Anand Kumar/AI-Generated Image

Anand Kumar/AI-Generated Image

Summary: Most investors don't deliberately put most of their money with one fund house. It just happens. And when it does, the several funds you own can turn out to be a single investment philosophy wearing different wrappers, a risk that only shows up when the style falls out of favour.

Most investors do not deliberately put most of their money with one fund house. It just happens. Perhaps your bank recommended two funds from the same AMC. Perhaps one fund did well, so the next came from the same brand because the name now felt safe. We all have our Zara, our Nike, the label we reach for without thinking.

Mutual funds do not reward that loyalty. Buy several funds from the same fund house and you may be less diversified than you think. The several funds you own can turn out to be a single bet, wearing different wrappers.

One fund house, one investment philosophy

Every fund house has its own way of investing. The same research team supports every scheme. The same chief investment officer shapes the process. The same beliefs about markets and valuations run through every fund manager in the building. So different funds from the same AMC can end up moving in the same direction at the same time.

When that style suits the market, several funds from the house outperform together. When it falls out of favour, several struggle together. You already accept this idea with investment styles such as growth and value, or with sectors such as banking and technology. It applies one level up, at the fund-house level too.

This happens more often than you would think

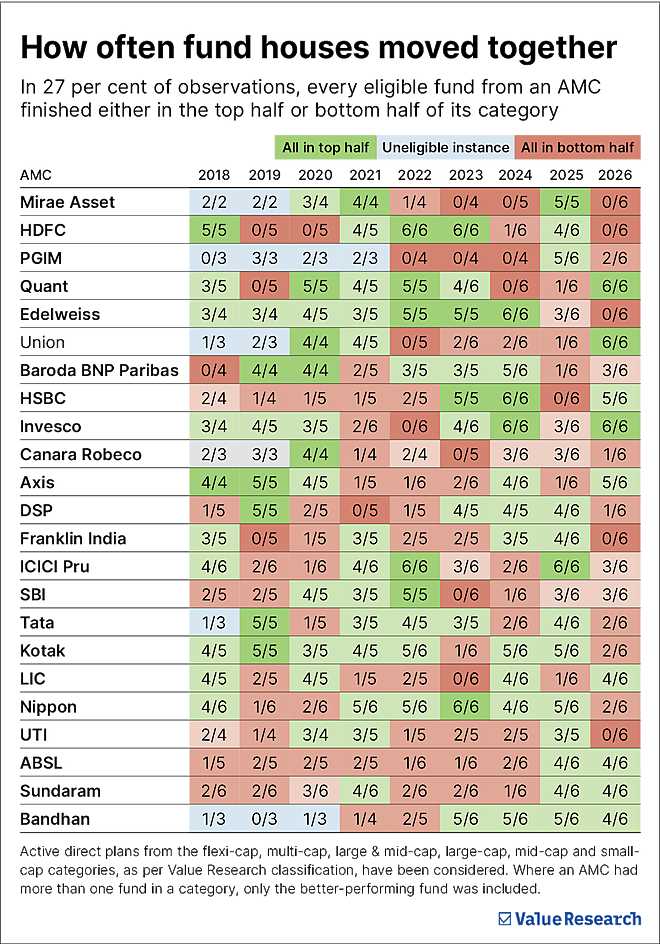

We took six diversified equity categories, flexi cap, multi cap, large cap, large and mid cap, mid cap and small cap, and ranked every fund against its category peers on calendar-year returns from 2018 to June 25, 2026. Then, for every year a house ran at least four funds across these categories, we asked one question. Did they all finish on the same side of their category rankings, either all in the top half or all in the bottom?

Twenty-three AMCs gave us 193 such observations. In 52 of them, every eligible fund from the house landed together, all in the top half or all in the bottom. That is 27 per cent. If performance across categories were independent, chance alone would produce a clean sweep like that no more than 12.5 per cent of the time, and usually far less.

So open your portfolio and count fund houses, not just funds. If most of your money sits with one AMC, you may own the same investment view several times over.

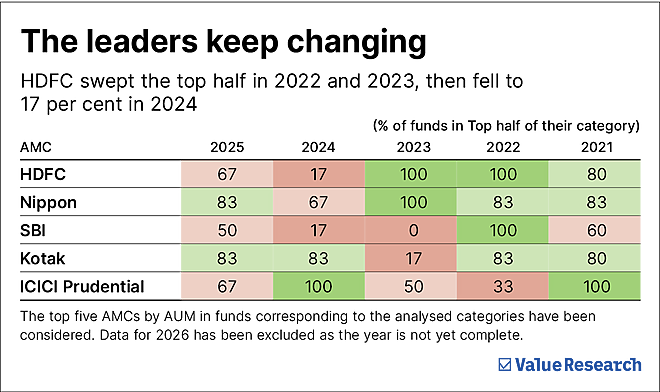

The best fund house rarely stays the best

The obvious response is to find the one exceptional AMC and put everything there. But investing does not work that way, because no house stays exceptional for long. The houses leading the rankings today are often very different from those that led a few years ago. Some of today's best performers sat among the weakest in the previous period. Some former leaders have fallen sharply since. Investment styles move in and out of favour, and a house that looks brilliant in one market cycle can look ordinary in the next.

What the risk is, and what it is not

Concentration in one house sounds like it should be a solvency risk. It is not that. If an AMC runs into business trouble, your investments do not disappear. Mutual fund assets are held separately for investors and are not part of the AMC's own balance sheet.

The real risk is subtler. You may believe you own a diversified portfolio because you hold several funds. But if they all share the same investment philosophy, they can behave very similarly when markets turn difficult. The most extreme example came in 2020, when credit problems forced the closure of six debt schemes at Franklin Templeton. Investors who held several of those schemes discovered their diversification was not as broad as they had assumed.

Pick funds, not fund houses

So do not impose crude limits such as "no more than two funds from an AMC." Instead, choose funds on two things: your asset-allocation needs, and each fund's ability to deliver consistent returns for the risk it takes. Diversification across houses tends to follow on its own.

Then run a quick check. Group your investments by AMC and see where your money sits. If one house dominates your active equity portfolio and its funds share a style, ask whether you truly own different strategies or simply different versions of the same one. There is no magic number. Two or three houses with genuinely different approaches diversify you better than five that all think alike.

And there is no need for drastic action. Direct future SIPs and fresh investments towards the houses you are light on, and let time solve a concentration problem more efficiently than tax-triggering sales ever could.

Running that check, seeing where your money actually sits, whether your funds truly think differently or just wear different labels, is exactly what Value Research Fund Advisor does. It looks inside your portfolio so you are not discovering your concentration problem at the wrong moment.

Find out where you actually stand.

Ask Value Research ![]()