Open most investors' portfolios and you'll usually see a hotch-potch of schemes collected over the years rather than a carefully thought-out investment strategy: a flexi-cap from 2015, a tax-saver from 2017, two large caps bought after each bull-market TV debate, a mid cap discovered via a WhatsApp forward, a glossy NFO subscribed on the nudge of an advisor and so on.

That said, no one sets out to own a dozen funds; these funds just pile up. It doesn't take long before the number of funds outscore the episodes of a long-running web series.

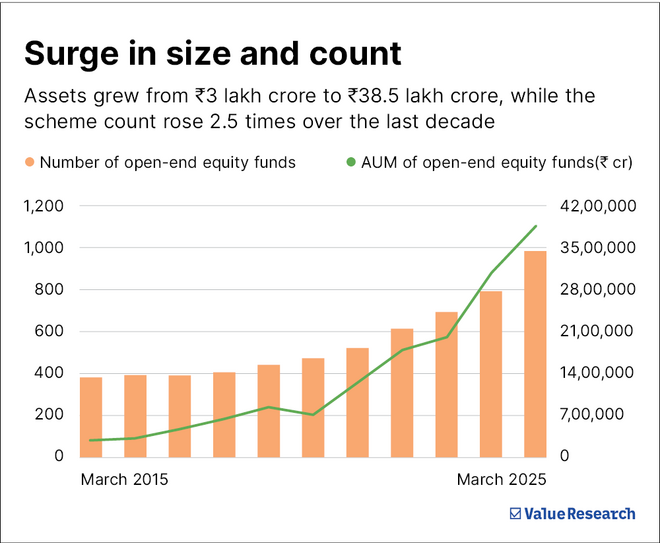

The numbers prove it as well. Assets in open-ended equity funds have shot up from Rs 3 lakh crore to Rs 38.5 lakh crore in a decade, while the count of live schemes has climbed from 382 to 986. The first graphic - Surge in size and count - shows both lines rising almost in lock-step.

Funds are getting launched at a furious rate, too. New-fund activity was before 2020. But after Covid, the watergates opened. From a modest 22 equity NFOs (new fund offerings) in 2015, 50 funds were rolled out in 2020, 87 in 2021, 111 in 2022 and a record 184 in 2024. The pace hasn't been let up this year either, with another 52 new funds hitting the market in just the first three months of 2025.

While the numbers clearly show our growing appetite for mutual funds , there's a worrying trend beneath the surface. The supply of fresh funds is outpacing the supply of fresh ideas - and that's bad news for investors. Why? Because launching new funds with similar mandates only adds to costs and paperwork, without offering anything meaningfully different in the underlying portfolios.

More ≠ better: The hidden overlap problem

Let's substantiate our previous statement as to why investing in more funds doesn't add much to our bottomline.

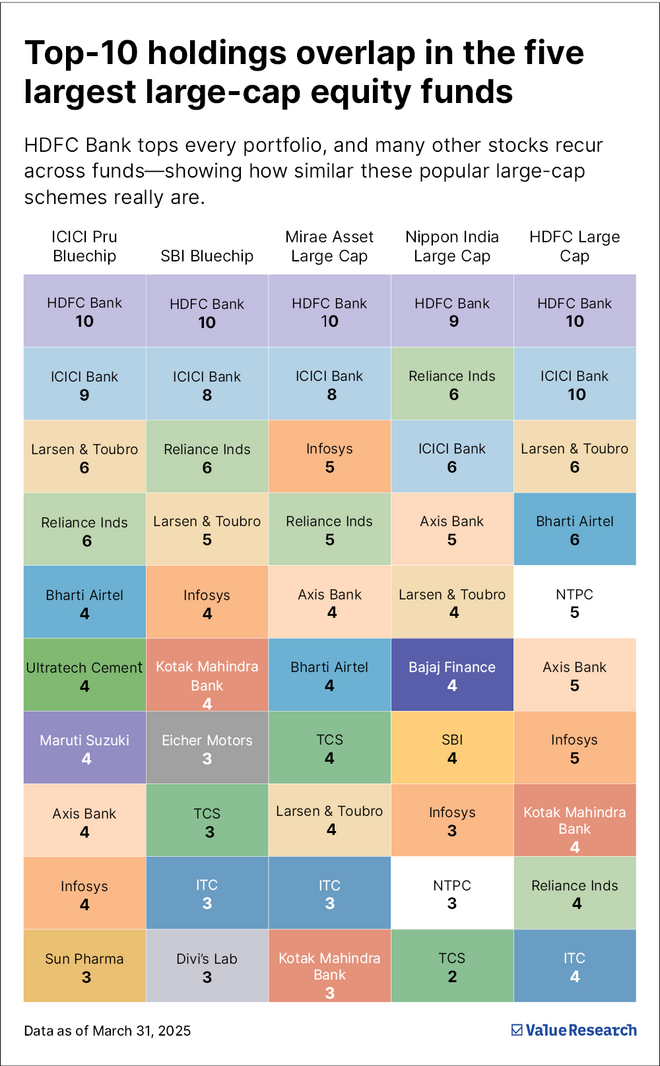

In order to this, our research team took the five largest active large-cap funds - HDFC Large Cap, ICICI Pru Bluechip, Mirae Asset Large Cap, Nippon India Large Cap and SBI Bluechip - to check how similar their portfolios are to each other with the help of Value Research Online's Fund Compare tool .

The heat-map graphic lights up like a summer afternoon. Portfolio overlap peaked at 59 per cent between HDFC Large Cap and Mirae Asset Large Cap. Even the least resembling large-cap funds, Nippon India Large Cap and SBI Bluechip, had 46 per cent stocks in common.

Stocks of HDFC Bank, ICICI Bank, Larsen & Toubro, Reliance Industries and Infosys are part of all the five funds, while Axis Bank appears in four. That is six stocks accounting for a chunky slice of each fund. Add two or three more usual suspects and you have the bulk of the "diversification" done.

Suggested read: Diversification can be a dummy exercise. So, check this for best result.

Which means that if you own two or three of these funds, you have paid multiple expense ratios to own the same companies several times over.

The expense ratio pinch

Let's now look at the expense ratio , which is an annual maintenance fee charged by fund houses.

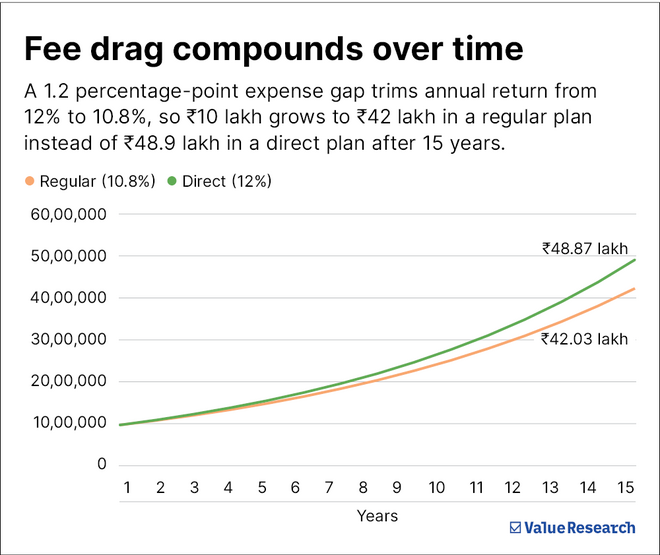

Expense ratio feels harmless when you look at them in a single‐year snapshot. It never exceeds 2.5 per cent, which is a small percentage from a one-year perspective. This is the reason why most investors still hold the regular plan that their adviser first sold them, even though the direct version of the very same fund is cheaper. As of March 2025, the median gap in expense ratio between a regular and a direct actively managed flexi-cap plan is 1.2 per cent a year.

In other words, let's assume you put Rs 10 lakh away for 15 years and assume the underlying portfolio earns 12 per cent before costs. In the direct plan (paying lower fees), your money would grow to Rs 48.9 lakh. Meanwhile, the regular plan grows to a tickle over Rs 42 lakh. Result? You make almost Rs 7 lakh more by investing in a direct plan because it charges a lower expense ratio.

And remember, that figure is for one scheme. Hold two or three funds - in regular plans - and the fee drag multiplies faster than your returns do.

The behavioural problem

While fees are visible on paper, behavioural mistakes creep in unseen. Industry flow data across equity and hybrid schemes reveal a familiar beat: money floods into any fund after a standout year and trickles out after the first wobble. That hot-hand chase leaves investors earning significantly less than the very funds they own. Recency bias, fear of missing out and headline envy all play their part.

That said, before you make the switch to a direct plan or plan to trim your fund count, there are two things you need to consider:

- Exit-load clocks: Many equity schemes claw back 1 per cent if you take your money out from a mutual fund within 365 days. So, check what the exit load of the fund is.

- Capital gains: Equity gains under a year are taxed at 20 per cent; beyond a year, they attract 12.5 per cent but only after the first Rs 1.25 lakh per financial year. Spread the exits over two years and you double the exemption.

How many funds do you really need?

There's no statutory number, but experience suggests most investors can cover all asset classes with just three to five funds: one broad-market equity core (index or seasoned flexi-cap), one mid- / small-cap satellite, one short-duration debt anchor, a global equity feeder and an optional liquid fund for emergencies.

Everything else must justify its seat at the table by adding a genuinely new return driver at a reasonable cost.

A four-phase clean-up plan

| Phase | Action | Pay-off |

|---|---|---|

| 1 Inventory | Upload portfolio on Value Research's My Investments tracker | Provides a consolidated view of exit load and tax outgo. |

| 2 Portfolio check | Use the VR Fund Compare tool to look at the portfolio of two funds. | Spot funds with high portfolio overlaps. |

| 3 Rank & decide | If there are two funds with significant overlaps, keep the cheaper, steadier option; schedule the exit of the other fund once its exit-load window has passed. | Cuts fee drag without incurring avoidable penalties. |

| 4 Tax-smart switch | Split large redemptions across two financial years to use the Rs 1.25 lakh LTCG allowance twice, and reinvest the proceeds the same day in the survivor funds. | Minimises the tax bite and removes market-timing risk while you streamline. |

Follow these four passes and you'll turn a tangle of look-alike schemes into a tight, low-cost line-up that's easier to monitor - and cheaper to own.

The bigger picture

The clean-up is not about picking the "best" funds. That list changes every cycle. It is about owning a line-up you can monitor easily. Doing so will help you:

- Rebalance with a single spreadsheet column

- Spot style drift before it hurts

- Update nominees without a paper chase

- Leave behind an estate that your family can settle over a weekend, not a season.

Simplicity compounds

Collecting funds is effortless; curating them is work. Yet the difference between a tidy portfolio and a cluttered one is not just administrative - it is measured in percentage points of return and lakhs of rupees left on the table.

So pour yourself a cup of tea or coffee, open your fund portfolio and start scratching out duplicates. Let the graphs in this story serve as both warning and motivation: fee drag is relentless, overlap is rampant and the industry will not stop offering you more options. Your job is to say "no, thanks" often enough to keep your money - and your mind - free to grow. In investing, as in life, less clutter usually leaves more room for growth.

Wondering which of your schemes are keepers and which are clutter? Let Value Research Fund Advisor analyse and tell you.

Also read: Is your mutual fund portfolio a mess?

This article was originally published on April 28, 2025.

Ask Value Research ![]()