The milestone is set. The government's Vision 2047 scheme envisions India becoming a $30 trillion economy to mark the 100th year of an independent India. But to turn this vision into reality, it needs more roads, airports, highways, and, most importantly, cement.

Simply put, India's march towards becoming a developed nation is bound to push the cement industry to new heights. And for investors, this means new opportunities.

So, let's look closer at the cement industry, from how it is made and who the major players are to how to analyse it.

Conjuring the concrete

The first step to analysing any industry is understanding the product and how it is made. When it comes to the cement industry, the first part is rather simple. It is a basic material used to build anything, from schools to airports.

The second part, however, needs a bit of explaining. Cement production starts with mining limestone, which is then mixed and ground with clay and some other materials. Next, this mixture is heated at high temperatures and then cooled to create a hard material called clinker. Then, the clinker is crushed and mixed with gypsum, and that is it. You have your everyday cement.

Nature of the beast

You must decipher the industry dynamics to pick the best from the rest for any industry. The cement industry is a push industry , meaning the focus is on making the products widely available. Marketing and branding take the back seat.

So, how do you know which cement manufacturer is slated for success? There are essentially two factors you should look at to assess if a cement company is worth investing: cost and scale.

Controlling the costs

In a push market, maintaining a cost advantage is key to gaining an edge. So, whoever can maintain quality while keeping a tight lid on costs has significantly higher chances of climbing the industry ladder.

Here are the three major costs for manufacturing cement and the companies saving the most on them.

-

Raw material costs:

The primary raw material for cement is limestone. Manufacturers procure it through mines, which require licences and carry considerable royalty charges. Hence, the trick is to produce the most quantity using the least amount of limestone. Cement producers achieve this by mixing limestone with other materials, such as fly ash and limestone.

Mixing for margins

Adding other materials to clinker reduces overall cost

Items in proportion (%) OPC PPC PSC Clinker 95 65-45 45-25 Gypsum 5 5 5 Flyash - 30-50 - Slag - - 50-70 Total 100 100 100 Margin profile Low Medium High Source: Sciencedirect; OPC stands for Ordinary Portland Cement; PPC stands for Portland Pozzolana Cement; PSC stands for Portland Slag Cement

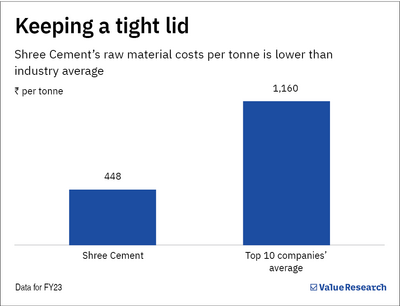

Shree Cement is ahead of most in this and has the lowest raw material costs in the industry. Its blending ratio, a measure of how much fly ash and slag it is mixing with limestone, stood at 77 per cent in FY23. In addition, it procures limestone from multiple locations, which has helped it reduce costs further.

-

Power and fuel costs:

As mentioned earlier, you need heat to make cement. Thus, fuel costs account for a bulk of production costs, nearly 40 to 50 per cent. So, manufacturers are always on the lookout for cheaper alternative fuels (alternative to coal and pet coke).

Dalmia Bharat leads the pack in this regard and has consistently increased its thermal substitution rate (the proportion of heat derived from alternative energy sources); it grew to 17 per cent in FY23 from 5 per cent in FY19.

-

Transportation costs.

Cement is bulky. Hence, transporting it requires a considerable amount of effort and money. So, cement makers are always looking for innovative ways to reduce transportation costs.

Ramco Cements , for example, uses a mix of trains, trucks, and ships, ensuring minimal transportation costs. Similarly, Dalmia Bharat has created a digital platform to bid for shipping services, helping them choose the best deals and save money.

Economies of scale

We had established earlier that to make a name in the cement industry, companies must make their product readily available. In simple terms, it's a volume game. The higher the production capacity, the more cement it can produce and push out. Also, manufacturing cement has a lot of fixed costs. So, spreading these costs over larger volumes reduces per-unit costs.

In terms of scale, UltraTech Cement is clear of the rest, with an impressive total production capacity of 132 metric tonnes per annum (as of FY23). This enormous production capacity helped it lead the industry in terms of profitability despite not dominating the cost aspects. As of FY23, it had the highest operating margin in the industry. In addition, its scale has ensured lower depreciation costs as a percentage of its sales compared to its peers.

Standing tall among giants

UltraTech commands the highest margin

| Company | EBITDA per tonne (Rs) | Operating profit margin (%) | Capacity (MTPA) |

|---|---|---|---|

| Dalmia Bharat | 901 | 7.8 | 44 |

| Shree Cement | 925 | 9.2 | 46.4 |

| Ramco Cement | 789 | 9.3 | 22 |

| UltraTech Cement | 1005 | 12.2 | 132 |

| Data as of FY23 | |||

A word for investors

Note that the above article is purely for educational purposes. Our aim is to help you make more informed decisions while investing. We are not presenting a recommendation case for any of these companies.

There are several more factors you must consider, especially your risk appetite. The cement industry can be highly cyclical and volatile. In addition, we have not delved into the management history and other qualitative aspects of the companies mentioned above.

Hence, use the above article as a guidebook for analysing the cement industry. But before investing, do the due diligence.

Also read: The auto parts industry is accelerating ahead

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()