AI-generated image

AI-generated image

Inheriting money from your parents isn't just about numbers—it's a deeply emotional experience. It's their hard work, their sacrifices and their love for you, bundled into a sum that can shape your future. The responsibility? To honour their legacy while securing your own.

So, when a reader recently asked - "I inherited some money from my parents. How can I grow this amount while keeping it safe, as it's all I have? I was thinking of putting it in a post office monthly income scheme and investing the monthly interest in mutual funds. Is it a good plan?" - we thought of offering even better options that can make your money work hard for you.

Option 1: The 'safe but slow' approach

Parking your inheritance in the Post Office Monthly Income Scheme (POMIS) would provide fixed monthly interest, which you could then channel into equity mutual funds for potential corpus growth.

What's good

-

Your principal remains safe.

- You have a consistent income stream.

What's not-so-good

-

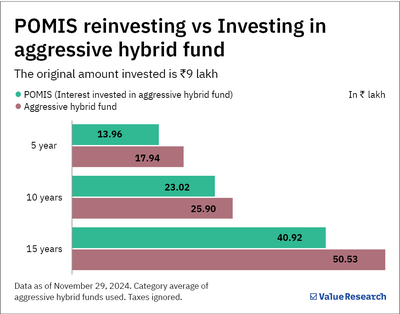

Growth is limited because you only invest the interest amount, not the principal. Let's say you invested the maximum investable amount of Rs 9 lakh in POMIS and invest only the interest amount in

aggressive hybrid funds

, your corpus would have grown to Rs 14 lakh in five years, around Rs 23 lakh in 10 and nearly Rs 41 lakh in 15. If you instead invest the interest into a pure equity fund, like a flexi-cap fund, you could accumulate over Rs 14 lakh in five years, nearly Rs 25 lakh in 10 years and over Rs 47 lakh in 15 years. These calculations ignore taxation. Do note that interest earned from POMIS is taxable at your slab rate.

-

Secondly, inflation can silently erode your purchasing power over time.

So, the Rs 14 lakh accumulated in five years would have a reduced purchasing power of just Rs 10.46 lakh, assuming inflation at 6 per cent p.a. Similarly, Rs 23 lakh accumulated in 10 years and Rs 41 lakh in 15 years would be worth only Rs 12.84 lakh and Rs 17.10 lakh, respectively, in today's terms.

Option 2: The 'let it soar' approach

The other option is to shift the inheritance money to an equity-focused mutual fund.

However, since many people are hesitant to have 100 per cent of their inheritance in equities, you can invest the amount in aggressive hybrid funds. Why? Because these funds typically allocate 65 to 80 per cent in equities, with the remainder in debt instruments, offering a balanced approach. While equity investments do carry some risk, the long-term potential for substantial rewards makes them an attractive option.

If you can recall, in the previous section, the Rs 9 lakh investment in POMIS would have grown to Rs 14 lakh, Rs 23 lakh and nearly Rs 41 lakh over five, 10 and 15 years, respectively.

In comparison, the same Rs 9 lakh amount invested in an aggressive hybrid fund would have grown to Rs 18 lakh in five years, Rs 26 lakh over 10 years and over Rs 50 lakh in 15 years.

At this point, you might think, "Wait, isn't the stock market risky?"

Yes, it is. But here's the kicker: time is the ultimate risk mitigator. Over 10, 15 or 20 years, the ups and downs of the market tend to smooth out. The longer you stay invested, the lesser the chances of losing money in equities.

History has shown that, with time, the likelihood of negative returns diminishes significantly. The table below shows how, with an increase in time, the chances of negative returns go down.

Longer timeframes flatten risk element from equity investment

The longer you stay invested, the higher the chances of earning double-digit returns

| Return range | 3 years | 5 years | 7 years | 10 years |

|---|---|---|---|---|

| Negative returns | 7% | 1% | 0% | 0% |

| 0% to 5% | 14% | 4% | 2% | 0% |

| 5% to 10% | 18% | 22% | 24% | 10% |

| 10% and above | 62% | 72% | 74% | 90% |

| Data based on rolling SIP returns for category average of aggressive hybrid funds | ||||

What you should do

-

If you are emotionally attached to the inherited money, keep part of it in safe options like POMIS or fixed deposits for peace of mind.

-

Invest the rest in diversified mutual funds. Consider aggressive hybrid funds for a mix of equity and debt. For a more risk-on investor,

flexi-cap funds

can offer higher growth potential.

-

Don't invest all your money in one go. Start a

systematic investment plan (SIP) or a systematic transfer plan (STP)

to spread your investments and reduce the impact of market volatility.

- Review your portfolio every year to ensure it aligns with your plans.

Also read: How can a three-layered emergency corpus help you ride out emergencies?

This article was originally published on December 05, 2024.

Ask Value Research ![]()