AI-generated image

AI-generated image

The rate-cut cycle has already started, with the Reserve Bank of India (RBI) cutting the repo rate from 6.5 to 6.25 per cent in its last policy meeting—its first rate cut in around five years. And with the next monetary policy scheduled for April 7 to 9, there are chances the repo rates are slashed further.

Whether we'll see another cut during this meeting is uncertain, but the direction is clear: we are now in the early stages of a falling interest rate cycle. In such a time, a key question arises for investors: which type of debt (fixed-income) mutual fund is best suited to this environment?

Why interest rates matter to debt funds

To understand which fixed-income category works best, it's important to first grasp how interest rates impact the returns of debt funds.

Debt mutual funds invest in bonds that pay a fixed interest (called a coupon) for a certain period. When interest rates fall, newly issued bonds start offering lower interest. This makes existing bonds—paying higher rates—more valuable. As a result, their prices rise.

Since mutual funds hold these bonds, a price rise increases the fund's net asset value (NAV), leading to capital gains for investors.

However, not all bonds behave the same way. Bonds with longer maturity periods (or higher duration) react more sharply to changes in interest rates than short-term bonds. This means:

-

When rates fall → long-duration bond prices rise more → long-duration funds deliver higher returns

- When rates rise → long-duration bond prices fall more → long-duration funds suffer steeper losses

In contrast, short-duration funds are relatively immune to these swings. They offer lower upside when rates fall but also cushion investors during rising rate scenarios.

What history tells us

To see how this plays out in reality, let's look at how long- and short-duration funds have performed during major rate-cut cycles.

Long-duration funds generally fare better in falling rate cycles

| Date of rate cut | Repo rate cut by | Fund type | Following 6-month return | Following 1-year return | |

|---|---|---|---|---|---|

| 07-Feb-19 | 0.25% | Long duration | 12.3% | 15.3% | |

| Short duration | 2.2% | 6.1% | |||

| 04-Mar-15 | 0.25% | Long duration | 1.0% | 13.5% | |

| Short-duration | 3.7% | 12.6% | |||

| 30-Jul-08 | 0.50% | Long duration | 18.9% | 19.6% | |

| Short duration | 6.7% | 9.5% | |||

| Note: For a long time, only one long-duration fund existed, and its data has been used as a proxy for historical performance. | |||||

Clearly, long-duration funds generally shine when interest rates start falling. The gains can be substantial over a relatively short span, especially when the market is caught off guard by a rate cut.

Why you should not chase returns blindly

While the past returns look attractive, they come with a caveat: volatility.

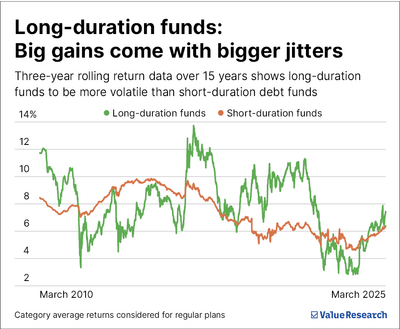

Over the past 15 years, based on one-year rolling returns, long-duration funds have swung between -3.3 per cent and 21.5 per cent. Short-duration funds, on the other hand, have ranged between 2.6 per cent and 11.3 per cent. When you look at the average returns over the same period, the gap narrows significantly.

Even over holding periods like three years, long-duration funds have delivered an average of 8 per cent, while short-duration funds have provided 7.4 per cent. So while long-duration funds may outperform briefly during rate cuts, their long-term edge isn't dramatic. Worse, they expose you to much higher volatility in the process. That said, it's worth mentioning that for a long time, only one long-duration fund existed, and its performance has been used as a proxy to illustrate the category's historical behaviour.

Which type of fixed-income fund to choose?

Falling interest rates generally benefit long-duration fixed-income mutual funds the most. But that doesn't make them the right choice for everyone.

The primary role of fixed income is to provide stability, not to chase returns. That job is better left to equities. Given this, your core fixed income portfolio should be built around short-duration or other lower-duration categories, which offer more predictable returns and lower volatility.

However, if you're keen to take advantage of the current rate-cutting cycle, you can consider a tactical allocation of 5 to 10 per cent to long-duration or dynamic bond funds. This allows you to capture potential upside without compromising the overall safety of your debt portfolio.

Stick to short-duration for your core, and treat long-duration as an optional overlay—not the foundation.

Also read: Index vs Flexi-cap vs Multi-cap funds: Where to invest today

Ask Value Research ![]()