Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

Summary: Most mutual fund investors assume the return figure on their fund factsheet is their personal return, but for SIP investors, that number tells only part of the story. This guide explains what XIRR actually measures, why it differs from the fund's reported CAGR, and when it can mislead you.

XIRR, or extended internal rate of return, is the method that calculates your actual annualised return when you have made multiple investments or withdrawals at different points in time.

For investors, this matters because most people invest in mutual funds through SIPs, a series of cash flows, not a single lumpsum, which means a simple annual return figure cannot capture the full picture of what your money actually earned.

Unlike CAGR (compound annual growth rate), which tells you how a fund performed from start to finish, XIRR adjusts for both the size and the timing of each individual cash flow. If you invested Rs 5,000 every month beginning January 2019, added Rs 50,000 as a lump sum in March 2020, and withdrew Rs 1 lakh in April 2024, XIRR calculates the single annualised rate that connects all those transactions and the current value of your holdings, as if it were one coherent investment.

How is XIRR calculated?

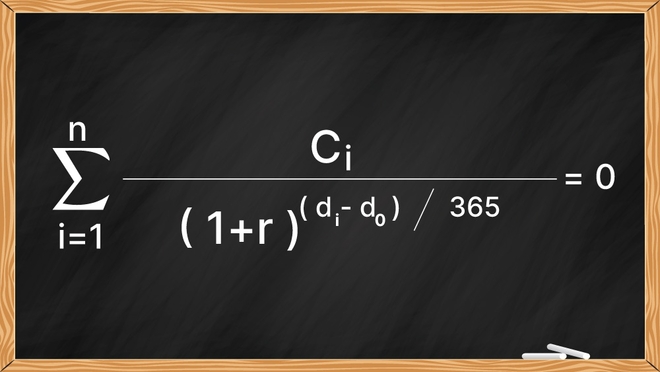

The technical definition: XIRR is the rate at which the present value of all cash flows (both investments and withdrawals) and the current value of your holdings equals zero.

XIRR is the rate ‘r’ that satisfies this equation:

Where:

C₁, C₂ … Cₙ = cash flows (negative for investments, positive for withdrawals or current value)

d₀ = date of first cash flow

dᵢ = date of each cash flow

r = XIRR (the annualised return rate that balances all cash flows to zero)

Alternatively, you can use this Excel formula to calculate your XIRR: =XIRR(values, dates).

To see how this works, consider a Rs 5,000 monthly SIP started in January 2019 and checked after five years. Your XIRR reflects not just the total return of the fund, but also how your money grew, given that your January 2019 instalment had 5 full years to compound, while your December 2023 instalment had only one month. This timing effect is exactly what XIRR captures and what CAGR ignores entirely.

XIRR vs CAGR: What's the difference?

XIRR and CAGR measure different things: CAGR tells you how the fund performed; XIRR tells you how your investment performed. The two figures will only match if you made a single lump-sum investment and exited all at once, a scenario that applies to very few SIP investors.

| Feature | CAGR | XIRR |

|---|---|---|

| What it measures | Fund's return, from one point to another | Your actual annualised return |

| Assumes cash flows | One-time investment, one-time exit | Multiple investments and/or withdrawals |

| Affected by when you invested | No | Yes |

| Useful for | Comparing fund performance | Tracking your personal return |

| Direct vs regular plan difference | Reflects scheme-level return | Reflects your actual plan's return |

Important: if you hold the same fund in a direct plan versus a regular plan, your XIRR figures will differ. The lower expense ratio in a direct plan means more of the fund's return reaches you. And over a long-horizon SIP, this gap can widen every year. CAGR, being a scheme-level figure, does not capture this difference.

Why is your XIRR different from your fund's reported return?

Most mutual fund investors assume that if a fund reports 12 per cent CAGR over five years, they personally earned 12 per cent. For SIP investors, this is rarely accurate, and understanding why the gap exists is one of the most practically useful things an investor can know.

In an SIP, your monthly instalments are invested at different NAVs. Instalments made when the market was lower bought more units, and those units had more time to grow. Instalments made when the market was higher bought fewer units at a higher price. XIRR weights each instalment by both size and timing. CAGR does not.

The direction of divergence depends on your entry point: if you began your SIP before a significant market rally, your early instalments compounded for longer at lower NAVs, meaning your XIRR may actually exceed the fund's reported CAGR. If you began near a market peak, your early instalments grew less than the fund's overall return suggests, making your XIRR lower than the fund's CAGR. Both figures are correct. They simply measure different things.

This is why checking only the fund factsheet can mislead you about your personal experience. Two investors who ran SIPs in the same fund at different times can have meaningfully different XIRRs.

Why does your XIRR look unusually high (or low) in the short term?

When you check XIRR within the first few months of starting a SIP, the figure can appear dramatically inflated, sometimes exceeding 40 per cent or 50 per cent, or deeply negative after a market dip. For investors, this is a mathematical artefact, not a signal of extraordinary performance or catastrophic loss.

Here is the mechanism: XIRR annualises returns. It scales any gain or loss up to a full year's equivalent. In the early months of a SIP, most of your invested capital is recent, so even a modest market gain translates into a very high annualised figure when projected over 12 months. A Rs 5,000 SIP that gains Rs 300 in two months would show an XIRR of roughly 36 per cent, because that gain on that capital over two months, annualised, implies a large rate.

But this says very little about what the fund will do over the years. Investors who check XIRR within three months of starting a SIP regularly see figures above 40 per cent. This is the annualisation effect, not a forecast.

The practical rule: XIRR becomes a meaningful guide only when your investment history spans at least two to three years. For shorter periods, the figure is mathematically valid but practically misleading.

Key takeaways

The number on your fund's factsheet is not your return. XIRR is

A fund can report 12 per cent CAGR and produce a meaningfully different XIRR for two investors running SIPs in the same fund, depending entirely on when each instalment was made. Checking only the fund's reported return gives you an incomplete picture of your personal wealth-building journey.

Short-term XIRR is a mathematical artefact, not a performance signal

Because XIRR annualises returns, a few months of SIP data can produce extreme-looking figures in either direction. Treat XIRR as a meaningful indicator only after at least two to three years of investment history.

Most mutual fund investors check the CAGR on their fund factsheet and assume that is their personal return.

For SIP investors, the two figures often diverge, and the direction of that divergence depends on when you started your SIP relative to market cycles. Understanding this gap is what separates investors who genuinely understand their portfolio from those who don't.

Frequently asked questions

Can XIRR be negative? What does that mean?

XIRR can be negative if your portfolio's current value is lower than the total amount you invested, accounting for the timing of each payment. A negative XIRR means your money has lost value in annualised terms. As with a high short-term XIRR, a negative figure in the early months of a SIP can reverse significantly as markets recover and the investment horizon lengthens.

Is XIRR the same for direct and regular plan investors in the same fund?

No. XIRR differs between direct and regular plan investors in the same fund because expense ratios differ. A direct plan carries a lower expense ratio, which means higher NAV growth and, over time, a measurably higher XIRR for the same SIP schedule. This gap compounds over the years.

Is there a ‘good’ XIRR target for a mutual fund SIP?

XIRR is a measure of what your investment has earned so far, not a target. Investors who want context for their XIRR can compare it against the fund's benchmark return (available on VRO fund pages) and against what a comparable fixed-income instrument, such as an FD or PPF, would have returned over the same period. Whether XIRR is meaningful depends on the category, the market period and the time horizon; there is no universal target.

What is the difference between XIRR and absolute return?

Absolute return is the total percentage gain or loss on your investment with no adjustment for time. XIRR annualises that return, accounting for timing. A 20 per cent absolute return over two years is approximately a 10 per cent XIRR; the same 20 per cent over four years is approximately a 4.7 per cent XIRR. For investments held longer than one year, XIRR gives a far more comparable picture than absolute return.

Also read:

This article was originally published on July 03, 2025, and last updated on April 02, 2026.

Ask Value Research ![]()