AI-generated image

AI-generated image

Summary: One investor asked if a Rs 15,000 SIP could reach Rs 1 crore in 10 years. We ran the numbers, tested the returns and uncovered insights that might surprise even seasoned investors. So, before you plan your path to a crore, read this.

A curious investor recently asked: “Where and how much should I invest to target a corpus of Rs 1 crore in 10 years? I have started recently and invest Rs 15,000 every month in SIPs.”

This is the kind of question that pops up everywhere, from dinner tables to office chai breaks. Who does not dream of seeing seven zeroes in their portfolio in just a decade?

But whether this ambitious goal stands on firm ground depends on three critical levers: time, the amount invested and, of course, the returns earned. Let’s peel the layers to see if this dream is within striking distance.

The 10-year reality check

To keep things realistic—and steer clear of wishful thinking—the past decade was closely examined using 10-year rolling returns across various mutual fund categories.

For each, a straightforward approach was tested: a monthly SIP of Rs 15,000, once with no annual increase and once with a 10 per cent annual step-up. This helped estimate the corpus one might expect based on category average returns over the last 10 years. The outcomes are captured in the table below.

How far does Rs 15,000 SIP go in 10 years?

| Category | 10-year average return | Corpus after 10 years (no step-up) | Corpus after 10 years (10 % step-up) |

|---|---|---|---|

| Large Cap | 11.6% | ~32.9 lakh | ~48.1 lakh |

| Mid Cap | 15.1% | ~39.7 lakh | ~56.7 lakh |

| Small Cap | 16.1% | ~41.9 lakh | ~59.4 lakh |

| Flexi Cap | 12.6% | ~34.7 lakh | ~50.4 lakh |

| Large & MidCap | 13.3% | ~36 lakh | ~52.1 lakh |

| Value Oriented | 14.2% | ~37.8 lakh | ~54.3 lakh |

| 10-year category average rolling returns considered over the last 10-year period | |||

Turns out, even the top performers (small-cap funds) would have taken this investment to only around Rs 42 lakh without any step-ups. With a 10 per cent step-up, the most generous scenario nudges close to Rs 59 lakh.

So, how much longer to reach that crore?

Below is how long it would typically take (based on past average returns) to hit Rs 1 crore with a Rs 15,000 SIP, both without any step-up and with a 10 per cent annual step-up.

How many years to reach Rs 1 crore?

| Category | Time required (no-step-up) | Time required (10% step-up) |

|---|---|---|

| Large Cap | 18 years | 14 years |

| Mid Cap | 15.5 years | 13 years |

| Small Cap | 15 years | 12.6 years |

| Flexi Cap | 17.1 years | 13.9 years |

| Large & MidCap | 16.7 years | 13.5 years |

| Value Oriented | 16 years | 13.1 years |

| Calculations based on 10-year category average rolling returns from the past decade. Assumes a monthly SIP of Rs 15,000 in both cases. | ||

The time to reach Rs 1 crore stretches from about 15 to 18 years if the SIP stays flat. But add a 10 per cent annual step-up, and this range shortens meaningfully to roughly 12.6 to 14 years. Clearly, increasing the SIP each year speeds up the journey to the crore mark.

The key takeaway? Even if 10 years of disciplined investing doesn’t quite get you there, you’re not far off — just a few more years, and the target is well within reach.

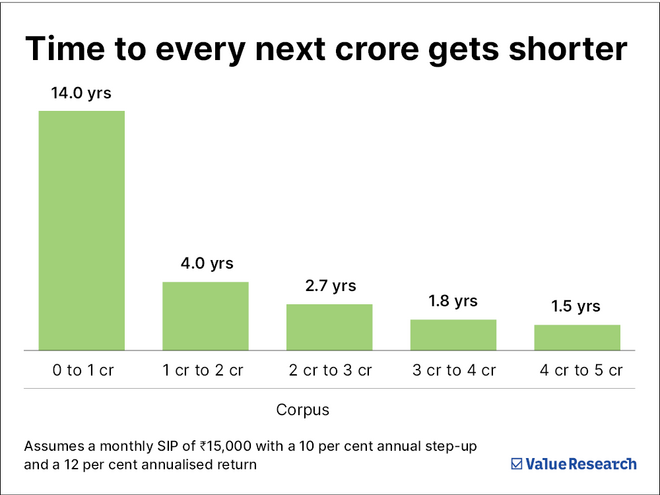

The next crore is a lot easier

Here’s where it really gets interesting. The first crore is always the hardest. It grinds along at a snail’s pace, taking more than 12 to 14 years to finally arrive. But after that, each new crore piles on much faster, all thanks to compounding quietly doing the heavy lifting behind the scenes.

So, while the first crore was a long, patient slog, taking 14 years, the leap from Rs 4 crore to Rs 5 crore comes in just about one and a half years.

Is Rs 1 crore in 10 years completely out of reach?

Not at all. It is very much possible, just not very common or easy for the average investor.

To see what kind of combination might do the trick, here is a matrix that shows the corpus amounts one can expect in 10 years based on a starting SIP (with 10 per cent step-up) and various annual returns.

SIP vs return matrix: What can you expect in 10 years?

| Starting SIP/Return % | Rs 5,000 | Rs 10,000 | Rs 15,000 | Rs 20,000 | Rs 25,000 | Rs 30,000 |

|---|---|---|---|---|---|---|

| 10 | 14.9 lakh | 29.8 lakh | 44.7 lakh | 59.6 lakh | 74.5 lakh | 89.4 lakh |

| 12 | 16.3 lakh | 32.7 lakh | 49 lakh | 65.4 lakh | 81.7 lakh | 98.1 lakh |

| 14 | 17.9 lakh | 35.9 lakh | 53.8 lakh | 71.8 lakh | 89.7 lakh | 1.1 crore |

| 16 | 19.7 lakh | 39.4 lakh | 59.1 lakh | 78.9 lakh | 98.6 lakh | 1.2 crore |

| 18 | 21.7 lakh | 43.4 lakh | 65 lakh | 86.7 lakh | 1.1 crore | 1.3 crore |

| 20 | 23.9 lakh | 47.7 lakh | 71.6 lakh | 95.4 lakh | 1.2 crore | 1.4 crore |

| 25 | 30.4 lakh | 60.8 lakh | 91.2 lakh | 1.2 crore | 1.5 crore | 1.8 crore |

The cells in bold reveal the magic combos of starting SIP and expected returns needed to hit that Rs 1 crore target in 10 years.

For instance, a monthly SIP of Rs 20,000 with a 10 per cent annual step-up could cross Rs 1 crore — if you also manage to snag a blistering 25 per cent annualised return. Now, putting in Rs 20,000 each month might still be within reach for some investors, but finding an investment category that reliably delivers 25 per cent year after year? That is about as likely as spotting a unicorn on a city street.

To put it in perspective, looking at category average 10-year rolling returns, no equity category has come close to sustaining 25 per cent over such a long period. Small caps are your best bet, but even they managed over 20 per cent only around 15 per cent of the time. The rest are nowhere near. Banking on such sky-high returns could set you up for a letdown.

But all is not lost. Even a more reasonable 14 per cent annualised return could get the job done, though it means starting with a heftier SIP of Rs 30,000 and stepping it up by 10 per cent each year.

The takeaway

The biggest lesson here? Be realistic. Future returns are not something anyone can command or predict with confidence. Everyone’s situation, goals and risk tolerance are different, so there is no one-size-fits-all plan. It is very important to invest as per your risk profile and time horizon.

Also, the first crore will likely take the longest. But once that snowball starts rolling, it picks up size and speed in a hurry. As seen above, getting from four crore to five crore can take a mere year and a half.

So, rather than chasing shortcuts, the focus should simply be on staying invested, upping SIPs over time and letting the twin forces of discipline and compounding do what they do best. In the end, the game rewards those who stay in it.

Also read: Rs 5 crore in 20 years: What should be the SIP amount?

This article was originally published on July 09, 2025.

Ask Value Research ![]()