"Forever". That's Warren Buffett's standard answer when asked, "For how long should you hold your investment?"

While we at Value Research are also advocates of buy and hold for the long term, the success of an investment ultimately lies in selling. In the words of our CEO, Dhirendra Kumar, "There is no such thing as buying well; there is only selling well. Because if you don't sell well, then the buying does not matter."

The key here is to sell well. So, here are six questions you must ask before selling your mutual fund investments.

1) Does the change in fund manager warrant a sale?

Although fund houses downplay the effect of a change in fund manager, in reality, it can significantly influence performance, for good or bad.

For instance, the HDFC ELSS Tax Saver Fund saw a turnaround in 2022 after a new fund manager took over. Conversely, the Motilal Flexi Cap Fund experienced a decline in performance after its long-term manager departed in 2019.

These two examples highlight the uncertainty of managerial changes.

That said, the mutual fund industry is prone to changes. So, switching funds each time a fund manager changes is impractical. Instead, sell your fund only if the longest-serving manager changes or if you had initially invested in the fund because of its fund manager.

You can also consider selling your fund if there's a change in the fund house's CIO (chief investment officer). That's because CIOs often set the investment style of a fund house, and any churn in this space can alter that philosophy.

2) Can you manage your mutual fund investments on your own?

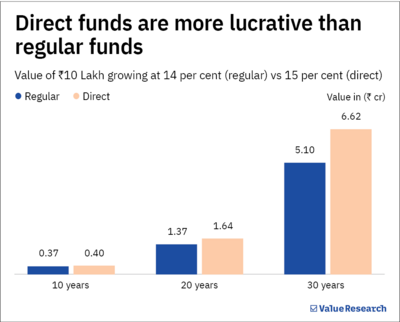

Direct equity plans generally deliver one per cent higher returns than regular funds, as they charge a lower expense ratio. In other words, they can generate more wealth in the long run, as you can see in the table below.

So, to maximise returns, consider selling your regular funds for direct funds. But before doing that, ensure you possess adequate knowledge for managing these funds by yourself.

3) Is your goal fast approaching?

The ideal time to sell your mutual fund is on the cusp of achieving your financial goal. However, since markets can be volatile, this strategy can be risky

Consider a scenario where you have diligently invested in equity funds for your child's education since 2015. We are all aware of what happened in March 2020. The markets slumped worldwide owing to the Covid-19 pandemic. The Sensex fell about 37 per cent from the start of the year.

Imagine what would have happened if your child's education goal had been due in early April or the end of March, with all your money in equities. A corpus of Rs 1 crore at the beginning of 2020 would have reduced to just Rs 63 lakh.

Therefore, to avoid such a nightmare, start an SWP (systematic withdrawal plan) at least two to three years before you are about to reach your long-term goal. An SWP allows you to withdraw in a phased manner and protects you from moving out all your investments at a market low. It averages the price at which you exit the market.

So, start an SWP and put the amount you have withdrawn into a liquid fund.

4) Has there been a drastic drop in ratings recently?

Much like we check Rotten Tomatoes score before watching a movie, Value Research ratings can be a similar starting point for investors to judge a mutual fund.

If the ratings of a fund decline rapidly, sell it.

That said, if the fund has a strong performance history, we suggest you wait a year or two before jumping ship. Because form is temporary and class is permanent.

Meanwhile, give it three to six months if it's a new fund. If the fund doesn't improve within that time, sell it.

5) Does the change in fund strategy align with your risk profile?

Consider Quant's mid and small-cap funds. Before 2018, they used to be aggressive and conservative hybrids. For those unfamiliar, conservative hybrids are relatively safe funds, typically investing 75 to 90 per cent in fixed income and a small portion in equity, while small-cap funds are bang opposite to them, focusing on riskier small-cap stocks.

When a fund changes its objective or style, ensure it matches your risk profile and investment goals, or look for alternatives that do.

6) Is the fund underperforming its benchmark?

Many investors resist selling, hoping that they'll eventually bounce back.

But that only happens a few times. An underperforming fund over three years is likely to remain a dud over five years, too. In fact, there's a 77 per cent chance that it will remain a laggard.

In short, you're simply delaying in cutting your losses.

The last word

The decision to sell your mutual fund investments should not be taken lightly. Sure, you may need to sell your mutual funds during an emergency, an unforeseen big purchase, or while rebalancing your portfolio. But on the whole, selling a mutual fund is a nuanced process that requires careful consideration of multiple factors.

This article was originally published on February 12, 2024.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()