It's that time of the year when many of us who have opted for the old tax regime will be scrambling to find investments that can lower our tax bill.

With so many investment choices out there in the market, picking the right one can be overwhelming. Often, the last-minute rush to save on taxes before the March 31 deadline means that many choose investments that simply qualify for a tax deduction under Section 80C without putting too much thought.

But that's the wrong strategy. Choosing where to invest shouldn't just be about saving taxes. They should be a good investment first and a tax-saving option later. That's because we'll be investing up to Rs 1.5 lakh, which is a significant amount.

So, without wasting more time, let's show you an effective way to determine which tax-saving investments are tailored to your needs based on the following three factors:

- Time horizon of the investment

- Risk appetite

- Liquidity (How easy it is to withdraw the money)

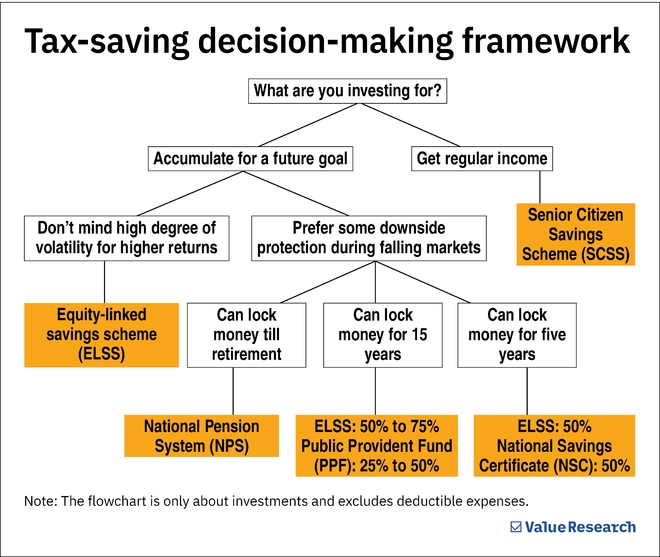

Why ELSS

ELSS (tax-saving mutual fund) invests in equities, and if you give them at least five years, they have generally provided double-digit returns. For instance, even the average ELSS has delivered over 18 per cent annual returns in the last five years as of February 27, 2024. That's because the volatility associated with equity usually flattens if you stay invested for at least five years.

In short, ELSS should be part of your long-term portfolio, regardless of whether you are a conservative or an aggressive investor.

But please note that although ELSS has the shortest lock-in period of three years, and that's not long-term when investing in equity. A three-year investment period can be fraught with market volatility. It would help to have at least a five-year outlook to optimise your equity investments fully.

Why PPF and NSC

Some investors may fear investing in equities through ELSS and look for safer fixed-income options like PPF (Public Provident Fund) and NSC (National Savings Certificate). Although they provide much lesser returns than ELSS, they are relatively safer. So, conservative investors can look at investing partly in NSC/PPF and ELSS.

Why NPS

The National Pension System or NPS (Tier I) comes with strong merits like extra low expenses, additional tax benefits and so on. Although its lock-in period until retirement is seen as a disadvantage, it is a blessing in disguise for investors who find it difficult to be disciplined with their retirement savings. Which means if you are looking for a retirement solution with the added benefit of tax savings each year, opt for the NPS.

What's more, unlike all the other options, NPS allows you to claim a tax deduction of up to Rs 2 lakh under the old tax regime. The others have a limit of Rs 1.5 lakh only.

Why SCSS

For a regular-income-seeker above 60 years, the automatic choice is the Senior Citizens' Savings Scheme (SCSS). The 8.2 per cent per annum it currently yields is higher than any other fixed-income alternative. It is also the safest option, as it comes with a sovereign guarantee and offers regular interest. Although the interest income is taxable, senior citizens above 60 get tax exemption for up to Rs 50,000 interest earned in a financial year.

The only downside is that it has a maximum limit of Rs 30 lakh per subscriber. It is Rs 60 lakh in case of joint holding with your spouse. Once that limit is exhausted, the investor cannot make incremental investments. So, one cannot rely on SCSS for tax savings year after year.

Also, please note that a portfolio made up only of fixed-income investments (SCSS being one of them) is not appropriate for an income-seeker. The portfolio must have at least 33 per cent of equity allocation to ensure your retirement corpus doesn't run out.

To conclude, the flowchart caters to all types of investors (the safe and the aggressive). Not only will it help you make the right decision, but it will also help you make a quick decision, which is essential as the deadline to invest in tax-saving options is March 31.

Also read: A legal hack to further reduce your taxes

This article was originally published on February 27, 2024.

Ask Value Research ![]()