Don't we have January 1 every year? It's just another day on the calendar; just the year changes. Yet, we get excited to start afresh and give ourselves a chance to improve from the previous year. And why not? January is named after Janus, a Roman god with one face looking forward to future possibilities and the other looking back at what has transpired.

Since January has been so deeply rooted in the concept of transitions and new beginnings, it is a good time to up our money game.

But that's easier said than done. Overcoming blind spots can be overwhelming as you may not know where to start. This is why we give you simple, easy-to-follow money moves to rewire your finances. So, without wasting your time, let's dive in.

Set your financial goals

Just like we decide on a destination before heading for a vacation, we first identify our financial goals to get money smart. So, here's how you set your financial goals:

Define broad goals (such as car/home purchase, vacation, etc.)

- Use our free 'Goal Calculator' to plan the amount and investment required.

- If goals are already set, follow up on their progress

- Ask yourself if a goal is negotiable or non-negotiable. A car purchase can wait, but higher education cannot.

4 Million+ copies sold! Get investment insights, market guidance, fund analysis, data stories, case studies and more. Subscribe to our digital & print magazine - Mutual Fund Insight.

Based on your goal and timeframe, invest in either equity or debt

For long-term goals (five years or more), invest in equity as they tend to provide high returns in the long run. For beginners, equity-oriented mutual funds are ideal, especially aggressive hybrid funds.

For short-term goals, park your money in debt. Short-duration debt funds can be a smart choice.

Fancy investment options seem attractive. But stay away from them. Last year's crypto bloodbath is a cautionary tale. Even then, if you want to be a thrill-seeker, invest at most 5-10 per cent of your money.

Kill your debt

Often an ignored topic, but an increasing number of young Indians are getting trapped in debt. While vacations and experiences are always welcome, the expenses can increase your blood pressure. So, here's what you should do:

If you are already in a debt trap

Pay off credit card debt at the earliest.

If possible, make one additional EMI payment on the outstanding amount.

Move credit card debt from one card to another at 0 per cent interest rate (for a billing cycle) or at a lower rate than the previous card.

If you are planning on taking easy loans or no-cost EMI

We don't realise, but we pay interest/charges in some form for even no-cost EMIs. There are no free lunches in life.

Make a budget (and stay within it)

Sounds simple, but only some people follow this resolution. It's an underdog in the truest sense. A harmless number-crunching at the start of the month can save you from overspending and make you conscious of how and where you spend.

Use the 50-30-20 rule

Use the 'golden rule' of budgeting, where you allocate 50 per cent of the money for your needs, 30 per cent for wants, and 20 per cent for investing. Try to stick to this rule as much as possible.

Use a specific card for a particular stream of expenses. For example, one account can be used for investing through SIPs, while another can service your needs (rent, travel, etc.).

Plan your taxes early

By being proactive, you can actually save a lot of tax and last-minute stress.

Plan your Section 80C tax deductions at the start of the financial year (April), not in February or March.

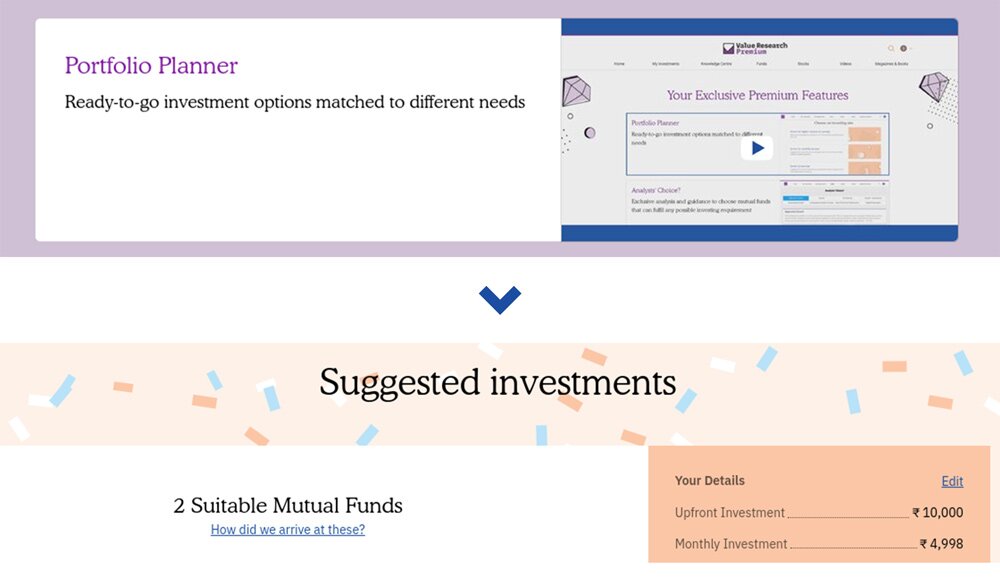

Save in tax-saving mutual funds, National Pension Scheme (NPS), etc., to lower your tax outgo. Looking for our recommended funds to save taxes? Login to our portfolio planner to get suggested funds.

Beyond 80C, there are a bunch of allowances and deductions to reduce your tax burden. House rent, home loan repayment and tuition fees are a few tax-saving avenues.

Check if you paid less tax in 2022. If so, plan your cash outflow in the last financial quarter.

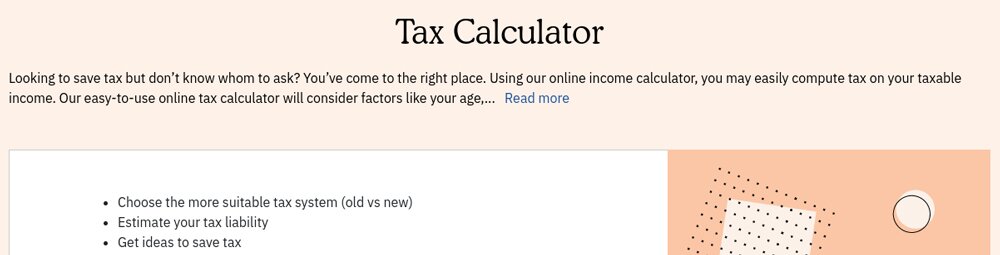

You can use our free 'Tax Calculator' to determine your tax liability. You'd get recommended suggestions as well.

Cover yourself well

What's the use of investing if you have to withdraw all of them during an emergency?

This is why you should have an emergency fund. Keep six to 12 months of your monthly expenses in that account. This can come in handy in a job loss, medical emergency, etc.

Get health insurance. It is a must since hospital expenses can cost you an arm and a leg.

Do you have a young family or parents who rely on your salary? If so, get life insurance. Term plans are the best and most cost-effective. Refrain from falling for endowment policies or ULIPs.

In a nutshell, there's no more room for procrastination. Follow these five resolutions and you'll be surprised how confident you'll feel this time next year.

So, let's get to work and up our money game.

Suggested read: The number on the calendar

This article was originally published on January 30, 2023.

Ask Value Research ![]()