In the first part of the story, we discussed a flow chart that can be used to make a quick decision regarding your tax-saving investments options. Now let's continue further and see what are the best tax-saving options available for you as per your needs.

Seeking regular income

For a regular-income-seeker above 60 years, the automatic choice is the Senior Citizens' Savings Scheme (SCSS). The 7.4 per cent per annum it yields is higher than any other fixed income alternative. It also comes with a sovereign guarantee and gives regular interest. The interest income is taxable, but senior citizens above 60 get tax exemption for up to Rs 50,000 interest earned in a financial year. So, up to Rs 6.75 lakh invested in the scheme will earn tax free interest. Making the income from SCSS completely tax-free has long been on our wish list. It will make this scheme even more attractive.

A portfolio made up only of fixed-income investments is not appropriate for an income-seeker. The portfolio must have some equity allocation (we have talked about this often), which can come from one-two conservatively managed diversified equity funds. Even so, the SCSS fits well in the debt allocation of the overall income portfolio. The only downside is that it has the maximum limit of Rs 15 lakh per subscriber. Once that limit is exhausted, the investor cannot make incremental investments. So, one cannot rely on the SCSS for tax savings year after year.

The other alternatives are tax-saving fixed deposits with a monthly pay-out option and annuity products from life insurance companies. We don't think highly of annuity products. They yield low returns, lack transparency and are often complicated to understand. Beyond the SCSS, a senior citizen should rather forego the tax-saving benefit and focus on other options to generate income than investing in a low-yield scheme to claim tax deduction.

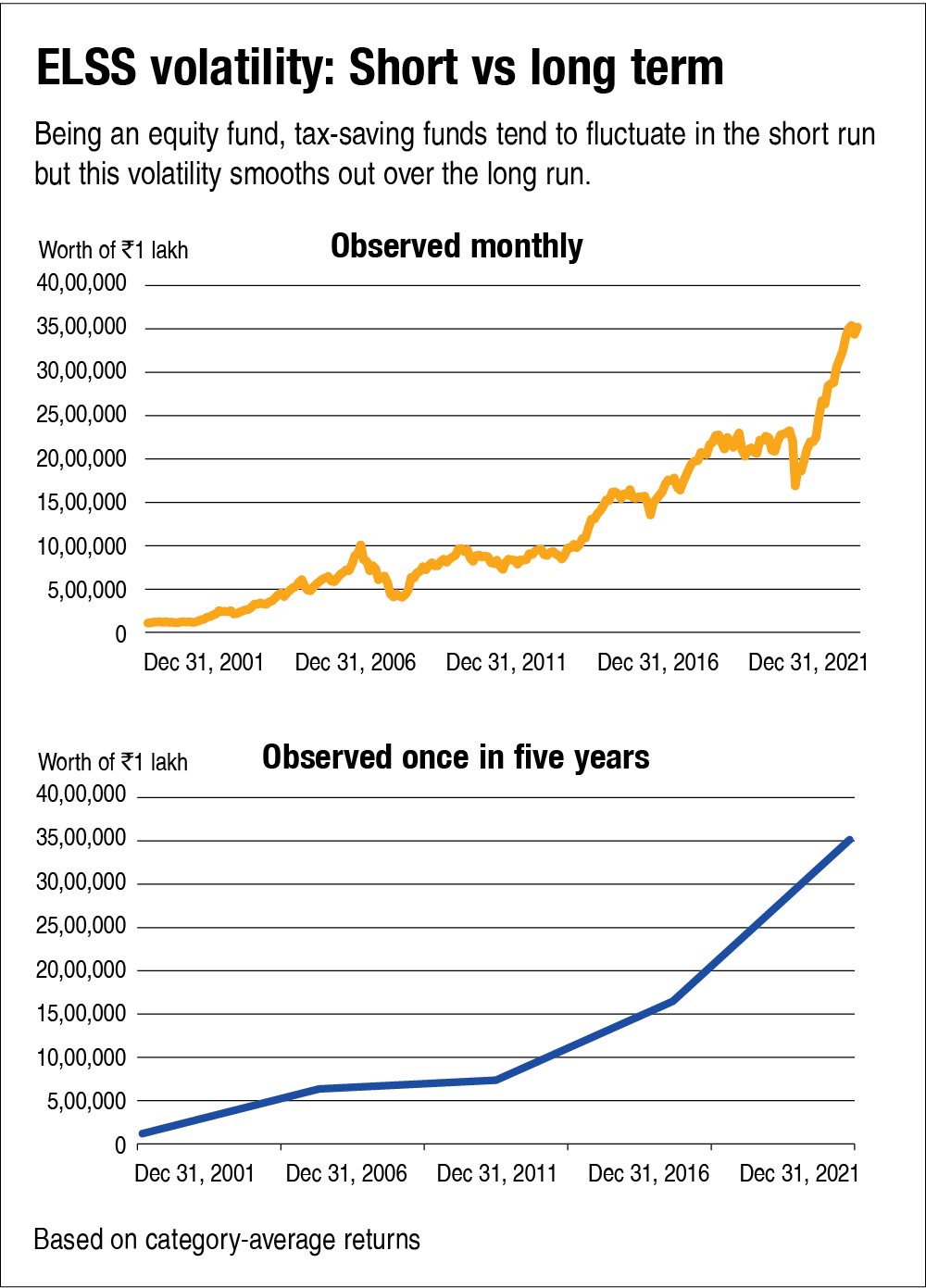

Seeking accumulation with tolerance for high volatility

ELSS needs no introduction to readers of this magazine. For someone who can withstand the ups and downs of equity markets, there is no better alternative than these funds. They measure up very well on all parameters - return potential, liquidity, tax efficiency, transparency and ease of investing. Even the volatility is more of a psychological issue. Looking at your ELSS investments once every five years leaves an entirely different impression than observing them every day, week or month.

The three-year lock-in is desirable because equity investing should anyway have a long-time horizon. Besides, the lock-in often prevents investors from exiting at the worst possible time.

The simplest tax-saving plan for an overwhelming majority of taxpayers should be to pick a good ELSS fund (we have listed our favourites later in this edition) and do a monthly SIP aggregating up to whatever is left of the Section 80C limit after deducting the life insurance premium, mandatory contributions like provident fund and other expenses eligible for deduction.

Many readers ask, 'Do ULIPs make sense now?' With their costs coming down and their capital gains being tax-free, do they now have an upper hand over ELSS? We have done a threadbare analysis decoding the complex cost structure of ULIPs and comparing them against ELSS funds. An objective analysis reveals that the odds are still in favour of ELSS, though our analysis does bring out some interesting observations. Read 'ELSS vs ULIPs: Which is better' for details.

Even after the comparisons, one could still fall for a ULIP unless one is careful. ULIPs have earned such a bad reputation that it has become difficult to sell a plan by calling it a ULIP. At least, knowledgeable investors don't buy these plans anymore. So, insurance agents now say that they have a good 'fund' for tax-saving investments. That 'fund' is actually an equity plan of a ULIP. To call out the subterfuge, just ask the seller if the 'fund' will also give life insurance as a bonus. If the answer is yes, you know you are being sold a monkey disguised as a goat!

Other parts of the story:

Best tax saving options for you

Tax saving plan: Insufficient investable surplus

This article was originally published on March 15, 2022.

Ask Value Research ![]()