AI-generated image

AI-generated image

Many people get caught in the spiral of spending and earning. So, keeping aside enough money for investing becomes a challenge. But the mutual fund industry has evolved quite a bit such that you can start small with even an SIP of Rs 250.

If you are curious about mutual funds and want to give a push to your investment journey, then this article is for you. First, we'll walk you through the reasons that make mutual funds the best place to start investing.

Build a diverse portfolio for a small sum

If you plan to invest in equity, then you can diversify your investments at a low cost by investing in equity funds. For example, even if you invest Rs 500 in one equity fund, you will still get exposure to a large number of stocks.

A professional manages your money

It can be challenging for some investors to navigate the capital markets as they do not have enough knowledge and experience. For such individuals, having a fund manager to oversee their investments can be a great boon.

Complete transparency about investment decisions

Usually, all asset management companies provide scheme-related details like past performance, expense ratio, the performance of the scheme as against the benchmark and category average, changes in NAV and so on. Also, there are several regulations enforced by SEBI (Securities and Exchange Board of India) on fund houses. These regulatory measures are meant to keep your money safe and secure.

Buying and selling your investments becomes simple

By investing in mutual funds, you get the benefit of being able to sell your investments without restrictions. Although fund categories like equity-linked savings scheme (ELSS) and fixed maturity plans come with a lock-in period, other funds have complete liquidity. Simply keep in mind that there might be an exit load when you sell your investments.

The power of compounding

"Money makes money. And the money that money makes, makes money."- Benjamin Franklin

This quote expresses the phenomenon best. Here's a small example:

Suppose you have invested Rs 10 lakh in a mutual fund, which gives you a return of 10 per cent every year. Your money would become Rs 11 lakh in the first year. In the second year, you will get returns on not just Rs 10 lakh but Rs 11 lakh - the sum your invested amount grew to in a year.

Easy to get started with

Mutual funds are an investment vehicle appropriate for small investors with limited funds to invest.

In fact, it is worth noting that among different kinds of investment instruments, the two types of mutual funds, outperform all other instruments, including but not limited to fixed deposits, PPF, and National Savings Certificates (NSCs). For instance, the below graph shows how your money would grow if you had invested Rs 1 lakh 10 years ago.

Now that we have run you through the many benefits of mutual funds, what are its drawbacks?

Tax on capital gains

One of the biggest concerns is the rising capital gains tax on equity-oriented funds. Also, a major upset is the loss of the indexation benefit on debt funds (and a number of other categories). While these may discourage you, we have some advice. Do not invest with the goal of simply tax efficiency; take other factors into consideration.

Suggested read: Beyond taxation

Lock-in period

As discussed earlier, certain fund categories come with a lock-in period. While a lock-in period can seem like a drawback, it helps build discipline on your investment journey.

Varying returns

If you invest in mutual funds, you will not get any fixed returns. Given the market volatility, your investments will be subject to a vast range of price fluctuations, including the depreciation of the value of your investments.

What is the KYC process for mutual funds?

KYC stands for 'Know Your Customer'. It is mainly a customer identification process that is conducted when opening an account with a financial entity.

Now you have the Central Know Your Customer (CKYC) facility, which was initiated by the government of India. This initiative allows you to do the KYC process just once. So, you do not need to complete the documentation process each time you invest in a new fund.

Also, you can do your KYC through the distributor, which would also lead to documentation in CKYC.

Documents required to invest in mutual funds

If you want to invest in mutual funds online, you need to submit the following documents.

1. Identity proof: To verify your identity, you can submit your passport, PAN card and Aadhar card to the fund house.

2. Address proof: To verify your address, you can submit your driver's licence, Aadhar card, and voter's ID card to the fund house.

How to transact in mutual funds

There are different ways through which you can transact in mutual funds.

- SIP: An SIP or Systematic Investment Plan is an investment mode that allows you to invest a fixed amount periodically.

You can start the SIP with a very small amount. The auto-debit service option of your bank will enable you to make your investments automatically. Now, you can even invest on specific dates of the month.

The key is to recognise that there is no best date for SIP. Instead, you should align it with your salary or earning cycle and start. You can always streamline it later.

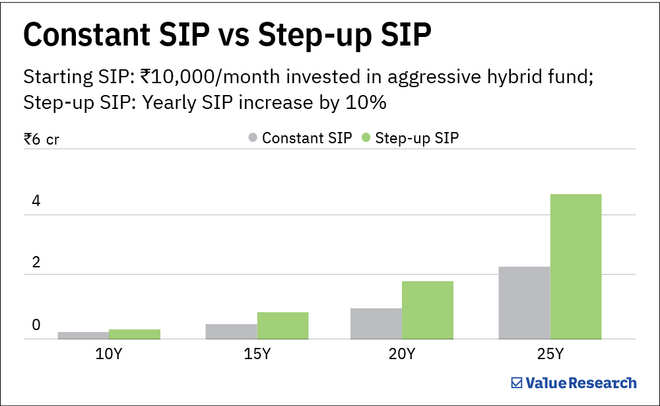

Also, you should increase your SIP as your income grows. Let's show you what happens if you invest in an average aggressive-hybrid fund and start an SIP of Rs 10,000, stepping it up by 10 per cent every year. - Lumpsum: It is a one-time investment where you make the entire investment in one go. This is usually not recommended for equity fund investments. However, if you're looking at investing in debt funds for a short duration, this is not a bad option.

- STP: You can opt for a systematic transfer plan (STP) when you have a lump sum to invest and want to invest the money across a longer time horizon. Under an STP, you can make a lump sum investment in one scheme (a debt scheme mainly) and transfer a specific amount regularly from this scheme to another scheme (mostly equity).

- SWP: An SWP or systematic withdrawal plan enables you to withdraw a fixed amount of money from your mutual funds at regular intervals. This mode is especially appropriate for retirees looking for a fixed income flow.

From where to invest in mutual funds

There are various ways through which you can invest in mutual funds. These include:

- You can invest through the website or apps of an AMC.

- Another option to invest in a mutual fund is through a distributor. However, if you follow this route, your expense ratio will be higher, which will eat into your returns.

- You can also invest in mutual funds through Registered Investment Advisors (RIA) and Registrars and Transfer Agents (RTAs).

- You can even try out some broking platforms as they allow you to invest in the direct plans of mutual funds. If you invest in a direct plan, you can avoid paying commissions and your net returns are higher.

- There's the option of using MFCentral, which makes mutual fund investing much easier. We've provided a complete guide for utilising this platform for investment needs.

What are the various mutual fund fees and charges?

- Expense ratio: To manage a fund, the fund house charges an annual maintenance fee called the expense ratio. This ratio varies from one fund to another. However, the market regulator has set a maximum limit to this fee.

- Transaction charge: It is a token amount levied on you only once during your entire investment period. Fund houses can charge a transaction fee of Rs 100 for their existing investors and a transaction fee of Rs 150 for new investors if the worth of the investment is Rs 10,000 and above. Nevertheless, you will not be charged any transaction fee if the value of your investment is less than Rs 10,000.

- Exit load: If you exit a mutual fund scheme within a short time, then you will be charged an exit load. Exit loads are also called redemption fees. It is charged to discourage you from withdrawing your funds prematurely. This fee enables fund houses to minimise the volume of withdrawals.

Also read: A beginner's guide to mutual funds

This article was originally published on September 26, 2024.

Ask Value Research ![]()