Of all the types of diversification, sectoral diversification is the hardest to achieve simply because the correct mix is the hardest to figure out. Sectoral diversification is about not having too much exposure to any one sector. However, there are two attendant problems. One, how much is too much? And secondly, how little is too little?

The answer to these questions may surprise you. Ideally, sectoral diversification should not be your problem at all. You should be investing in well-chosen diversified equity funds with a good track record and that's that. Once you have done that, you shouldn't bother about whether 30 per cent of your funds are in financial services companies or 10 per cent in infrastructure. You invest in a mutual fund so that such decisions can be off-loaded to the fund manager. Sectoral allocation is fundamentally different from say, asset class diversification. How much equity should your portfolio have is a decision that you have to take based on your own needs. But which sector that equity should come from is your fund manager's decision based on his or her judgement of where the market is going.

If you still want to know how a fund allocates across sectors, make sure you look at its allocation during different phases of the economic cycle. The way it allocates across sectors also reflects the fund manager's experience and expertise.

So why are we discussing sectoral allocation at all? There are two reasons. One, it is relevant in the light of the scourge of sector and theme funds. And secondly, it is helpful for investors looking to invest in equity on their own.

Even though they are in a Sebi-enforced retreat nowadays, sector and thematic funds have been very actively sold in the past, so much so that those who have invested in specific periods when a sector was the flavour of the day have ruinously high exposure to specific sectors. Take for instance, if you were investing in new mutual funds in 2006-2007, it is likely that you had a lot of money in the infrastructure sector. Before that, at the turn of the millennium, between 1999-2001, there was the technology phase and so on. Since these funds have a feature-driven identity, many investors tend to get attracted to them. They start betting aggressively on a sector before realising that their allocation is too high in a single sector.

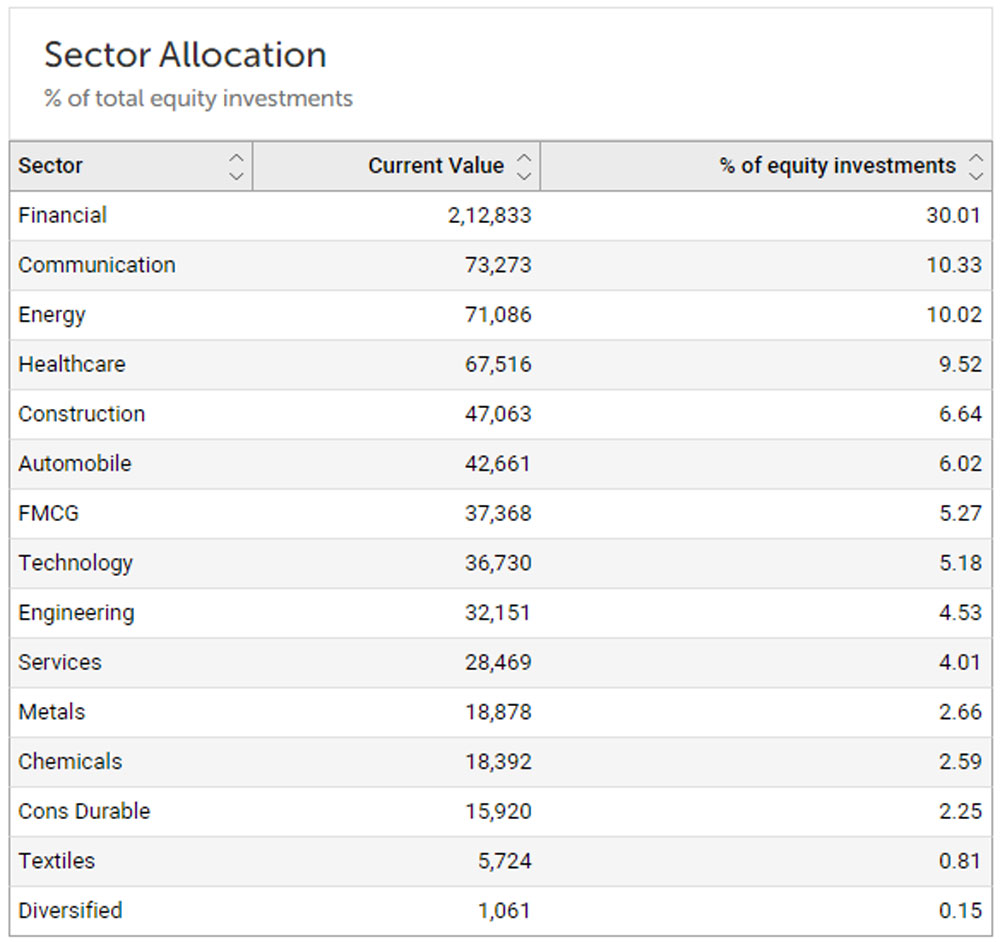

Sectoral diversification is especially important for fund investors who also buy stocks directly to achieve, as these can skew their sectoral allocation. In terms of tracking, this is not a problem because ValueResearchOnline can track equity investments too. My Investments can show you where you stand. Go to the Analysis tab here and scroll down to Composition under which there is a tab for Diversification. Click on this, and under that you will find a table for Sector Allocation. Here you can see what proportion of your portfolio is invested in each sector.

But really, this doesn't completely solve the problem. When is the allocation in a sector too high and when is it too low? There's no fixed answer to this question, but one good rule of thumb is that no sector should be more than 30-35 per cent of your portfolio, and the top three sectors should not add up to more than about 50-60 per cent.

To give yourself an idea of where the markets are, you could also take a look at the sectoral allocation of leading funds and indices. This could act as a reference for you to evaluate the sectoral allocation of your own portfolio.

This article was originally published on October 30, 2020.

Ask Value Research ![]()