On paper, it’s simple: income comes in, expenses go out, and whatever is left is “savings”. In real life, income comes in, rent, EMIs, school fees, petrol, Swiggy, Zomato, sale on Myntra, birthday gifts, one sudden expense… and at the end of the month, you look at your balance and say, “I’ll start investing from next month. Pakka.”

Next month looks surprisingly similar.

So let’s start with an honest admission: for most people, the problem is not which fund to choose. It’s how much they can realistically save when it feels like the money is just about enough.

At Value Research, whenever we look at this, we don’t begin with a number like “you must save 30 per cent”. We start with a different idea: savings are not what is left after spending. Savings are what you decide first; spending adjusts after that if you flip this order, the maths – and your behaviour – changes completely.

A good rule of thumb for many middle-class households is to aim for 20–30 per cent of their take-home income to go towards savings and investments. But I also know that for a lot of people today, 30 per cent sounds like a bad joke. So instead of fighting over the “ideal” number, let’s work with two simpler questions:

- What can you save today without breaking your life?

- How can you make that number grow every year?

To answer the first question, you need to know where your money is actually going, not where you think it is going. For one or two months, track your expenses honestly – not for Instagram, for yourself. You don’t need an app; even a simple notebook or spreadsheet works. Usually a salary of Rs 50,000 goes in four areas:

- Fixed essentials (Rent/EMI, school fees, utilities, groceries) - 40 per cent

- Discretionary (eating out, shopping, entertainment) - 30 per cent

- Random / One-offs - 20 per cent

- Transport - 10 per cent

Once you see your own pie chart, three things usually stand out:

- Some expenses are non-negotiable (rent, basic food, fees).

- Some are negotiable but important (a modest phone, occasional eating out).

- Some are pure leakage (unused subscriptions, impulsive orders, “I don’t even remember what this was”).

Your first “investment” might simply be plugging two or three leaks. Even if that frees up only Rs 2,000– Rs 3,000 a month, that is your starting SIP.

Now let’s look at how “small” that really is.

Suggested read: The great savings squeeze

From spare change to serious money

Even modest SIPs compound meaningfully over time

| Particulars | Scenario 1 | Scenario 2 | Scenario 3 |

|---|---|---|---|

| Monthly SIP (Rs) | 2,000 | 5,000 | 10,000 |

| Tenure | 20 years | 20 years | 20 years |

| Invested amount (Rs lakh) | 4.8 | 12 | 24 |

| Final value (Rs lakh) | 18.4 | 46 | 92 |

| Note: Assuming an annualised return of 12 per cent | |||

When we run these numbers at Value Research in our retirement and goal calculators, the results are always the same: the gap between zero and small is far bigger than the gap between small and perfect.

But what if your income truly is at the survival stage? There are people for whom even Rs 2,000 is a luxury some months. If that’s your reality, you have two parallel jobs. One is to create a tiny habit – even Rs 500 or Rs 1,000 a month into a recurring deposit or a conservative fund. The absolute amount is less important than the mental switch from “I’ll save if anything is left” to “I will save something, and then I will live on the rest.”

The second job is to make sure that as your income grows, your lifestyle doesn’t expand at the same speed. This is where a lot of middle-class Indians quietly sabotage themselves. Every salary increase automatically becomes a better phone, nicer meals out, upgraded gadgets, and bigger car loans. The percentage saved stays the same, or sometimes even falls.

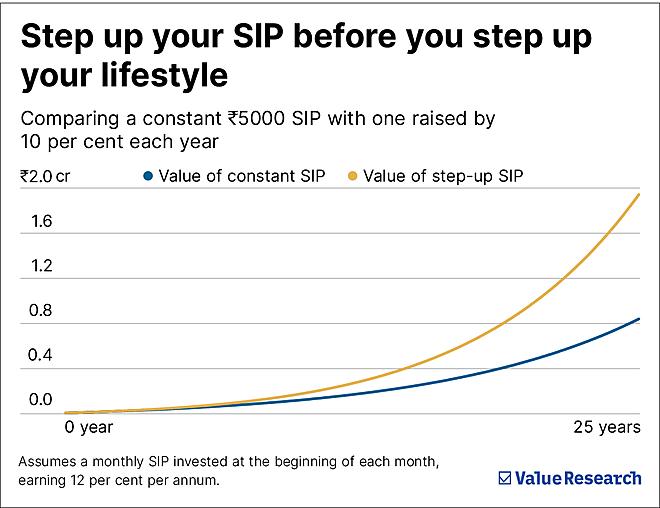

A very powerful habit – one we often build into plans at Value Research – is the “step-up”. Each year, when your salary goes up, you increase your SIPs and savings before you upgrade anything else.

Suggested read: Are we out of touch with reality to advise 10% step-up SIP?

In many examples we’ve run, the step-up strategy leads to a dramatically higher corpus at the end, without you ever feeling an acute “sacrifice” in any single year. You just avoid letting every pay hike leak out into lifestyle.

Now, how do you decide your own number?

Here’s a simple approach:

- First, add up your genuine essentials: rent/EMI, groceries, utilities, fees, basic transport.

- Next, be realistic and add a modest amount for discretionary spending that you know you’ll do anyway – because you are human, not a robot.

- See what is left. From that leftover, commit to a percentage – even 10 per cent of your take-home income – as a non-negotiable saving and investing amount. Set up automatic transfers and SIPs for that right after your salary date.

If that number feels tight, start a little lower and promise yourself one thing: every time your income goes up, your savings rate will go up faster than your spending.

At Value Research, when we build long-term plans, we don’t assume people will suddenly start saving 40% from next month. We assume they will start somewhere realistic, and then we design step-ups. The rigour is in the process, not in some magical starting number.

One last point. Many people postpone investing because they are embarrassed by how small their starting amount looks. Please don’t underestimate the psychological power of seeing a small, growing pile that you started and maintained. It changes how you think about yourself: from “I can’t save” to “I am someone who always saves something.” That identity is worth more than one extra dinner out.

So how much should you save and invest when your income feels just about enough? The honest answer is: start with whatever you can without lying to yourself, protect that amount like you protect your rent, and then make sure it rises every time your income increases. The “right” number is not what a formula says; it’s the number you will actually stick to for the next 20 years.

The perfect percentage can wait. The first rupee cannot.

Also read: The habit machine

Ask Value Research ![]()