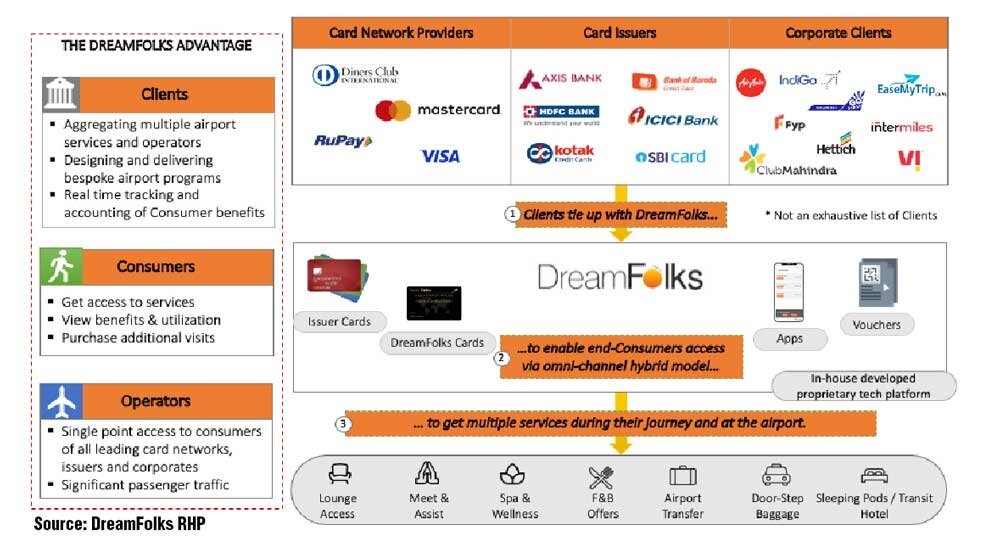

DreamFolks is India's largest airport service aggregator platform. The company has a technological platform where its clients (card issuers, airlines, and other airport service providers) offer a range of services that customers can choose according to their needs, such as lounges, food & beverage, spa, meet & assist, airport transfer, transit hotels, and baggage services. The image below explains the company's business model perfectly:

DreamFolks operates in all the airport lounges in India, has a 95 per cent market share in card-based access to airports, and accounts for 68 per cent of all lounge access volumes in India. The company is present in 1,416 touch points with 244 in India and the remaining overseas. The company has tie-ups with all five card networks, all major card issuers, and also with prominent airline companies.

The number of air travellers in India is expected to grow at 36 per cent CAGR from 2021 to 2025. The 44 per cent growth witnessed between 2016 and 2019 is an example of that. This, combined with ease of access and facilities provided, is expected to increase the number of people who use lounge services.

Strengths:

1) Market domination: DreamFolks is India's largest lounge access provider. 80 per cent of all lounge access was done through debit and credit cards in FY22, and DreamFolks has a 95 per cent market share in card-based access to lounges. The company also operates in all airport lounges in India and is the exclusive platform to access 12 lounges which account for 22 per cent of all lounge access.

2) Strong relationship with clients: DreamFolks has tie-ups with all card networks in India - Visa, Mastercard, Diners/Discover, and Rupay. It also has a good relationship with all major card issuers - HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra Bank, and SBI Cards. DreamFolks also has strong relationships with marquee airline companies such as Indigo, Go Airlines, and Air Asia.

3) Moated business: The company's moat comes from giving a win to both card issuers and lounge operators. Due to DreamFolks' access to all the lounges, card issuers and networks are interested and maintaining a relationship with the company. On the other hand, due to DreamFolks' relationship with card issuers and networks, lounge operators maintain a relationship with the company. Both of these build upon each other through expansion and thus give a moat to the company.

Weaknesses:

1) Dependence on the air travel industry: DreamFolks' whole operations are heavily dependent on the air travel industry and its growth. While there is nothing wrong with this inherently and the number is only expected to grow going forward, events like COVID can have a drastic impact on operations. In FY21, when the whole country was affected by the COVID pandemic, DreamFolks reported a loss and its revenue fell by 71 per cent. If any such event occurs in the future, it would be catastrophic.

2) Card issuers and regulations: The company is heavily dependent on the ability of card issuers and card networks to get new customers. Card issuers and networks contribute 99 per cent of the company's revenue. If there is any stagnation or even regulations barring these companies from onboarding new customers, it will have an impact on DreamFolks as only this volume will help them increase their revenues.

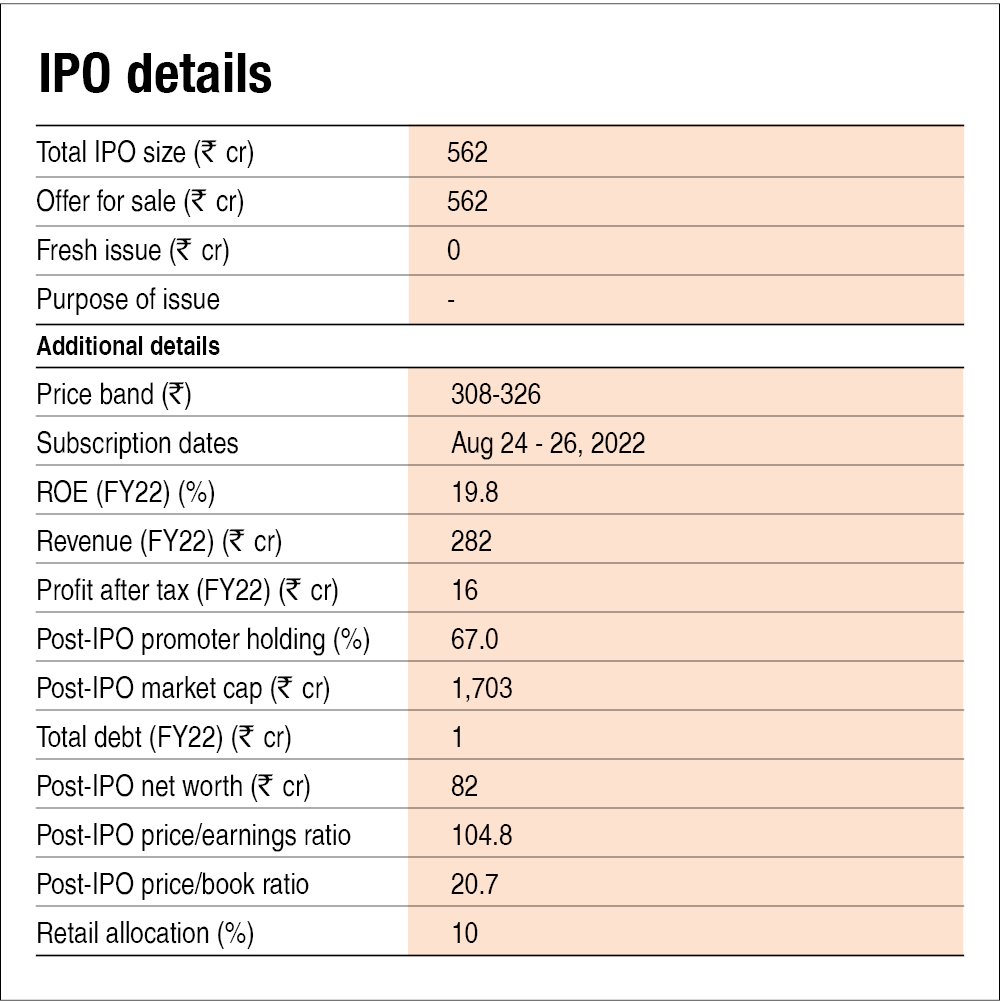

3) High valuations: At the upper price band, the company has a price-to-earnings (P/E ratio) of 105 times and a price-to-book (P/B ratio) value of 21 times. This is a high valuation compared to its earnings yield of just 1.3 per cent. While points such as the only player in the industry are agreeable, such high valuations may not be sustainable in the long run.

Also read DreamFolks Services IPO: How good is it? to learn how we evaluate the company on various metrics.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()