Income tax is a complex subject. Our goal here is to familiarise you with the taxation aspects of only that income (or losses) that you may have from your investments, and the ways and means available to use your investments to reduce the amount of tax you have to pay. There are various tax saving investments available at your disposal. We recommend that you consult your tax advisor for details on the tax laws that might be needed to actually file your returns.

Paying taxes on investments

Of the various types of investments discussed here, mutual funds and stocks are capital assets, and gains from the purchase and sale of these are called capital gains. If you lose money on them, then these are capital losses. Capital gains or losses occur only when you actually sell an investment.

Dividends paid by funds or shares are dividend income, while interest earned from bank, post office or other such deposits is called interest income.

Here's an overview of the taxation situation for each of these:

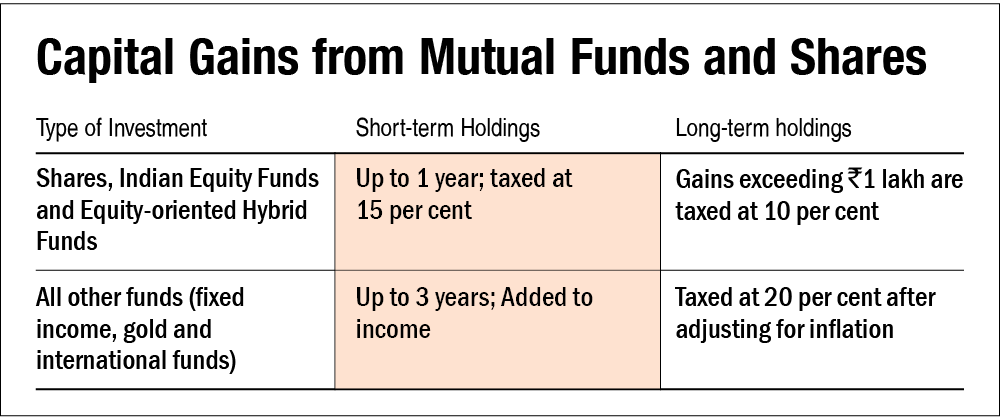

Tax on mutual funds

Non-equity funds are treated as long-term capital assets if held for more than three years. Long-term capital gains tax is payable at 20 per cent with indexation benefit on the realised gains. Gains on investments in non-equity funds held for up to three years are added to income and taxed as per the applicable slab rate.

Equity funds are treated as long-term capital assets if held for more than one year. The long-term gains are taxed at 10 per cent without indexation. Short-term capital gains from equity funds are taxed at 15 per cent. Dividend income is now added to the income of the receiver and taxed as per the applicable slab.

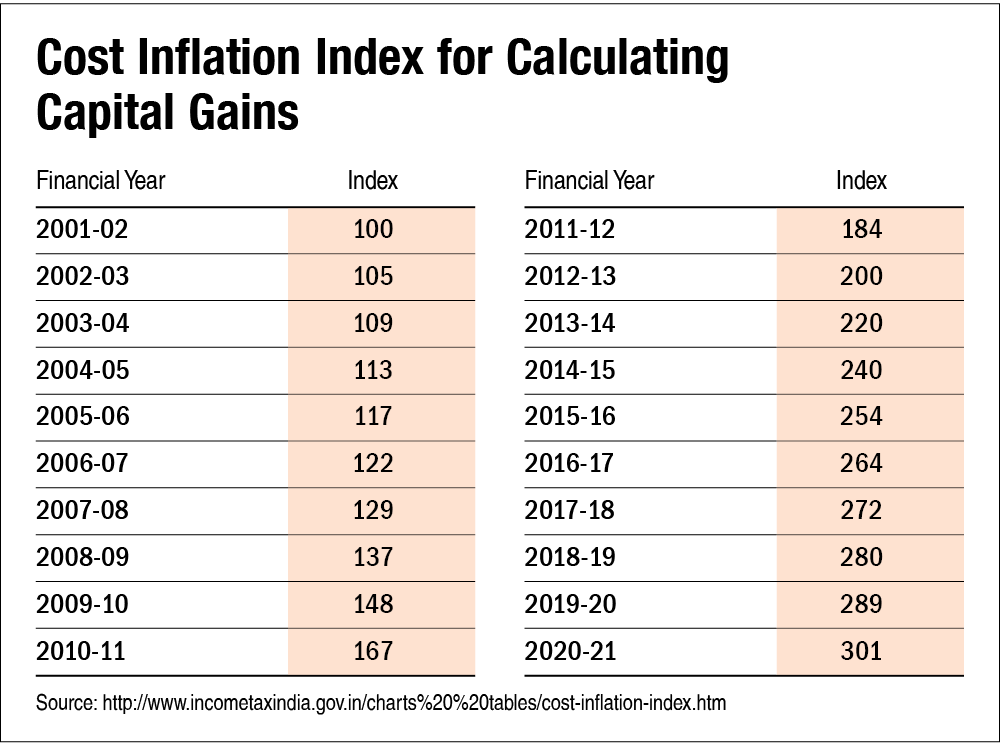

As an example, say you have made an investment in a non-equity fund, in the year 2002-03 of Rs 1 lakh and sold it for Rs 5 lakh in 2018-19. Your capital gains tax will be adjusted for the inflation adjustment factor, i.e., 280 divided by 105, which is 2.67. By this method, your cost of the investment will be deemed to be higher by 2.67 times than what it actually was, that is, it will be Rs 2.67 lakh. Thus, your profit will be Rs 2.33 lakh and the tax payable will be Rs 46,600.

Interest income

Interest income is simply added to your income and taxed according to whatever tax bracket you are in.

Section 80C investment options: Saving taxes through Section 80C

Section 80C offers a window of tax saving investment opportunities for up to Rs 1.5 lakh investment in each financial year. This benefit is available to everyone irrespective of their income levels. If you are in the highest tax bracket of 30 per cent, the investment of Rs 1.5 lakh under this section will save you Rs 46,800 each year. The various financial products that qualify for Section 80C benefits are as follows:

- Life insurance premium payment

- Repayment of home loan principal

- Your contribution to Employees Provident Fund (EPF) (employers' contribution is not deductible)

- Tuition fees for up to two children. However, any payment towards any development fees or donation to institutions is excluded. Also, the aggregate deduction under section 80C should not exceed the overall Rs 1.5 lakh limit.

- Contributions to the Public Provident Fund (PPF)

- Investments in the Senior Citizens Savings Scheme

- Savings in notified term deposits in scheduled banks with a minimum period of five years under the bank term deposit scheme, 2006

- Savings in post office time deposits with 5-year lock-in

- National Savings Certificate, five-year government-backed security available at post offices

- Investments in tax planning mutual funds (ELSS)

- Investments in pension plans

Also read:

Make your tax-saving investments equity-based

An overview of 6 popular tax-saving options

Investing in a tax-saving fixed deposit

This article was originally published on March 05, 2021.

Ask Value Research ![]()