Adobe Stock

Adobe Stock

Does investing in stock markets feel unsettling, demotivating, full of anxiety or even depressing - especially when the market is tanking? Worry not, there's a smart way to handle this chaos.

Here's introducing asset allocation and rebalancing .

While these jargons may sound Greek to you and you may feel your morale sagging, let us assure you both 'asset allocation' and 'rebalancing' are easy nuts to crack.

So, let's decode them and understand when is the right time to put them into action.

Asset allocation

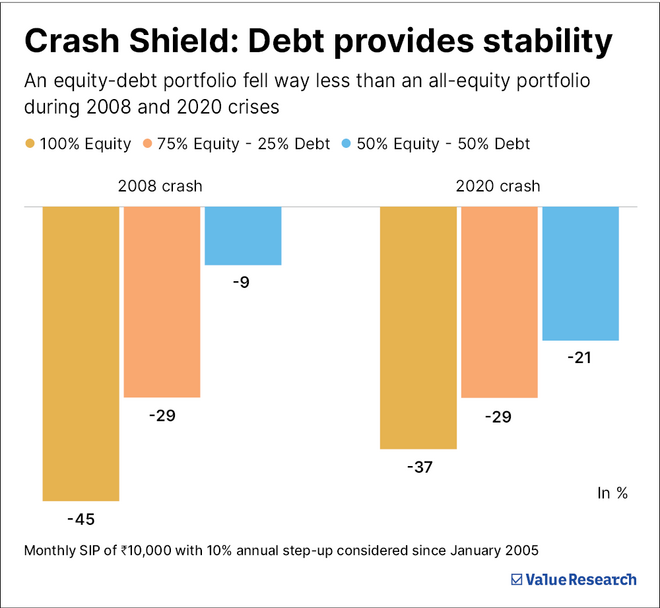

Asset allocation is simply deciding how much of your money should go into equity, debt or other assets (gold, real estate, etc.) based on your risk appetite, age and goals.

For new or cautious investors, this is especially important. Why? Because it gives you the best of both worlds: Equity brings growth. Debt brings stability.

So, when markets tumble, that boring old debt investment helps soften the blow. And when markets soar, equity ensures you don't miss the party.

The graph below clearly shows how adding debt to your portfolio can reduce the severity of losses compared to going 100 per cent into equity. This smaller dip can help investors - especially those new to the market - stay calmer during market crashes, making them less likely to pause SIPs or redeem in panic. In short, debt helps you keep your cool — and stay in the game when it matters most.

Rebalancing

Let's assume you've nailed your dream mix — say, 75 per cent equity and 25 per cent debt. You should remember that markets don't sit still. For example, after a market crash, your equity portion might drop to 65 per cent, while debt stays strong. In a bull market, your 75:25 mix might morph into 85:15.

That's where rebalancing comes in. It's like hitting the reset button — you realign your portfolio back to your ideal 75:25 mix.

How? If equity has grown too much, you sell a bit of it and buy some debt.

If equity has fallen too much, you buy more of it at a lower price.

In short, rebalancing helps you stay on track, book profits when high, and invest more when prices are low — all without emotional decisions. It's simple, powerful and a must-do for long-term success.

Which is the ideal way to rebalance?

There are different rebalancing strategies. Let's understand them and then look at their historical performances.

-

Calendar-based

: Once a year, every six months, or quarterly — like a dental cleaning for your investments.

-

Trigger-based

: Rebalance only when your allocation deviates by, say, 5 percentage points. We also explored a strategy combining annual rebalancing with trigger-based rebalancing. In this approach, you rebalance once a year on a fixed date, but also whenever your portfolio deviates by 5 per cent in between.

- Crash-triggered (being contrarian): Go all-in on equity during deep market falls by 20 per cent, then revert once markets recover.

To compare the performance of each rebalancing strategy, we assumed a monthly SIP of Rs 10,000 starting in January 2005, with a 10 per cent annual step-up. The portfolio began with a 75:25 mix — 75 per cent in equity (Sensex) and 25 per cent in debt (average short-duration fund ). Here's how each rebalancing strategy would have shaped your final corpus:

How different rebalancing tactics stack up

| Strategy | Corpus (in Rs) | Difference in corpus | Number of times rebalanced | XIRR (Performance) |

|---|---|---|---|---|

| Annual rebalancing (January each year) | 1.76 cr | - | 21 | 10.92% |

| Semi-annual rebalancing (January & July each year) | 1.76 cr | -0.44% | 41 | 10.87% |

| Quarterly rebalancing (January, April, July & October each year) | 1.76 cr | -0.16% | 81 | 10.90% |

| Crash-triggered rebalancing* (100% to equity when market fall 20%, back to 75-25% when it recovers) | 1.87 cr | 6.09% | 10 | 11.54% |

| Trigger based rebalancing (when allocation deviates +/- 5%) | 1.77 cr | 0.48% | 11 | 10.97% |

| Trigger based + Annual rebalancing | 1.74 cr | -1.52% | 30 | 10.76% |

| Note: Corpus value as of April 17, 2025. *In the crash-triggered strategy, annual rebalancing is followed except during crash periods, when the allocation shifts to 100 per cent equity. | ||||

As you can see, most strategies delivered a corpus nearly identical to simple annual rebalancing. The only outlier was the crash-triggered strategy, which came out on top, but only by a modest 6 per cent higher corpus. Modest because, in XIRR terms, that's just a 0.62 percentage point edge.

But that extra half a per cent comes at a higher risk. Let's assume that in a crash-triggered strategy, you go all-in on equity after a 20 per cent fall, but the risk doesn't pay off because the market keeps falling, like in 2008 (over 60 per cent) or 2020 (38 per cent). That means more pain before recovery begins.

Moreover, this approach demands constant market tracking. You'll need to know exactly when the fall hits 20 per cent and when the recovery happens to rebalance at the right time. All that effort is done for just 0.62 percentage points more. Probably not worth it.

Which is why annual rebalancing works best for most investors. This strategy delivers nearly the same outcome, with far less effort and stress. Just pick a date and rebalance once a year — that's it.

Now, some might wonder that if you're rebalancing annually, does the month you pick make a difference? To find out, we ran the numbers for each month. The result: rebalancing every April gave the best XIRR at 11 per cent, while August came in last at 10.73 per cent. That's a tiny gap of just 0.27 percentage points. In short, the month hardly matters. Just pick a date, stick to it and let your discipline do the heavy lifting.

The last word

At the end of the day, rebalancing is less about finding the "perfect" strategy and more about staying consistent. While crash-triggered or hyper-frequent methods may look fancy, they demand more effort and offer only marginal gains. Annual rebalancing strikes the sweet spot — simple, effective and stress-free.

Also read: The ultimate 'buy the dip' strategy for every investor

This article was originally published on May 06, 2025.

Ask Value Research ![]()