Anand Kumar

Anand Kumar

Summary: Market crises don’t just create panic; they reveal what your portfolio is really made of. Some stocks recover, others unravel. The key lies in knowing which ones you own and why.

On Thursday (March 19, 2026), the Sensex fell 2,497 points. Oil crossed $119 a barrel. The India VIX spiked 22 per cent in a single session. I have been doing this for over three decades, and I can tell you, the phone calls and emails that arrive on days like this follow a pattern. The questions are never about the market. They are about specific stocks. “Should I sell this one?” “Is this company going to survive?” “I bought this two years ago, and I have no idea what it actually does.”

That last one is the one that worries me.

Because here is what a crisis does, quietly, while everyone is watching the index: it sorts every portfolio in the country into two piles. In the first pile are companies that wobble and recover. Their stock prices fall with the market, sometimes sharply, but the business underneath is fine. The balance sheet was clean before the fall. The management was trustworthy before the fall. The earnings were real, not a product of creative accounting or favourable one-offs. When fear subsides, these companies get bought back. The loss becomes a memory.

In the second pile are companies that wobble and keep falling. Their stories sounded compelling enough when the markets were calm. A hot sector. An exciting narrative. A promoter who gave confident interviews on television. But these companies were carrying risks that the bull market managed to hide. Excessive debt that looked manageable when sentiment was high. Related-party transactions that nobody bothered to scrutinise. Governance problems that only become visible when the environment turns harsh. For these companies, the crisis is not a dip. It is a reckoning.

The investor I feel most concerned about this week is not the one whose portfolio has fallen the furthest. It is the one who genuinely does not know which pile he is in. He bought some stocks on a colleague’s tip. A few others he researched himself, partly. Some he inherited from an earlier phase of his investing life, when his standards were different. He looks at his holdings and feels uneasy. Not because he knows there is a problem. Because he cannot tell whether there is one.

That uncertainty is worse than a known loss. A known loss has a number. You can look at it and decide what to do. An unknown risk just sits there, feeding anxiety every time you open your portfolio app.

I have believed for a long time now that the most important work in stock investing happens before you buy anything. The question of which companies to own is inseparable from the question of which companies to reject. And if I had to choose between the two skills, I would choose the second one. The ability to identify businesses to avoid, the overleveraged, the governance-compromised, the ones where the promoter’s interests and the minority shareholder’s interests quietly diverge. That protects you in ways that even excellent stock-picking cannot. One catastrophic holding can undo years of patient gains.

Let me tell you what this looked like in real time, this week. Companies with clean balance sheets and genuine cash generation fell with the market. Of course they did. But their economics did not change. A well-run consumer company or a conservatively financed private bank is worth roughly what it was worth three weeks ago. The price moved. The value did not. Meanwhile, companies that had been running on borrowed confidence, leveraged plays with stretched balance sheets, story stocks where the narrative was doing all the work because the earnings certainly weren’t: those fell harder, and some of them will not recover to their previous levels.

The sorting happened in real time. If you knew what you owned, you could watch it and stay calm. If you didn’t, you couldn’t.

At Value Research Stock Advisor, our research process begins with elimination. Out of roughly 4,500 listed companies in India, our filter rejects the overwhelming majority before any portfolio consideration begins. The filter is designed to catch exactly the risks that weeks like this one expose: governance problems that accounting numbers cannot fully capture, debt levels that become dangerous when credit tightens and business models that depend on narrative rather than cash flow. Most stocks do not survive this process. That is the point.

I also want to tell you about a structural change we have made, because the timing makes it relevant. Over the past two years, our analysts have noticed that whenever they build the ‘Dividend Growth Portfolio’, the shortlist overlaps heavily with the ‘All-Weather Portfolio’. Same reasoning. Businesses that grow their dividends year after year do so because they generate real cash, keep their debt manageable and maintain the kind of financial discipline that holds up when conditions get difficult, something we have discussed in the previous edition of Wealth Insight in our cover story. Those are also exactly the qualities that define an all-weather business.

We should have acted on this overlap sooner. We didn’t, partly because subscribers had signed up for a specific portfolio and we were reluctant to change something they relied on. But maintaining two portfolios to say one thing is not a service to anyone. So we have now retired Dividend Growth as a standalone portfolio and rebuilt All-Weather with a proper construction framework.

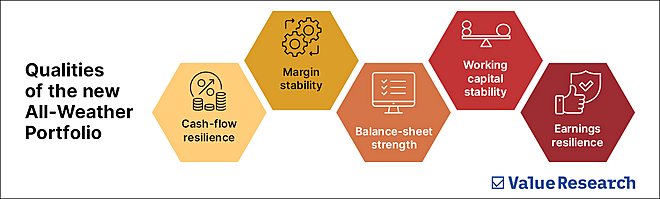

The new All-weather portfolio applies what we call a fundamental resilience score across five dimensions, as you can see in the graphic below.

A business that scores well on all five is the kind of business that absorbs a 30 per cent market fall without cutting its dividend, without scrambling for emergency capital and without posting a surprise loss that catches everyone off guard. Dividend growth remains a relevant signal within this framework. But the portfolio is no longer limited to dividend growers. A business can earn its place through durable margins or stable earnings, even if its dividend history is shorter.

Value Research Stock Advisor now has three portfolios, each doing one job. Three portfolios. No overlap. Each one is doing its job.

Long-term Growth: Selects reasonably valued growth companies for investors with over a seven-year horizon and the patience to let compounding play.

Aggressive Growth: Holds higher-potential companies where improving quality drives returns. For investors with a stomach to bear drawdowns.

All-Weather: For investors who need their portfolio to hold up when things go wrong. Which is to say, for exactly the kind of week we just had.

The monthly reviews our research team conducts are not just about finding new opportunities. They are equally about watching for early signs that a holding is drifting toward the second pile. When working capital starts deteriorating in ways that quarterly headlines do not capture, or when a management change raises questions about governance, we act. You hear from us before the market delivers its own, harsher verdict.

Here is what I keep coming back to. Crisis weeks remind you that the decisions that matter most in investing are seldom made during the crisis. They are made before it, in the patient, unglamorous work of understanding what you own and, just as importantly, what you have chosen not to own.

If you hold our portfolios and feel relatively settled this week, that is not luck. It is a process. If you are looking at your holdings right now with that familiar knot of anxiety and uncertainty, this may be a good time to consider doing it differently. Stock Advisor gives you three researched portfolios, monthly reviews, and clear exit calls. At Rs 9,990 a year, you are not paying for stock tips. You are paying to know which pile you are in. That is worth something. Especially on weeks like this one.

Subscribe to Stock Advisor today

Ask Value Research ![]()