Public sector banks (PSBs) have had a dream run in the markets so far this year. And yet, barring State Bank of India, they have received little tender-loving-care from mutual funds, who have instead kept their faith with private bank stocks.

A champagne 2022

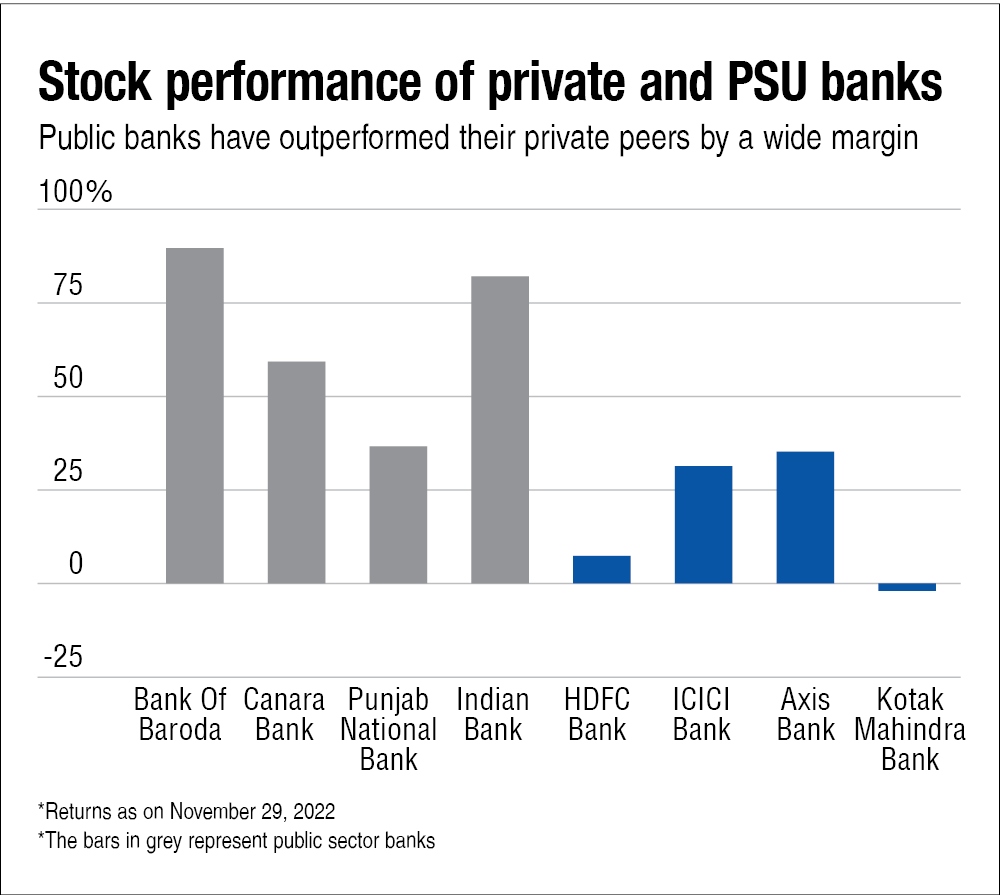

Some public sector bank stocks zoomed 30 to 90 per cent in the last one year, comfortably outpacing their private peers (as seen in the graph below).

In fact, the average returns of government-backed banks have been three times higher than their private counterparts.

Reasons for PSB sparkle

Higher recoveries and write-offs have helped public banks shrink their total bad loans amount.

Government's decision to create asset reconstruction companies (ARCs) have also helped matters. How? ARCs buy bad assets from banks to clean their balance sheet.

The ongoing consolidation of public banks has worked in their favour too. The now-larger banks have the capacity to finance larger projects.

On the other hand, public sector lenders have no such restrictions, with seven of the 12 public banks having over 80 per cent promoter holdings. Since there are lower levels of traded shares, even a slightly good performance can lead to a surge in their stock prices. A classic case of demand and supply.

Feeling is not mutual

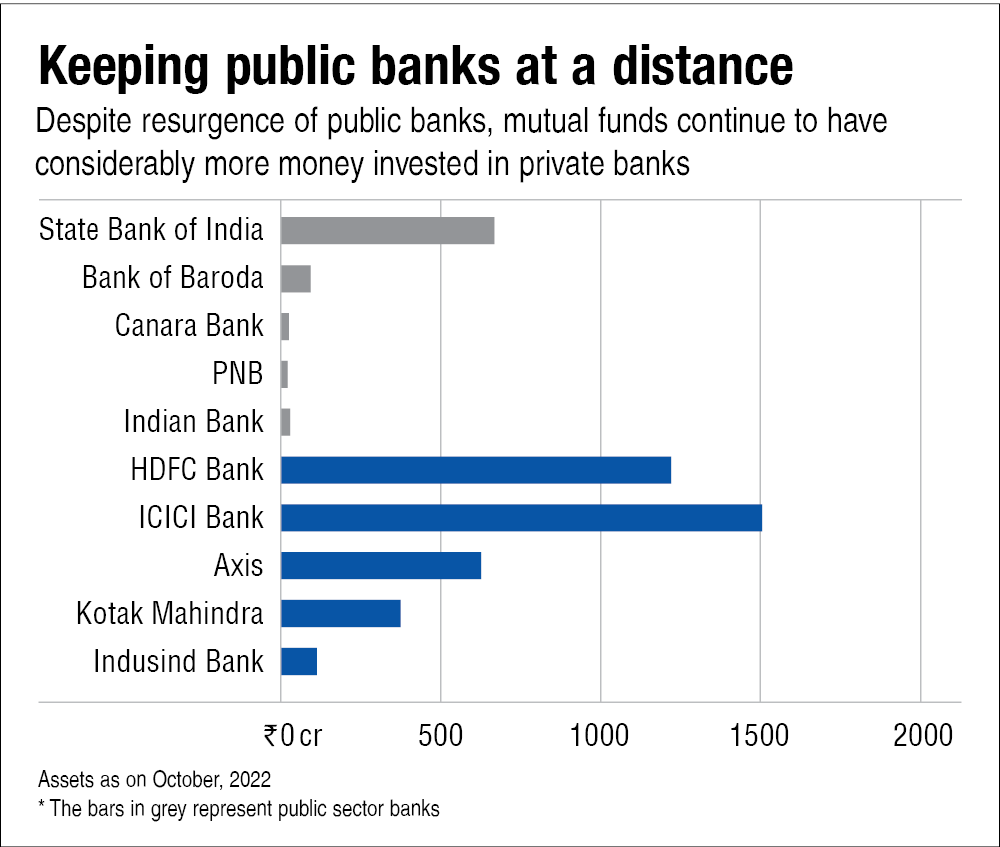

Despite reaping rich returns, government banks have found few takers in the mutual fund universe.

As on October end, mutual funds have deployed close to Rs 3.84 lakh crore in top five private banks, while investment in top PSBs stands at Rs 82,892.88 crore.

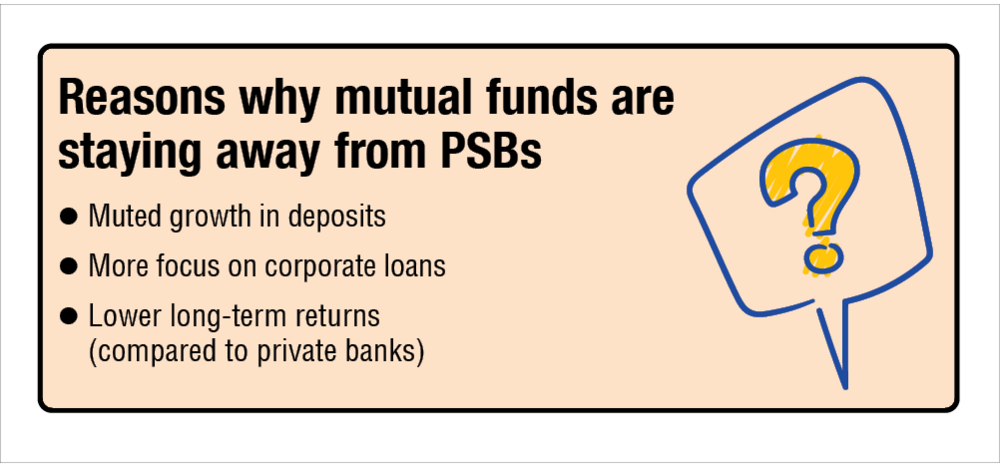

Why the step-motherly treatment?

Private banks are rapidly closing the public sector's gap in deposits. As per Reserve Bank of India March 30 2022 data, private lenders' deposit pace grew at 13.3 per cent from previous year - almost 50 per cent more than public sector banks.

Why are growing deposits good for banks? They can use this money to offer more loans, diversify their loan business and invest them for profit.

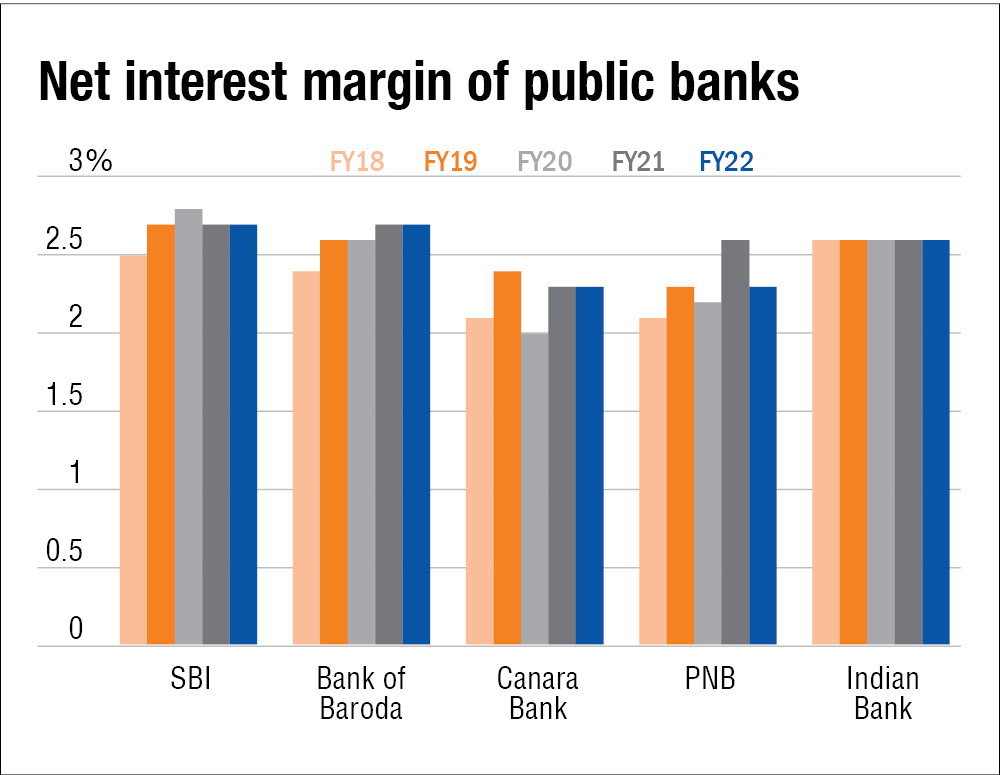

Over the years, government lenders have earned lesser NIM as compared to private banks. In addition, they have lagged behind in adoption of technology, branch networks and overall cost structures.

All these issues were further highlighted by a fund manager on the condition of anonymity: "Leaving top banks like State Bank of India, PSU banks don't have great technology. They are not much into branch expansion mode either. If they don't open branches, it'll be very difficult to get deposits growth. Also, the returns have plateaued and there isn't much upside from hereon for most public sector banks."

Ask Value Research ![]()