Right off the bat, we'd like to mention that SIP (systematic investment plan) is a much superior alternative to the lumpsum method because it solves four big problems that people face while starting their investing journey:

Option to invest small amounts: The SIP facility allows you to invest in mutual funds starting at just Rs 500 every month. If you think what difference such a small monthly investment can make, we can factually say that slowly but steadily, your money will start growing, leading to a bigger corpus over time.

Reduces risk: In fact, starting small can be better in hindsight. Because even if you make mistakes initially, a large amount of money would not be at stake. On the contrary, if you keep waiting to accumulate a sizable amount before making your first mutual fund investment, you may be too late. That's because your mutual fund investments, if given time, can grow rapidly.

Lack of discipline: Most of us often struggle to stick to our investment plan. Sometimes, it is the temptation to splurge money, sometimes it is the volatility of the stock market that throws us off our plans. This is where an SIP can be really helpful. Here, your money is auto-debited from your bank account every month. Initially, this would help you avoid splurging your hard-earned money and eventually, you would learn financial discipline, which is the secret to growing wealth.

Dealing with stock market volatility: Even the most experienced of investors are unable to time the market, i.e., invest money when the markets are low. This is why lumpsum investing can backfire. What if you invest now and the markets fall soon after?

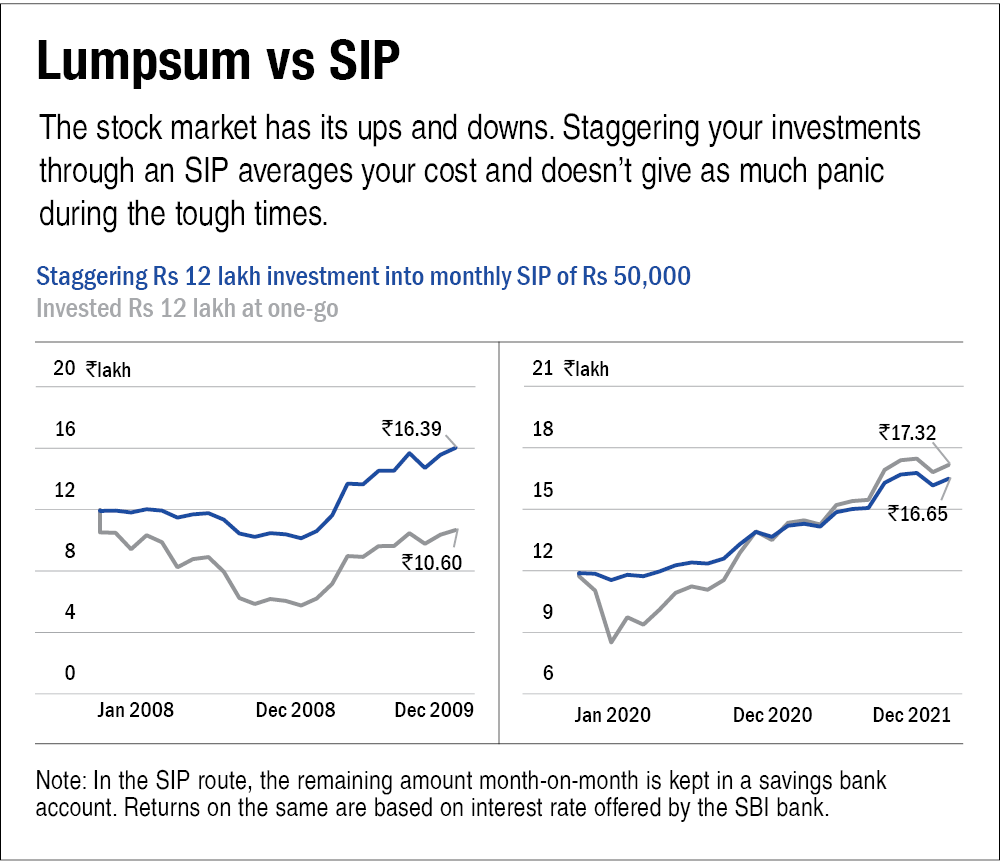

Let's look back at 2008. If you had invested Rs 12 lakh in one go, that investment would have dropped by more than 50 per cent (as seen in the chart below) by the end of the year. Only those who had a very strong risk appetite could see off this phase and see their one-time investment grow back to Rs 10.6 lakh (which is still a loss) by 2009-end.

The SIP route, too, saw a fall during 2008, but the drop was less alarming when compared to lumpsum investment. In addition, the Rs 12 lakh investment grew to Rs 16.39 lakh by the end of 2009, which means an SIP investor made a gain of more than Rs 6 lakh as against a lumpsum investor.

Clearly, SIP beats lumpsum investment when the markets are negative.

However, lumpsum tends to do better when the markets are on the rise, which happened during the first Covid-19 lockdown (seen in the chart to the right). But, as you can see, the rise is marginal.

How does SIP manage to minimise risk? It's due to this concept called rupee-cost averaging. Since SIP allows you to invest every month, you can buy more mutual fund units when the market is down and less units when it goes up. This helps you average out your risk.

Since we can't predict the stock market, doing an SIP is the only viable option to contain the volatility that comes with equity investing. SIPs protect you from sharp losses. This is very crucial as it will help you stick to your investing journey. Under most circumstances and over a sufficiently long period, SIPs will do well enough.

Therefore, if you lack a large lumpsum amount to invest, do not wait to accumulate one. Start with an SIP of however small an amount you can. Believe us, it has the potential to give you big results over the long-term.

In fact, even if you have a big amount to invest, spread that money over a six to 12 months SIP to average your cost and reduce the risk of investing when the market is high. It also helps avoid panic during tough times which leads to a healthy return in the long run.

This article was originally published on June 07, 2022, and last updated on October 13, 2022.

Ask Value Research ![]()