AI-generated image

AI-generated image

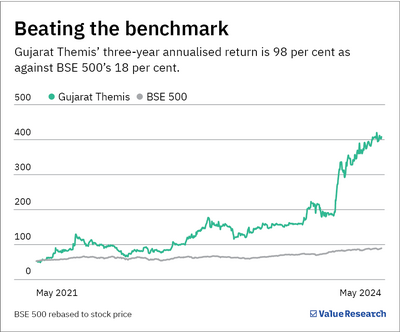

The Indian pharmaceutical industry has given the market several prominent wealth creators over the years. Gujarat Themis Biosyn, a small-cap pharma player, might be on its way to becoming a new addition to this illustrious list.

In the last five years, the stock witnessed remarkable financial growth, with its revenue and profit after tax growing at an annual rate of 31 and 62 per cent, respectively. Further, its operating profit margin zoomed by over 21 percentage points in FY20 and has remained steady.

This impressive performance did not go unnoticed. Its share price grew by 159 per cent in the last 12 months (as of May 18, 2024).

An impressive journey

The company's revenue has jumped by almost four times since FY19

| TTM | FY23 | FY22 | FY21 | FY20 | FY19 | |

|---|---|---|---|---|---|---|

| Revenue (Rs cr) | 156 | 149 | 115 | 91 | 85 | 41 |

| Operating profit (Rs cr) | 70 | 72 | 56 | 39 | 30 | 6 |

| CFO (Rs cr) | 57 | 40 | 40 | 11 | 1 | 1 |

| Profit after tax (Rs cr) | 55 | 58 | 44 | 30 | 24 | 6 |

| EBIT margin (%) | 44.6 | 48.1 | 48.6 | 42.6 | 35.8 | 15 |

| ROE (%) | 33.6 | 45.9 | 50.4 | 53.8 | 78 | 41.8 |

| D/E | 0 | 0 | 0 | 0 | 0.2 | 0.3 |

| Note: TTM as of December 2023 | ||||||

An unprecedented rally such as this demands further inquiry. So, let's delve into the factors driving Gujarat Themis' growth machine.

The story behind its success

Gujarat Themis Biosyn specialises in fermentation technology. Its key products include Rifamycin S and Rifamycin O, which are used to treat tuberculosis and diarrhoea.

Initially, it operated as a contract manufacturer with fixed profit margins. However, its financials took a turn for the better when the company's management saw an opportunity to fill the gap in the domestic market and started selling directly to large pharma clients. This strategy paid off, leading to significant increases in revenue and profit margins, which have been consistently high since FY20.

This increase in profitability surely wooed the market. But, D-street is betting on more than just its past performance.

The plan forward

To sustain its strong financials, Gujarat Themis has planned a capital expenditure of Rs 200 crore to boost the production of its existing products and APIs. It aims to double its production capacity by the end of FY25, with the new API facility expecting to generate around Rs 160 crore in revenue, slightly higher than its TTM (trailing twelve months) revenue as of December 2023.

But before you rush to invest, know that there are lurking concerns that cannot be ignored.

The challenges ahead

Currently, Gujarat Themis is operating at full capacity, and expansion will take time. For instance, its new API unit, launched in December 2023, will only start commercial operations in the second half of FY25 after multiple audits and approvals. Additionally, setting up R&D labs and launching new products is a lengthy process that can take up to two to three years.

Another challenge is the company's dependence on just two products and two key clients, which accounted for 56 per cent of its revenue in FY23. If these customers face any issues or change their contracts, it could significantly impact Gujarat Themis's books.

Further, entering the API manufacturing market might create conflicts of interest for the company with its clients, who are also in the API business.

Investor's corner

Gujarat Themis' remarkable growth presents a strong investment case. Its capacity expansion initiatives also add to it. However, the above risks should not be ignored.

Besides, the stock's valuations are also concerning. It trades at a P/E (price-to-earnings) ratio of around 54 times. If the P/E contracts to 33 times (the median P/E for pharma companies in the BSE Healthcare index) and its EPS (earnings per share) grows 20 per cent annually, its share price will compound a mere 8.9 per cent annually over the next five years. This is just slightly above the government bond yield rate of 7 per cent (risk-free rate).

Also, note that this is not a stock recommendation. We have only explored the factors that led to the recent surge. You must explore a business and its industry thoroughly before making any investment decision.

Also read: You may gain from this chemical manufacturer despite expensive valuations

Ask Value Research ![]()