Taxes can be saved through insurance, fixed-income options or equity-linked investments like ELSS. However, it is extremely important to pick up the right tax-saving option that matches your investment objective and horizon. Here are a few pointers that would help you to pick the right tax-saving options this year.

Saving tax through insurance

Buying an insurance cover is not always the smartest way to save taxes under Section 80C. Especially when you are buying life insurance plans with investment element in them. Such plans offer very little life insurance cover. They are also not an ideal investment option as they mostly offer modest returns. Also, getting rid of these plans may result in losing a part of the money invested. However, most taxpayers accumulate such plans over a period during their last-minute shopping. You can stay away from such plans this financial year.

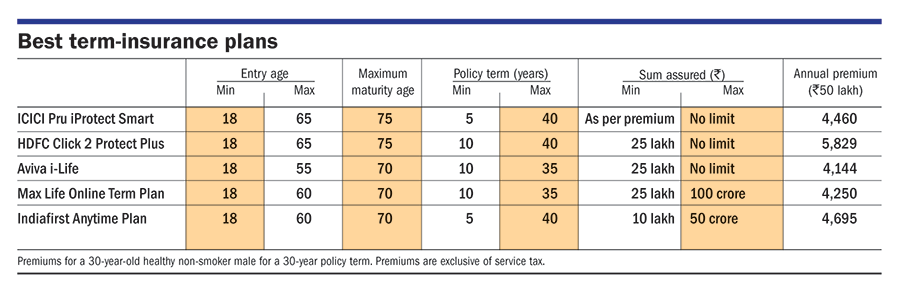

Life insurance is meant to support the dependents of an earning member. However, when the insurance cover is not large enough to take care of the financial needs of dependents, the whole purpose is defeated. That is where term insurance products come in. Term insurance plans have a very low premium and you can buy an adequate life insurance cover by paying a relatively low premium in them. So, say no to all other insurance products like traditional and non-traditional plans like endowment, whole life, money back, Unit Linked Insurance Plan, Unit Linked Pension Plan, etc this year.

Another insurance product that offers tax savings is health insurance. It is important to opt for a health insurance policy not to save taxes but to protect oneself from the financial hardship that ill health could bring. Section 80D of the Income Tax Act allows deduction of health insurance premium of up to ₹30,000 for senior citizens and up to ₹25,000 for insurance of self, spouse and dependent children. Additionally, a deduction of ₹30,000 is available for buying health insurance cover for parents.

Fixed-return options

The Public Provident Fund, National Savings Certificate, five-year bank fixed deposits are some fixed-return tax-saving options that can help you to reduce your tax liability. These instruments work on the simple premise of providing a fixed rate of return for fixed tenure for which the savings are locked in. Now you can also invest in the Sukanya Samriddhi Yojana and save taxes. This scheme, as the name indicates, is meant specially for saving for the girl child.

When selecting any of the savings options as a tax saver, keep in mind not just the returns but also the lock-in period and the tax treatment at the time of maturity. For instance, in the case of the PPF, at the time of maturity, the entire sum is tax free. However, in case of the NSC, at the time of maturity, the gains are taxed.

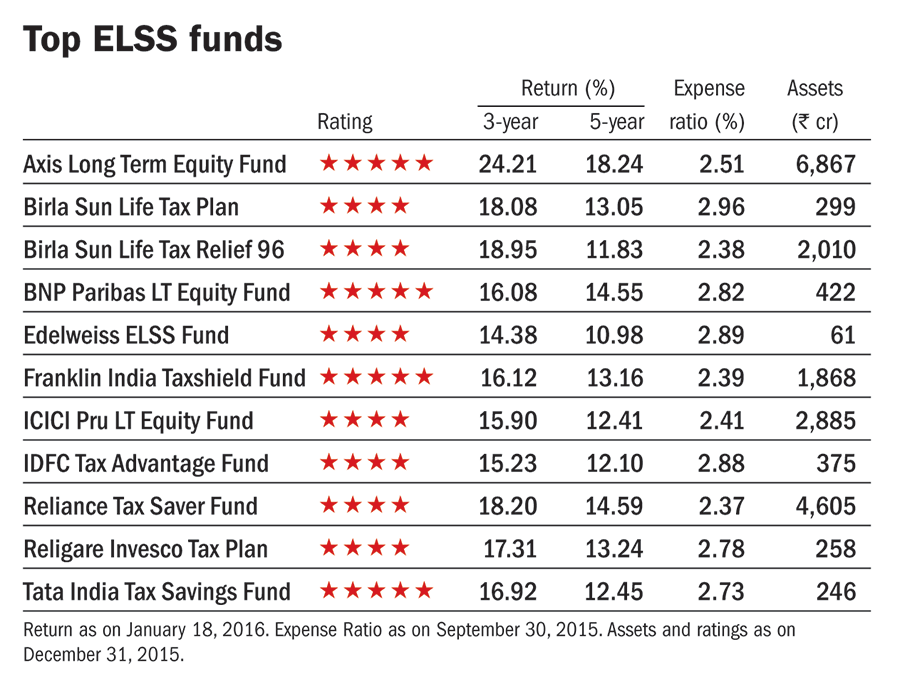

ELSS: The smart way to save tax

Among all the tax-saving options, there are just three instruments that have an equity exposure: the NPS, the Rajiv Gandhi Equity Savings Scheme (RGESS) and equity-linked savings scheme (ELSS).

A fund qualifies to be an ELSS if it invests more than 65 per cent in equity, has a three year lock-in on investments and has the necessary approval from tax authorities. Moreover, an ELSS has a three-year lock-in as compared to the minimum five-year lock-in in the case of life insurance and 15 years in the case of the PPF. This makes ELSS the preferred tax-saving choice, which can also offer better returns.

The three-year lock-in is long enough to be the right time-frame for equity investments, damping most of the risk. The ELSS option comes under Section 80C.

Among ELSS, RGESS and the NPS, ELSS scores highly over the other two. This is because over the long term you can get better returns from it than the other two.

The NPS has limited equity exposure, which is also restricted. With the NPS, however, you can choose your asset allocation - how much you want to invest in debt and how much in equity.

The RGESS was aimed at first-time equity investors but the scheme has failed to take off. The government is mulling making changes to it.

Finally, don't let these options confuse you. Always pick an instrument that suits both your financial needs and risk profile. For example, you should pick an option with the least lock-in period if you have cash flow issues. However, that doesn't mean that you should automatically pick up ELSS as it has the least lock-in period. If you don't have the stomach for risk, your choice should be the five-year tax-saving fixed deposit.

Also read: How much more do you need to invest?

This article was originally published on March 17, 2016.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()