have another casualty: new launches. In an already depressed environment with a lower surplus going around, new launches could face launch-budget tightening - something no FMCG company wants to go to the market with.

Why is the price inflation alarming?

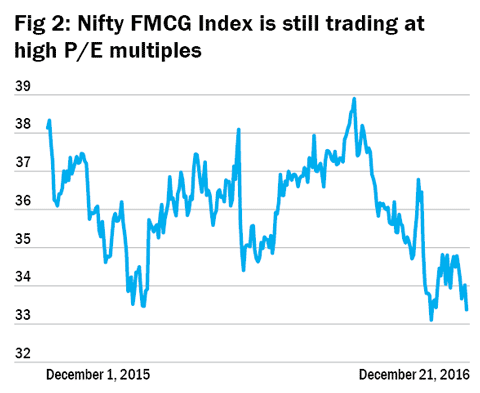

The market doesn't seem to have factored in this sustained higher input-price inflation and the limited ability of FMCG companies to take price hikes. This is evident from the continued high P/E of the FMCG index (see Figure 2).

This story appeared in the January 2017 issue of Wealth Insight.

Ask Value Research ![]()