Anand Kumar

Anand Kumar

We, as Indians, have been traditionally good at saving money.

However, saving money in a bank account or a locker is only half the job.

To meaningfully benefit from the power of compounding, you need to invest that saved money in the right place.

At this point, you may feel proud to have invested in a fixed deposit (FD). But hold on. Let's take a quick detour.

The return illusion

Say you get the chance to work in your dream company.

But to join the place, you need to take a pay cut.

That doesn't sound like a great deal, right?

But what if it is happening to you in some form without you being aware of it?

Let's introduce you to the dark side of bank fixed deposits (FDs).

Around 15 years back - FD return rates looked quite good, considering they were safe too.

Cut to the present, the return rates have sunk; in fact, the rates have fallen steadily over the last few years.

The only constant is that FD rates have barely managed to beat inflation!

As a result, your wealth is actually eroding over time because inflation is killing your gains.

Let's explain how.

The perils of inflation

Inflation is a general increase in the prices of goods and services.

Let's take the example of a one-litre packet of Amul milk. It cost Rs 30 in 2010, and now, it costs more than double (Rs 63). That's inflation for you.

Put simply, inflation reduces the purchasing value of money.

Let's give you another example: India has almost always had a high-inflation economy. If you had Rs 1 lakh saved in your cash drawer in 2001, it would not be worth more than Rs 24,000 in 2023!

And the future is certainly no better. Inflation will keep reducing the value of Rs 1 lakh.

Let's come back to fixed deposits (FDs) now. Since FD return rates have barely matched India's average inflation rate of 6-7 per cent in the last 20 years, nobody has made it big by investing in them.

If you compare, investing in FD is similar to taking a pay cut to join your dream company.

So, what's the best solution for an intelligent investor?

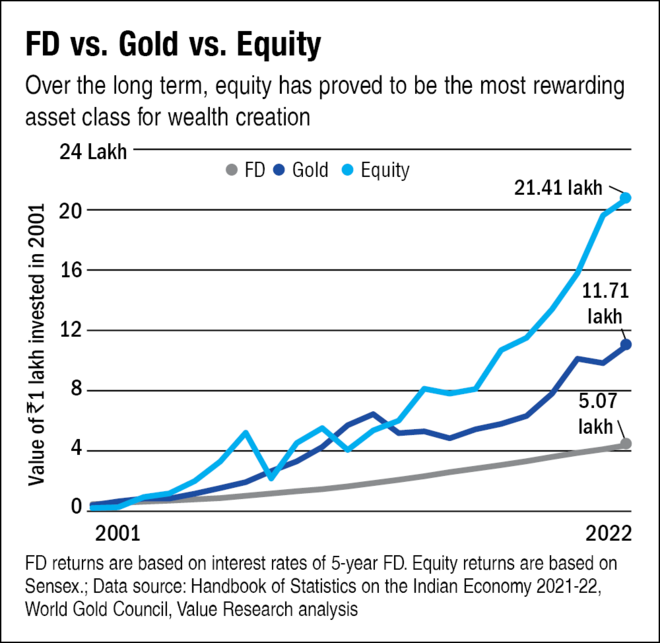

Say yes to equity

We must move beyond the comfort of assured returns provided by fixed-income investments and embrace equity, i.e., stocks.

Before you shut this page for thinking we have gone barking mad, consider this: equity has actually delivered higher returns than inflation over longer periods.

Aprajita Anushree

Aprajita Anushree

Yes, equity has outperformed gold too!

Remember how inflation destroyed the purchasing power of Rs 1 lakh in a cash drawer in 2001?

Investing in equity has the opposite effect on your money. If you had invested the same amount in Sensex (a basket of the 30-largest stocks in India), it would have grown to more than Rs 21 lakh by the end of 2022!

Think long-term

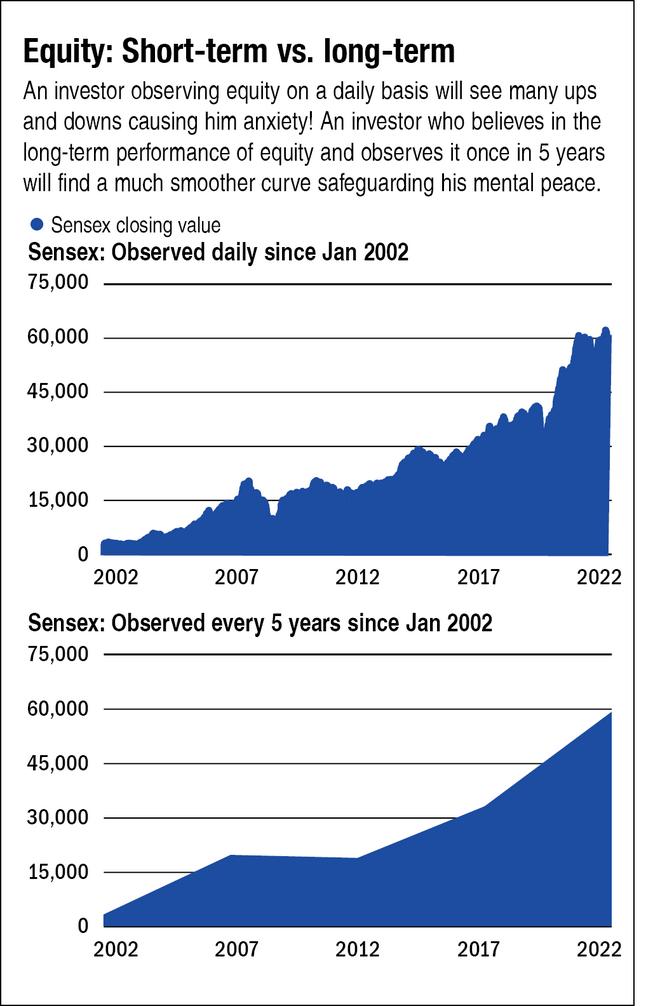

Sounds great, but what about the risk? Equity can even lose the money you invest.

True, equity can be very volatile over short periods.

However, the risk diminishes substantially over a longer time frame of five years or more.

Look at the Equity: Short-term vs long-term graph, which depicts the nature of equity markets.

Aprajita Anushree

Aprajita Anushree

The data clearly suggests that you can be confident of getting far better returns over a longer horizon than any fixed-income alternative.

Your confidence should increase further if you believe in India's growth story in the next 10 to 20 years. The faster India grows, the better it is for Indian stock markets.

How to invest in equity

There are two options at your disposal:

- Direct stock investin

- Mutual funds

While the end goal is the same, the approach is entirely different.

Direct stock investing is suitable for seasoned investors who track markets, understand businesses and find worthy stocks by themselves.

Mutual funds, on the other hand, are way more straightforward. Straightforward because you don't have the responsibility and pressure to choose your stocks; you allow a professional fund manager to do this for you.

This is primarily why mutual funds are suitable for both new and seasoned investors, who don't have the time to track markets and read lengthy business reports.

In the next chapter, we will address what mutual funds are in detail and the most common questions you may have.

This article was originally published on December 02, 2021, and last updated on July 20, 2023.

Ask Value Research ![]()