Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

Summary: What can a humble Rs 2,000 SIP really achieve? In this story, a casual dinner sparks a powerful lesson in the magic of starting small. Backed by numbers, nudges, and real conversations, the article demystifies how consistency matters more than capital in building long-term wealth. For anyone wondering if their tiny SIP can make a difference, this is a must-read.

It started over dinner with an old college junior.

He had always been the risk-averse type, never one for stocks or mutual funds. But that evening, as we caught up on life and work, he surprised me.

“So, I started a SIP,” he said.

“Nice,” I nodded. “How much?”

“Rs 2,000 a month,” he replied, slightly hesitant to reveal the amount.

“But I keep wondering…will it even make a difference?”

There it was. The most common question I hear from people just starting out.

And it's a fair one.

It feels like a drop in the ocean.

Rs 2,000 is barely a fancy dinner or a few cab rides from my office to the New Delhi Railway Station. When everyone seems to be chasing multi-crore wealth, and that too as quickly as possible, this humble SIP naturally seems underwhelming.

But here’s the catch: wealth isn’t built through inconsistent and uneven leaps that happen in the form of large sums of money. In all honesty, you are more likely to build sizable wealth by taking baby steps.

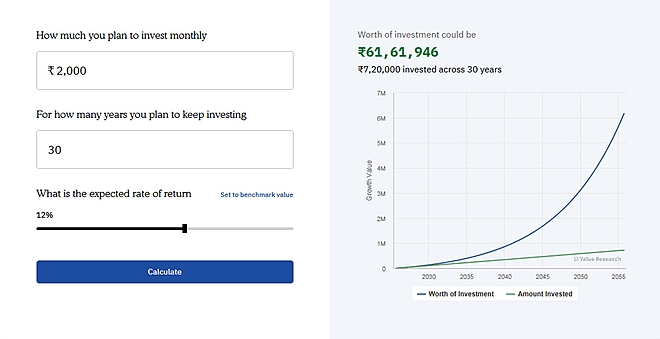

Using Value Research’s SIP calculator, I showed him how a Rs 2,000 monthly SIP in a good equity mutual fund delivering an average 12 per cent annual return could grow over time:

This is just from just Rs 2,000 a month.

“Over Rs 61 lakh?” he raised an eyebrow, slightly skeptical at first.

“Yes,” I smiled. “That's what time does. It's not about how much you start with, it’s about how long you stay with your habit.”

The habit matters more than the amount.

When you start small, you are building the habit of investing rather than trying to fast-track your way to a large corpus.

As you learn the basic tenet of investing – thinking long-term, you begin tracking your money. And if you treat this sum as a non-negotiable, your wealth grows over time.

And as your income grows, increasing your SIP then becomes second nature. And it becomes easier and more fun to invest.

My junior earns over Rs 75,000 a month. Even if he sticks to the same SIP amount, his portfolio will still be worth something. But if he steps it up by even 10 per cent a year, that Rs 2,000 SIP becomes around Rs 2,900 in five years and nearly Rs 4,700 in 10 years.

And his corpus after 30 years? It ends up growing to a significant Rs 1.5 crore. That’s right, Rs 1.5 crore!

And this doesn’t require big sacrifices. Just a small bump every year, ideally when you get your salary hike. You will need to manage expenses alongside to ensure the sum is present every month.

Now what about emergencies?

That night, my junior raised another concern. “What if I need the money? Won’t it get locked in?”

Another common worry.

The truth is, SIPs in most mutual funds aren’t locked in. The only exception is ELSS funds, which come with a three-year lock-in. So, if life throws a curveball, you can redeem your money at any time. Of course, we recommend not doing that unless absolutely necessary.

Which is why we always recommend building an emergency fund first. It should be at least six months of expenses kept in a liquid fund or a fixed deposit (FD). Only then should you start SIPs for long-term wealth.

This way, your long-term investments are not disturbed.

Even in a crisis, your emergency fund becomes your fallback.

The power of starting now

My junior is 29.

He has time on his side. Even if he doesn’t feel very wealthy today, he has something more powerful than wealth: he has many years on his side. And when it comes to compounding, time beats everything else. In fact, it doesn’t even matter if you invest a high sum if you have less time on your side.

Let’s say he delays his SIP by five years and starts at 34. Investing Rs 2,000 for 25 years instead of 30 would leave him with around Rs 34 lakh. That’s over Rs 27 lakh less than if he had started today.

This is why we always tell our readers: Don’t wait for the perfect time. Don’t wait for a big salary. Don’t wait till you know everything about mutual funds. And don’t wait until your finances are completely managed and you’re living on a surplus.

Start small. Start now. The rest will fall into place.

Some practical tips for new investors

Here’s what I told my friend that night and what I’d tell anyone starting a Rs 2,000 SIP:

Pick a simple, diversified equity fund. For instance, a flexi-cap fund can be a great starting point.

Automate your investments by setting your SIP date to the same time as when your salary reaches your bank account. To be on the safe side, you can keep it a couple of days from payday.

Don’t worry about the daily market noise, whether you’re buying a dip or you’re buying at a market high. Instead, just let the discipline of investing help you through.

For stepping up, there’s a simple rule. Keep the step-up amount proportionate to your income and do it every year.

Track your portfolio once a year. No need to tune into your investment app or news channels every day or week.

Now, will a Rs 2,000 SIP make you rich?

Maybe not by itself and not overnight.

But it’ll do something far more valuable: it’ll get you started on the investment route.

Along the way, you might see people sharing screenshots of massive portfolios or Rs 20,000 SIPs on social media. That’s okay. But don’t get caught up in comparisons. Your journey is your own. Starting with Rs 2,000 doesn’t make it any less valid; it makes it yours.

That night, as my college junior and I said our goodbyes, he looked a little more assured.

“I guess Rs 2,000 isn’t too bad then,” he said.

“It’s more than enough,” I replied. “As long as you stick with it.”

Want help picking the right fund for your Rs 2,000 SIP?

Getting started is the hardest part, but staying the course requires the right funds. At Value Research Fund Advisor, we guide you to mutual funds that match your goals, risk appetite, and investment horizon.

Start small, but start smart.

Also read: '25 funds in my portfolio. Where do I even begin?'

This article was originally published on September 16, 2025, and last updated on May 11, 2026.

Ask Value Research ![]()