While consistent revenue and earnings growth are crucial, every investor seeks share price growth as their primary objective. And the recent performance of Laurus Labs may have left its shareholders disappointed.

Despite reporting impressive growth in revenue and earnings from FY20 to FY23, the company struggled to maintain the same momentum in this financial year. In fact, during the second quarter of FY24, its revenue and net profit declined by 22 and 83 per cent, respectively, on a year-on-year (YoY) basis.

Consequently, the stock price plummeted from its peak of Rs 707 in August 2021 to Rs 397 on December 19, 2023, marking an annual decline of 27.5 per cent.

Before delving into the current slump, let's reflect on the factors that fueled the company's initial growth.

Growth from revenue diversification

Laurus Labs primarily generates its revenue from the API (active pharmaceutical ingredients) segment, until FY18. Within this segment, antiretrovirals (ARVs) stood out as the major revenue driver, constituting a significant 74 per cent of the total revenue. In contrast, the CDMO (contract development and manufacturing organisation) segment contributed a relatively modest 11 per cent to the overall revenue.

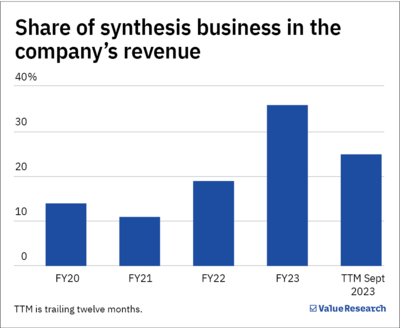

To enhance revenue diversification, the management strategically shifted focus to generic formulations and synthesis. This move paid off, as evidenced by the FY23 numbers, with the revenue share of ARV dropping to 37 per cent and the CDMO share rising to 36 per cent.

The synthesis CDMO segment became a game-changer, driving both revenue and net profit to annual growth rates of 27 per cent and 70 per cent, respectively, over the last five years. Revenue stream diversification also led to an improved product mix, elevating the operating margin from 14 per cent in FY18 to 21 per cent in FY23.

Laurus Labs: Financial performance over last five years

Profitability and ROE have shrunk significantly in the last 12 months

| TTM | FY23 | FY22 | FY21 | FY20 | |

|---|---|---|---|---|---|

| Revenue (Rs cr) | 5332 | 6041 | 4936 | 4814 | 2832 |

| PAT (Rs cr) | 378 | 797 | 832 | 984 | 255 |

| Operating margin (%) | 12.9 | 21 | 23.7 | 28 | 13.3 |

| ROE (%) | 9.1 | 21.6 | 28.1 | 45.2 | 15.4 |

|

PAT is profit after tax ROE is return on equity TTM is trailing twelve months |

|||||

The present

In FY24, though, the company has faced multiple challenges. Downward pressure on key API prices in the US and European markets and disappointing performance in the high-margin synthesis business impacted revenue and profit margins.

The CDMO segment, which saw substantial growth due to a large order in FY22, faltered as the company failed to secure significant orders. This resulted in a 69 per cent YoY decline in revenue in the second quarter.

Although revenue from formulations increased by 24 per cent in the first half of FY24, subsequent price erosion in the formulation business caused a sharp drop. Its operating margin shrunk from 23.3 per cent in the second quarter of FY23 to 7.7 per cent in the recent quarter.

The road ahead

An adverse macro environment and heightened competition continue challenging the company's performance in the current fiscal year.

Despite an increase in sales volume in the API and formulations segment, the unpredictable pricing and the business environment make the turnaround difficult for Laurus Labs.

Furthermore, the company has incurred substantial capital expenditures, approximately Rs 2,900 crore in the last three years, primarily directed towards the synthesis and CDMO business. The company expanded its manufacturing facilities and ventured into the synthesis business of animal healthcare, whose commercial operations commenced in October 2023. Only time will tell if the management's bet on the synthesis business will benefit the company and its shareholders in the long run.

Also read: Kalyan Jewellers: Sparkling growth

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()