The low-interest-rate environment and inflationary economy have reduced the scope for investors to earn meaningful real returns from fixed-income instruments. A sudden fall in interest rates could be attributed to the RBI's accommodative monetary policy, which was aimed at boosting the economy and mitigating the impact of COVID-19. But left in dire straits, regular-income seekers are now looking for better return opportunities.

Against this backdrop, credit-risk funds have started stealing the spotlight. These debt funds seek to earn high returns by investing in lower rated corporate bonds (AA & below), including the unruly unrated papers. However, in a seemingly kabhi khushi, kabhi gham spin, the journey of these funds so far has been quite dramatic. The last three years have underscored the fact that credit-appraisal practices are not very efficient to detect financial stress. Further, the lack of liquidity in lower-rated bonds enhances the risk. But then, from the investment perspective, the importance of yields can't be overlooked either. Fixed-income returns have shrunk massively across the globe, critically hurting those who depend on them for their day-to-day income needs.

Probably, therefore, the credit-risk-fund category has been receiving continuous net inflows since May 2021 and garnered nearly Rs 1,300 crore till September 2021 - a significant turnaround after prolonged net outflows totalling Rs 57,000 crore between April 2019 and April 2021. So, are credit-risk funds a viable option? Have they learnt enough from past misadventures and emerged as a more robust, investment-worthy alternative? Let's find out.

A chequered past

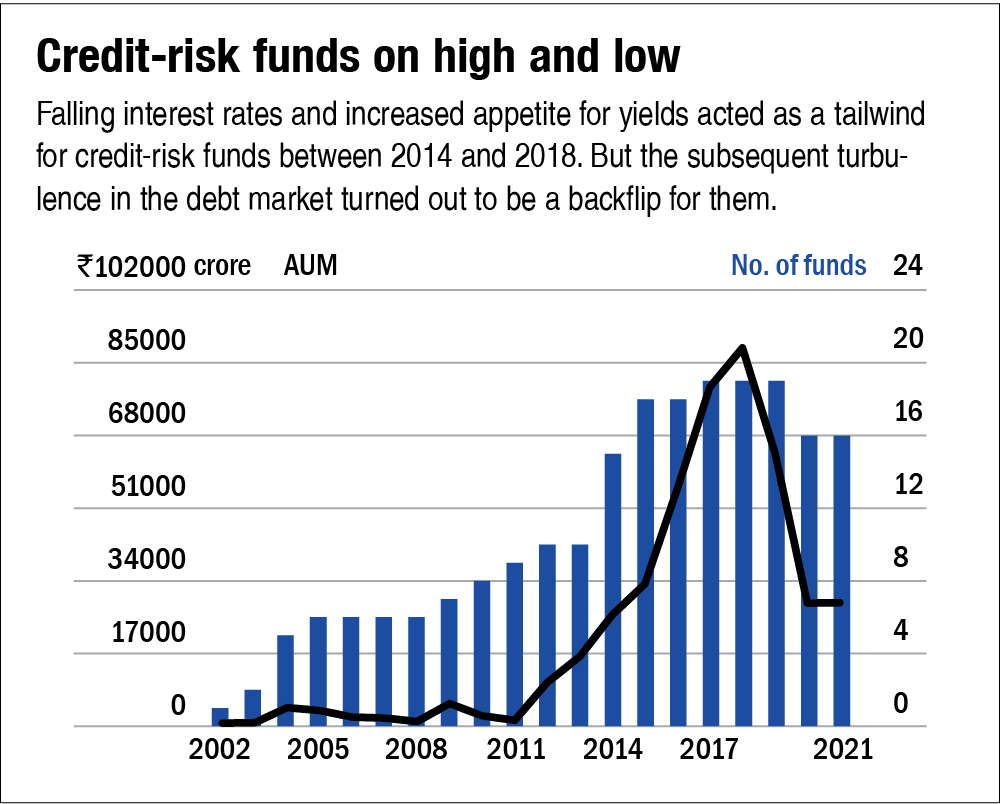

Although the first-ever credit-risk fund came into being in 2002, these funds gained prominence in 2014 when the toddling category had a big run. During this period, interest rates started falling and the focused credit strategy emerged to capture the increased appetite for yields. Since lower-rated securities are more prone to defaults, they provide higher returns to compensate for the additional risk. The strategy proved to be rewarding, as these funds outperformed other relatively high-quality debt funds, such as short-duration funds.

All of this acted as a tailwind for the category and AMCs started lining up these funds. Between 2014 and 2016, eight new schemes were launched - almost half of the total credit-risk funds available now. In just a matter of these two years, the assets managed by these funds rose from Rs 16,000 crore to around Rs 55,000 crore by the end of 2016 - a rise of a whopping 244 per cent! Continuing its growth momentum, the fund's AUM further climbed to more than Rs 94,000 in the third quarter of CY2018. See the chart 'Credit-risk funds on high and low'.

Nevertheless, the subsequent period turned out to be a backflip for these funds, owing to the biggest debt crisis that hit the Indian financial industry and revealed several cracks in the way these funds were being managed. We are talking about the IL&FS debacle here (naam toh suna hi hoga!). The episode put a big question mark on credit-assessment practices as the NBFC, despite being the highest rated, defaulted on its obligations and it was only after the mishap in September 2018 that its rating was abruptly downgraded to default grade ('D') by rating agencies. The incident was followed by a series of defaults, downgrades (DHFL, Essel Group, Vodafone Idea, YES Bank, etc.) and resulting side-pocketing of portfolios, which cast a dark shadow on debt mutual funds, particularly credit-risk funds. So far, they account for 27 per cent of the entire segregated value of nearly Rs 6,000 crore, as covered in one of our earlier article series on side-pocketing.

Further, the closure of six yield-oriented Franklin schemes in April 2020 because of redemption pressure and liquidity issues acted as the final nail in the coffin. The entire saga well illustrates what could potentially happen with a significant allocation to low-rated securities when many investors turn up demanding their money back at a difficult time. While some funds were able to navigate well through all this mess, together as a set, the darker side of these funds came to light. Consequently, the category AUM has nosedived over the last three years, while the returns continue to trail. Check the chart 'Credit-risk funds vs short-duration funds'.

As a fun fact, credit-risk funds were called 'credit-opportunities funds' before the SEBI's categorisation in October 2017. And now you know why their names were misleading earlier! But have they learnt anything from all these past disasters? Are they safer now? We assess their investment case in the next part of this two-part article series.

You can read the next part here.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()