India's growing aspiration for fit and healthier lifestyles is strengthening its fitness industry and driving demand for sports and athleisure products, including footwear, apparel, and accessories. Notably, this segment grew the fastest (in terms of usage) against casual and formal segments between FY15 and FY20, according to a report by consulting firm Technopak. The sports footwear category has been the prime beneficiary of this trend, witnessing intense competition with the presence of many global and local players.

Comparison with peers

Metro beats its peers comfortably on every factor

| Company name | Revenue (5Y per annum growth) | Operating profits (5Y per annum growth) | Profit after tax (5Y per annum growth) | 5Y median operating profits margins (%) | 5Y median ROCE |

|---|---|---|---|---|---|

| Metro Brands | 15 | 19 | 21 | 19 | 34 |

| Bata India | 6 | 11 | 8 | 13 | 31 |

| Relaxo Footwears | 7 | -3 | -1 | 12 | 25 |

| Khadim India | -2 | -10 | -14 | 4 | 10 |

| Liberty Shoes | 4 | 1 | 14 | 4 | 10 |

| Mirza International | -8 | -24 | -20 | 9 | 12 |

|

We haven't taken Campus Activewear because its five years number were not available. These have been computed from FY18-FY23 and not on TTM basis because Metro got listed in December 2021 and its quarterly TTM data isn't available for five years. |

|||||

The largest footwear company by market capitalisation, Metro Brands , is the latest to foray into the rapidly growing sports footwear category. In 2022, it acquired Cravatex Brands, a retailer and distributor of global giant Fila and homegrown Proline, and rebranded it as Metro Athleisure. It also recently entered into a strategic partnership with American premium athletic footwear retailer Foot Locker to own and operate its stores.

Metro plans to grow the Foot Locker brand only in metro and tier-one cities to capitalise on the rising premiumisation trend in the country. It planned to initially open 4-6 Foot locker stores as of March this year and ramp up by FY25. For Fila, it plans to close its existing 14 stores by June and re-launch the brand by leveraging the vast distribution network of its multi-brand outlets (MBOs).

But what gives it the edge? Is the company capable of succeeding in such a heated-up segment? Take a look at factors in its favour.

1) Riding on premiumisation

Metro Brands offers footwear in the economy (Rs 501-1,000), mid (Rs 1,000-3,000), and premium (more than Rs 3,000) segments. However, it has been sharpening its focus on product premiumisation, leading to a consistent increase in its average selling price over the years.

It has the highest average selling price among its peers and has been the fastest-growing player in the industry in the past five years. Despite not having its own manufacturing units, the company has the highest margins and return on capital employed (ROCE). The addition of Fila with a higher average selling price is also in line with its premiumisation strategy.

2) Most liked by global brands

The company is the most preferred for global tie-ups and has the largest third-party portfolio, including prominent names like Crocs , Skechers , Fitflop, etc. This is due to its massive distribution network and years of experience, which allow its international partners to reduce their gestation period and increase the probability of success.

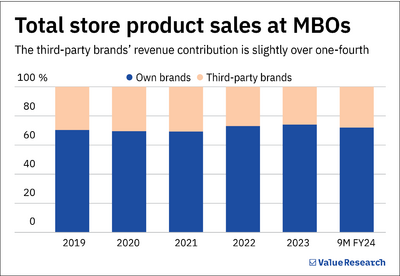

Partnering with Metro Brands further gives global companies a head start, as they get quick access to the company's 612 MBOs in 192 cities (as of 9M FY24). Metro, too, gains over one-fourth of the total store product sales at MBOs from third-party products.

3) Penetration in the hinterlands

Despite its high average selling price compared to peers, the company makes 40 per cent of its revenue (as of 9M FY24) jointly from tier 2 and tier 3 cities owing to its strong distribution network, market penetration and retailing experience of serving customers of different ethnicities.

4) Good track record

The company has an impressive execution track record, having successfully partnered with and scaled various national and international brands since its inception in 1955. Given its vast retailing experience, it won't be difficult for it to compete with existing giants like Puma, Adidas, and Nike in this segment.

Investors' corner

Since its listing in December 2021, the company's stock has generated a steady return of 45 per cent per annum. However, investors should note that it is trading at a hefty price-to-earnings multiple of 96 times as of March 28, 2024. Also, its asset turnover has deteriorated from 1.4 times in FY19 to 0.8 as on 9M FY24 (TTM basis).

Also read: These companies achieved rapid growth without losing equity

Ask Value Research ![]()