Tax planning is a last minute exercise for many taxpayers. For many of them, the last three months of the financial year (January to March) are the tax-planning months. However, some individuals love to push the whole exercise to the last two to three weeks of the financial year. Now, they must be running around to finalise their tax-saving investments. Sadly, most of them end up with wrong products, mostly expensive insurance plans. Ideally, tax planning should start at the beginning of the financial year and investments should be made regularly through the year. However, if you are late this year, don't lose heart. Help is here. A little bit of homework can save a lot of heartburn later. Read on.

To begin with, the sole objective of tax planning should never be saving taxes. Tax planning is more about maximising wealth by the optimum use of tax-saving avenues than simply putting money in some tax-saving products. In fact, it should be in sync with your other long- and short-term goals.

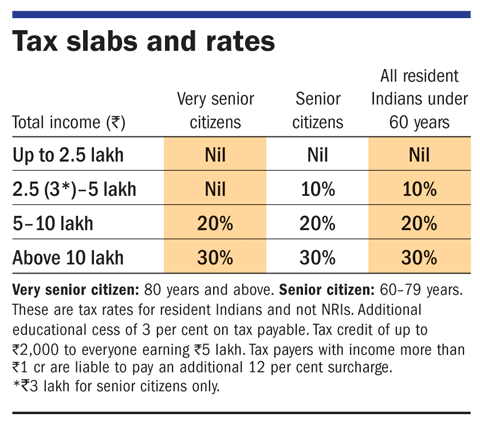

Know your tax liability

There are a number of factors that decide whether you have to file your income-tax return; every person who has earned an income in 2015-16 is not liable to pay income tax. The factors that determine whether you need to pay income tax include how much you have earned, the source of income as well as your age. For example, if you are earning less than ₹2.5 lakh a year, you don't have to pay any income tax.

For most of us, identifying our tax bracket is pretty straightforward. Using the table on tax slabs and rates, choose your filing status and your gross income. Then, check in which tax slab you fall to know your tax liability. There is, however, another criterion that decides your income tax: your residential status in India. It could be resident Indian, non-resident Indian (NRI) or not ordinarily resident (NOR). The applicable income tax varies for each of these categories. Also, tax rates are different for senior and very-senior citizens and those under 60 years of age.

The next step is to arrive at your gross 'taxable' income. This is easy as long as you have a single source of income. However, some individuals will have multiple sources of income. For instance, a salaried person may have income from investments that pay out dividends or a property that is let out on rent. Such additional sources is treated as an income source. To calculate tax, income can fall under five heads: income from salary, income from house property, income from profits and gains of business or profession, income from capital gains, and income from other sources which are outside the other four sources. The income from other sources includes interest income from bank deposits or income from lottery.

Now come tax-saving investments or expenses. There are several options available in the form of savings, investments and even expenses against which you can claim tax deductions and reduce your income-tax liability. With a little bit of homework, an individual can use one or more of these options to reduce his tax liability and create wealth in the process.

Know how much you need to invest

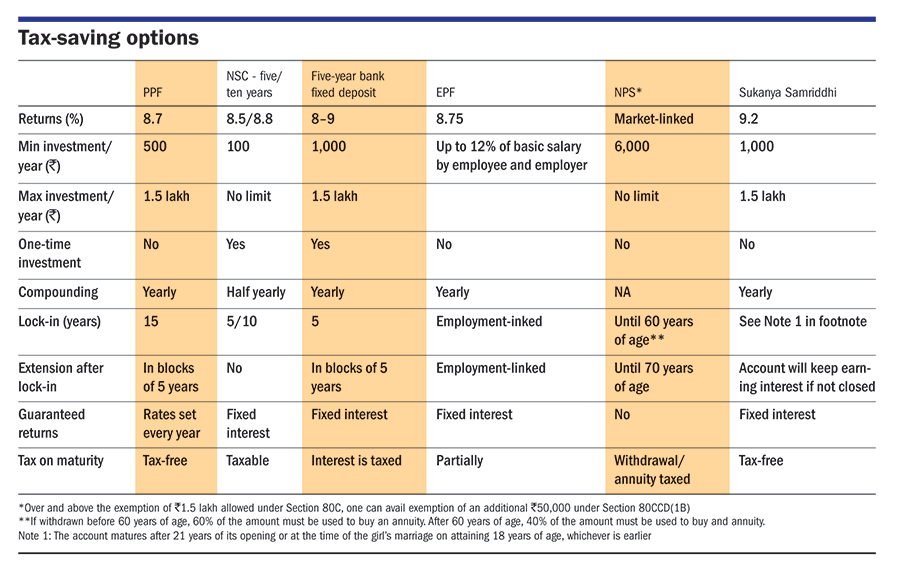

Most tax payers know that they can save up to ₹1.5 lakh under Section 80C of the Income Tax Act. They claim a deduction of ₹50,000 on contributions to National Pension Scheme (NPS) under Section 80CCD(1B). Their NPS contribution qualifies for a deduction under Section 80CCD(1) and so on. Often, many taxpayers find out after the whole exercise that they have invested more than they needed to save taxes. The trouble with tax-saving investments is that they all come with mandatory lock-in period. once you invest in them, you need to stay invested for a stipulated period. This problem can be avoided if you find out what contributions or expenses of yours qualify for tax deductions under Section 80C. For example, most salaried employees have monthly contributions to the EPF or the NPS. These should be deducted from ₹1.5 lakh permitted under Section 80C to find out how much they can invest more to save taxes. Similarly, if you have health or life-insurance plans, you can deduct the premium paid under Section 80C and 80D. Now, if you know how much you actually need to invest, you can turn your attention to the investment options.

Tomorrow: Tax planning 2016 - II will discuss the best tax-saving investments.

Also read: Best tax-saving options for you

This article was originally published on March 16, 2016.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()