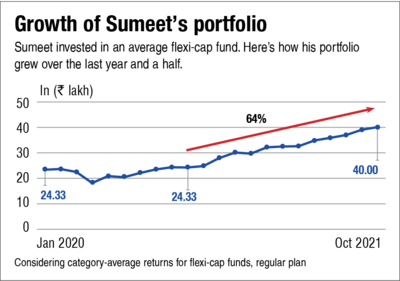

Sumeet (45) has an equity portfolio of about Rs 40 lakh. Amid the ongoing fear of a market crash, he wants to protect the gains that he has earned over the last one year during the bull run. At the same time, Sumeet also fears missing out on the opportunity of getting higher returns if the market continues to rise.

He would need about Rs 20 lakh from this corpus within three years for his daughter's higher education. Sumeet plans to keep the rest of the corpus for his retirement. He wants us to guide him through the dilemma.

Never exit equities in haste

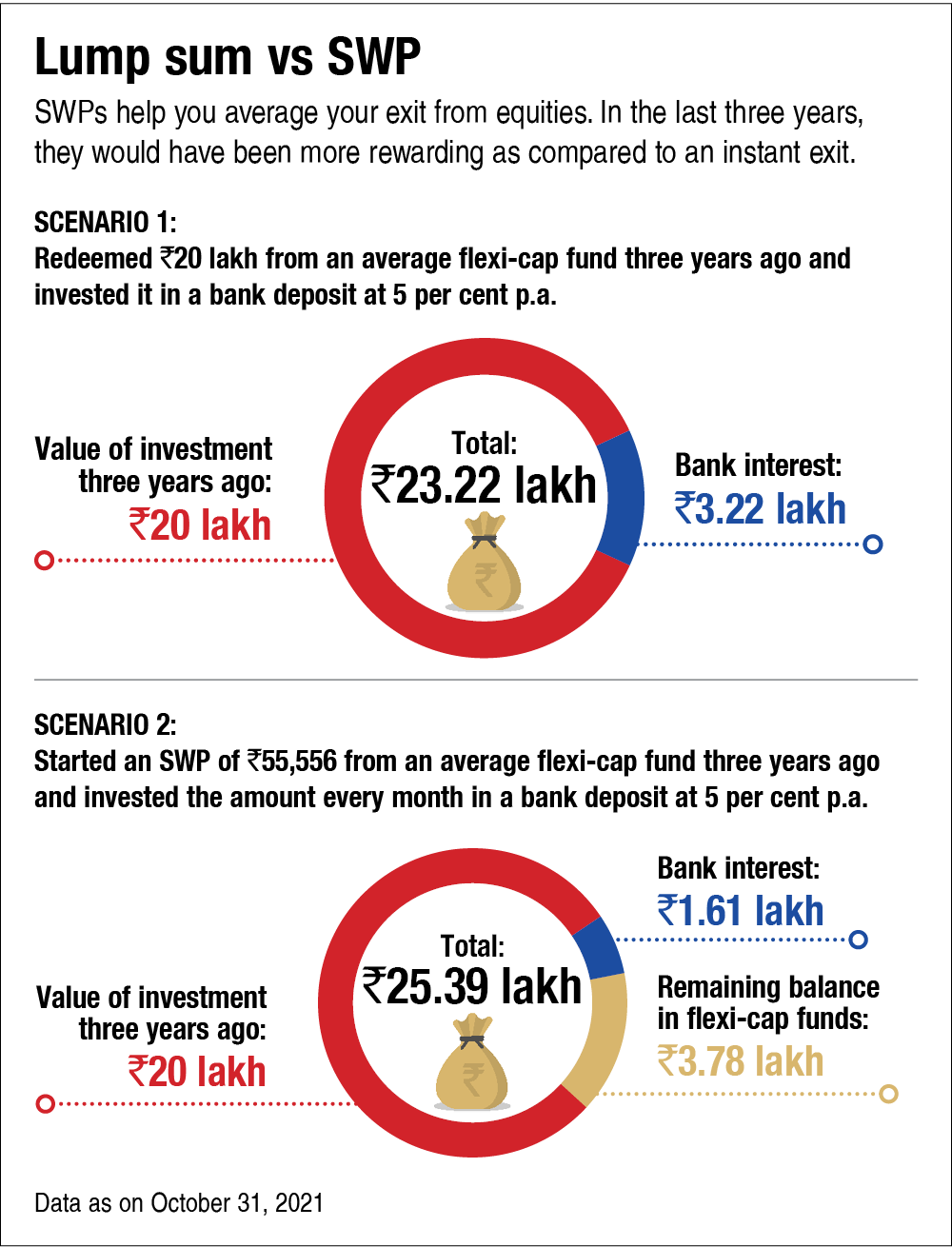

Since equities are highly volatile, Sumeet should not wait till the last moment for a non-negotiable goal like his daughter's higher education. He should rather start redeeming the required money in equal monthly instalments through a systematic withdrawal plan (SWP). Remember, staggering your exit from equities is as important as staggering your investment through SIPs.

When you set up an SWP, a part of your accumulated corpus is transferred to your bank account or the chosen fixed-income fund periodically. Just as SIPs help average the investment cost, SWPs help average your withdrawal. They also ensure that you don't sell out at the bottom. Of course, this also means that you don't sell out at the top either. If Sumeet chooses to move the entire Rs 20 lakh to fixed income at one go, he will lose the opportunity to earn a higher return on this amount if the market rises over the next three years.

Sumeet should also reassess the exact requirement of funds. He may not require Rs 20 lakh at one go after three years. Rather, it is possible that it would be required over time, say three to four years, depending on the duration of the course selected by her daughter. The withdrawal can be planned accordingly. Choosing a fixed-income fund over a bank account will help Sumeet earn higher returns in a tax-efficient way.

Follow an asset-allocation plan

While everyone wants to capture each and every opportunity that the market presents by investing exactly when the market bottoms out and redeeming at the peak just before the fall, doing so consistently is nearly impossible. The only methodical way to deal with this is by following an asset-allocation plan. It helps you automatically book profits when the market rises and invest more when it falls.

Since Sumeet is 15 years away from his retirement, he can follow a 75 (equity): 25 (fixed income) asset-allocation plan for his remaining corpus. However, he should avoid rebalancing the portfolio very often. It should be limited to either once a year or when the actual asset allocation deviates by more than 10 per cent on a sustained basis from the decided allocation.

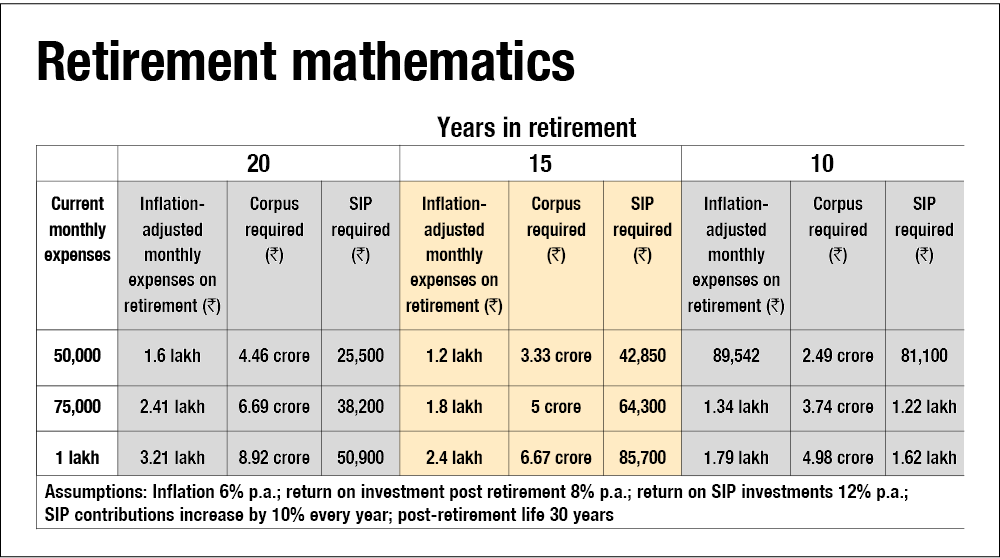

Plan carefully for your retirement

Retirement is a crucial goal and should not be ignored. At an annualised return of 12 per cent, the remaining Rs 20 lakh would fetch Sumeet a little more than Rs 1 crore in 15 years. Often we think that a huge corpus like Rs 1 crore would be sufficient to take care of our post-retirement years. But that may not be the case.

The amount required for a comfortable retirement entirely depends on your monthly expenses that will continue in your old age at an inflation-adjusted level. If need be, Sumeet may consider encouraging his daughter to finance a small portion of her education costs through a loan. It will also teach her financial discipline.

Avoid the noise, stay calm and stick to the investment plan

Due to the pandemic, an air of uncertainty has prevailed over the market and economy in the last one-and-a-half year. Sumeet must stay focused and stick to his investment plan.

One should always avoid making investment-related decisions based on the market noise and hype. One should avoid the urge of acting on daily news. The purpose of watching the news should only be to stay informed. Limiting the news time is one way to reduce impulsive investing decisions.

Keep in mind

- Maintain a contingency fund equivalent to at least your six-month expenses. It should be maintained in a combination of sweep-in deposit and liquid fund.

- An adequate life cover through a pure term plan is a must if you have financial dependents. It should also cover all your outstanding loans.

- One should have adequate health cover for all the family members. It is now more important in view of the pandemic and rising cases of lifestyle-related diseases.

This article was originally published on December 29, 2021.

Ask Value Research ![]()