Credit-risk funds have drawn investors' attention of late as the one-year return differential between them and the remaining debt funds is quite stark. We saw in the previous part what credit-risk funds are and how they have had a roller-coaster ride in the past few years. In this part, we assess whether these funds have learnt lessons from their previous setbacks and if they are now investment worthy.

Have credit-risk funds become safer now?

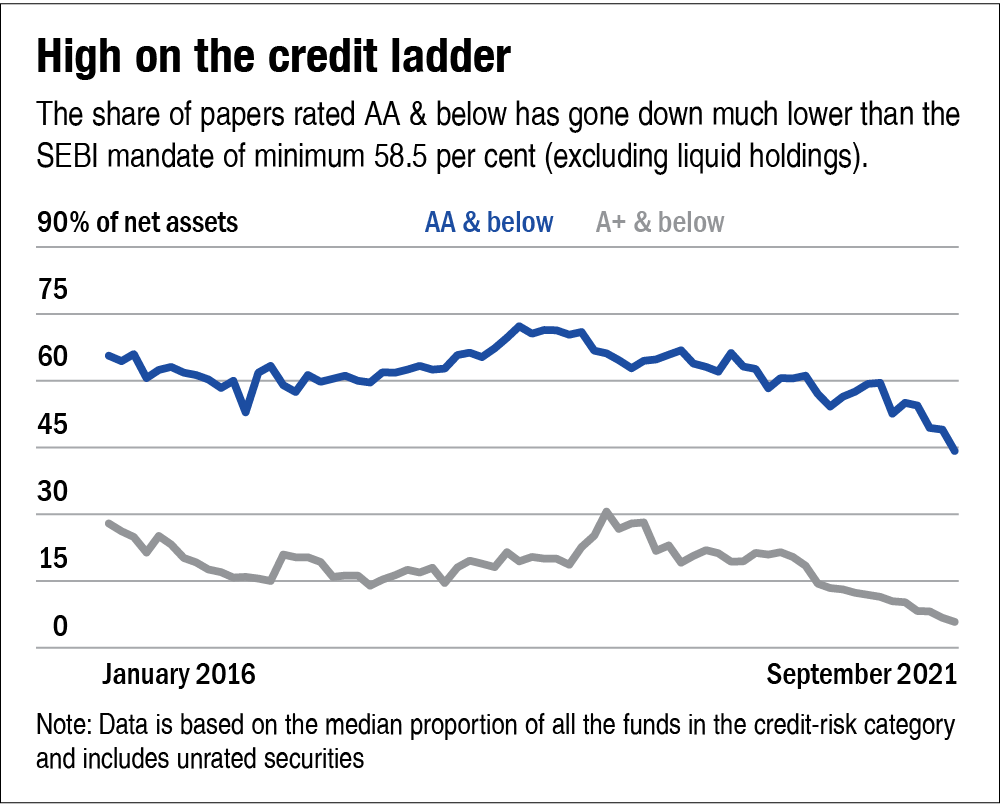

As per SEBI's mandate, credit-risk funds have to invest at least 65 per cent of the assets in papers rated AA & below. However, in a knee-jerk response to the IL&FS and subsequent crises, funds have been on a spree to prune down the share of lower-rated papers. Also, amid the strained liquidity in the corporate-bond markets in mid-2020, AMCs sought the regulator's permission to make additional investments in treasury bills and government securities across credit-risk funds. Later, the SEBI mandated 10 per cent investment in such liquid assets (cash, government securities and the like) to enhance the liquidity of open-end debt funds. Besides, the asset-allocation limit of select fund categories, including credit-risk funds, is now applied after the exclusion of this mandatory liquid holding. So, the threshold of investing in AA & below-rated securities for credit-risk funds effectively comes down to 58.5 per cent (65 per cent of the 90 per cent left after deduction of 10 per cent for liquid assets). However, lately, their share has gone down much lower than this as depicted in the chart 'High on the credit ladder'.

As a popular saying goes, if you find yourself in a hole, stop digging. So, fund houses now seem to be more cautious in their approach. Further, following the outbreak of the pandemic, access to credit facilities has been reduced for borrowers with weaker balance sheets. It ultimately has resulted in an absence of adequate risk-reward opportunities for AMCs, thereby causing this inflexion. So, there has been a general aversion to lousy-rated papers and funds have moved higher on the credit spectrum.

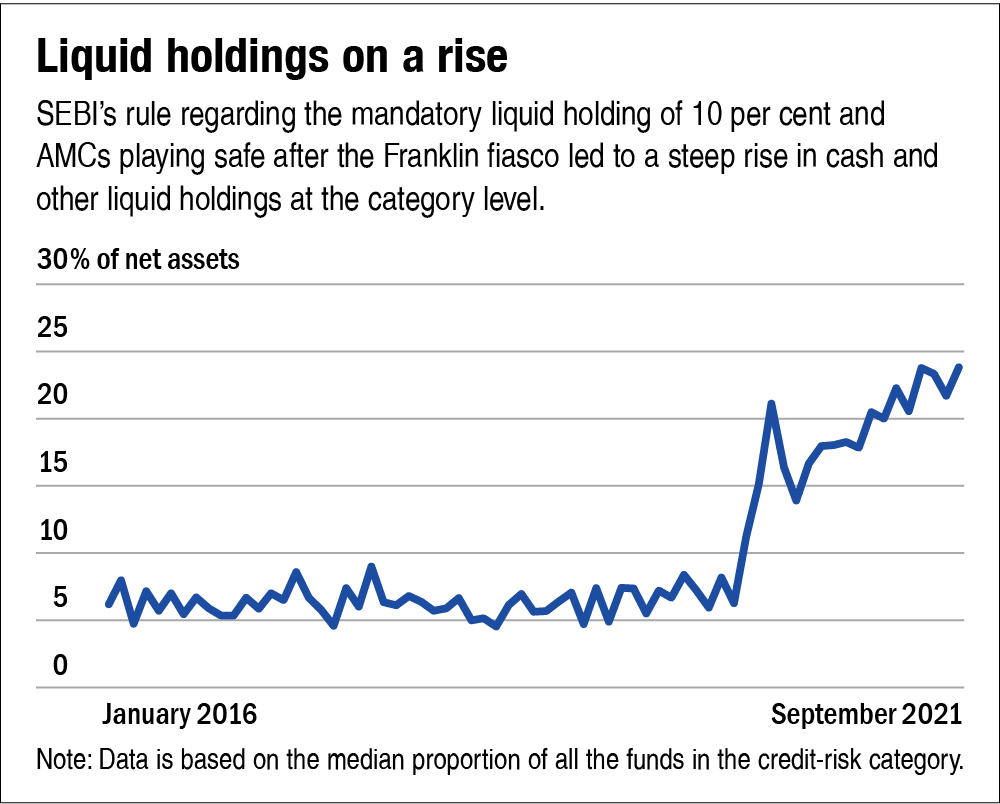

Moreover, a mix of two-three factors has resulted in a steep rise in cash and other liquid holdings at the category level. Refer to the chart 'Liquid holdings on a rise'. SEBI's diktat regarding the mandatory liquid holdings is one reason. Besides, given the Franklin fiasco, AMCs seem to be playing safe to meet sudden massive outflow requests.

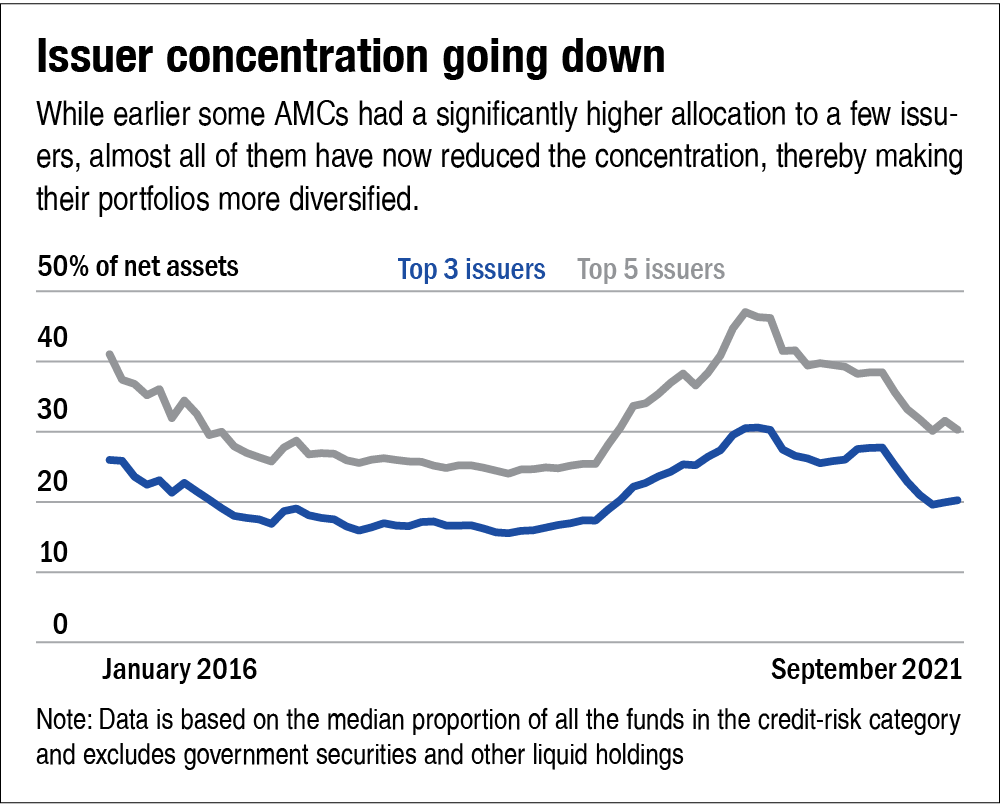

Recently, a reduction in the issuer-level concentration in the portfolio composition of credit-risk funds is another optimistic change. Condensed positions and shoddy credit ratings are a deadly combination. In fact, such funds were hit hardest by the falling AUM on account of defaults /downgrades (DHFL, Essel Group, Vodafone Idea, YES Bank, etc.) and the resulting redemption pressure. As a result, while some funds shut their shop, some took shelter by merging with other schemes. So, while earlier, some AMCs had a significantly higher allocation to a few issuers, almost all of them have now reduced the concentration, thereby making their portfolios more diversified. The declining issuer-level concentration at a category level testifies the fact. See the chart 'Issuer concentration going down'.

The current credit environment

The shaky debt market, coupled with the pandemic, nudged spreads (the gap between the yields of the same tenure but different-rated bonds) to go up in recent years. During the onset of the pandemic, the market feared more corporate defaults on account of a slow economy. However, that did not happen. So, spreads seem to have shown some compression but they look attractive at this juncture as per industry participants.

"Credits remain an attractive play for investors with a three-five-year investment horizon as an improving economic cycle and liquidity support assuage credit-risk concerns, especially in higher quality names. While we remain selective in our selection and rigorous in our due diligence, we believe the current environment is conducive to credit exposure," as per Axis Mutual Fund's 'Sep '21 Debt Outlook Update'. Somewhat similar thoughts are echoed by other fund houses in their recent market updates, suggesting some allocation to non-AAA rated bonds as per individual risk appetite.

All in all, there seems to be a consensus market opinion on embracing credit strategies in a cautious and calibrated manner. So, should you bet on them?

The way forward for investors

We have all heard the old saying that experience is the best teacher. But as Dhirendra Kumar, CEO, Value Research, mentioned in one of his columns, there is a complication to this truth. Bad experiences are good teachers, while good experiences are bad teachers. So, is this the case with credit-risk funds too? Their gala time made them overconfident and the latest agony might hopefully keep them on their toes. But if you ask us, maybe it is too early to be that optimistic.

It is said that a true test of character is not how you are on your best days but how you act on your worst days. But it is the other way round in the case of credit-risk funds. So, we would like to wait and watch. Anyways, the good part is that most retail investors can simply avoid this category and their goals can be accomplished by following other more dependable investing strategies:

For debt allocation: Those investors who are risk-averse with their fixed-income allocation and have a very low tolerance for any negative experience in this segment should stay away from credit-risk funds. For them, versatile categories, like short-duration funds, are a more viable option. Such funds have the flexibility to invest across different kinds of debt securities and they do not take much credit risk by investing heavily in lower-rated bonds.

For regular-income seekers: As we always say, even regular-income seekers should keep some portion of their portfolio in equity. Combining equity with high-quality fixed-income instruments helps navigate income needs as well as beat inflation. Investors can either set their asset allocation themselves or choose to invest in hybrid funds such as conservative hybrid and equity-savings funds.

Finally, some investors may still want to choose credit-risk funds for a limited supplementary fixed-income allocation. But they should have the ability to withstand volatility and a stomach to tolerate the worst scenarios (if they come). They should also avoid putting their short-term money in these funds. But do not forget that fund selection is of utmost importance here. One can find two types of credit-risk funds - some funds follow a cautious and disciplined approach, while some have shown subpar risk-management practices. Ironically, the latter ones have been topping the return charts over the last one year on account of some recovery and the write-back of earlier defaulted/downgraded bonds. So, investors need to look beyond their near-term performance.

Ask Value Research ![]()