India's largest private sector bank - HDFC Bank, and largest housing finance company - HDFC (Housing Development Finance Corporation) have announced merging their operations. HDFC's board approved the scheme of amalgamation. Share prices of both the companies have jumped 10 per cent till now and may continue to grow. As of April 1, 2022 closing, the merged entity would have a total market capitalisation of Rs 12.8 lakh crore making it the third-largest listed entity behind Reliance Industries and Tata Consultancy Services.

Here are some key points that investors of both companies must be aware of:

- The scheme of amalgamation may take upto 18 months to complete.

- Shareholders of HDFC Ltd will receive 42 fully paid-up equity shares for every 25 shares held by them.

- The equity shares that HDFC Ltd holds in HDFC Bank will be extinguished or cancelled as per the scheme.

- Post-merger, HDFC Bank will be completely owned by the public shareholders. The existing shareholders of HDFC Ltd will hold 41 per cent in the HDFC Bank.

- All the subsidiaries that HDFC Ltd has, such as HDFC Life Insurance and HDFC Asset Management Company would become subsidiaries of HDFC Bank.

- Approval is still pending from shareholders, creditors and regulators such as RBI, IRDAI, CCI, and SEBI.

- Sashidhar Jagdishan, the current CEO of HDFC Bank will continue as CEO post merger. All the employees of HDFC Ltd, including the senior management, would be retained.

What is the purpose of the merger?

The merger has been announced due to both strategic and regulatory reasons. Over the last few years, regulations for banks and NBFCs (Non-Banking Financial Company) have been harmonised, which enabled the merger. This has been in the news since 2015 when HDFC Ltd's Chairman Deepak Parekh stated that they would consider a merger given the right circumstances.

One major reason for this is that there is no significant incentive for being an NBFC. India's central bank, RBI has been tightening the rules over the years. The top NBFCs would have to comply with regulations that are closely similar to those of banks. It makes more sense for the housing finance giant to merge with its huge banking arm. It has been said that the regulations are stringent as RBI does not want NBFCs to grow at a similar size to banks while having comparatively liberal rules.

Apart from the regulatory point of view, the merged entity will also have a strategic advantage for both entities which will help them grow.

How will HDFC Ltd benefit?

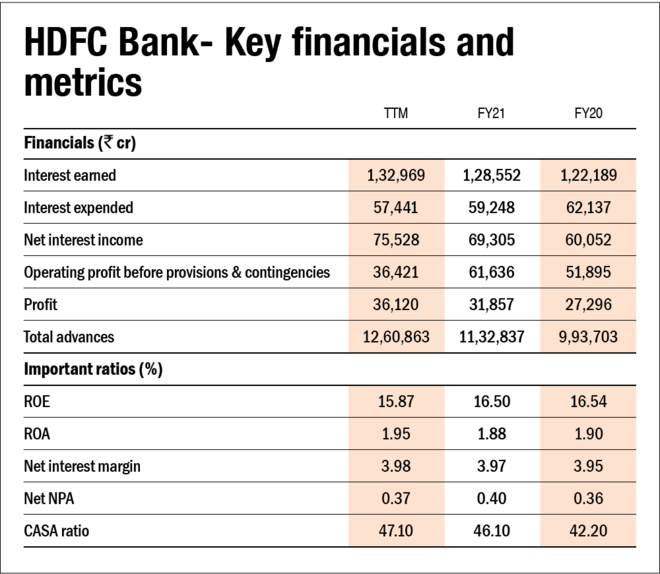

HDFC Ltd will have access to low-cost deposits of HDFC Bank. Normally NBFCs raise capital at a higher rate while traditional banks have access to savings and current deposits which cost much lower. This merger will allow HDFC Ltd to have access to CASA deposits as HDFC Bank has a high CASA ratio of 47.1 per cent as of Dec 31, 2021.

How will HDFC Bank benefit?

HDFC Bank would be able to build its housing loan portfolio. Mortgages will be offered as core products to the customers. At present, the company has 11 per cent exposure to mortgages, and post-merger, the company would have 33 per cent exposure (based on Dec 31, 2021 numbers). This is a massive 200 per cent jump. Total net advances as of Dec 31, 2021, were Rs 12.7 lakh crore, and the total advances for the combined entity would be Rs 17.9 lakh crore, a 38.6 per cent jump. This merger will also result in an increase in its net worth and book value.

This makes it a win-win situation for both entities and their respective shareholders in the long run. The combined entity will have a huge scale which will increase its credit profile and access to customers. This will help fight competition as the housing loan sector is facing attractive tailwinds which will help this segment grow. This will also bring down costs which will increase overall efficiency. At present, HDFC Bank trades at a price to earnings of 25.5 times and a price to book of 3.9 times. HDFC Ltd trades at a price to earnings of 22.1 times and price to book of 2.9 times.

Ask Value Research ![]()