We all know investing is different from just saving. If we put our saved money somewhere where it will grow, then that's investing. However, when it comes to investing, there are so many possibilities that unless we find some way to make sense of them, it is hard to make a good decision.

However, let's not jump to classifying investments right away. Before we do that, we need to classify the needs that prompt us to invest in the first place. Now these can be extremely diverse. You could be saving for emergency medical funds which are usually required at a moment's notice. Or you could be investing for your retirement which is a few decades away. Or anything in between.

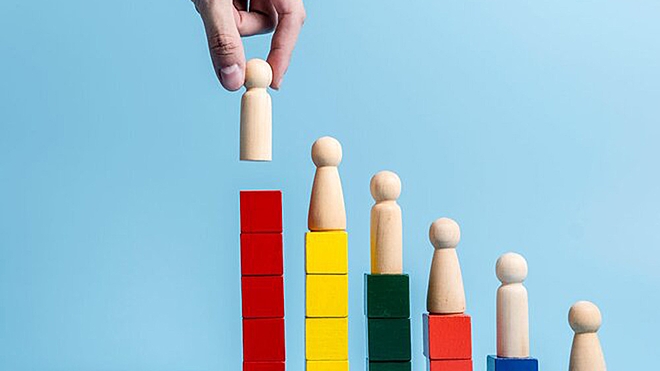

At Value Research, we have created a useful framework for thinking about these investment needs. We divide investment needs into four levels. Each level is more fundamental than the ones that come after it. Only once you have the needs of a lower level met should you move on to the next level. You may recognise this system as being based on the 'Hierarchy of Needs', a concept proposed by psychologist Abraham Maslow. Maslow's hierarchy deals with the whole gamut of needs, right from basic ones like food, clothing and shelter to the need for self-actualisation. His idea was that people aim to fulfil their higher needs only after the simpler ones are satisfied.

So here is Value Research's hierarchy of investing needs:

Level 1: Basic contingency funds

This is the money that you may need to handle a personal emergency. It should be available instantly, partly as physical cash and partly as funds that can be easily and immediately liquidated. Sweep-in fixed deposits and liquid funds are appropriate avenues for your emergency corpus, and online banking and ATMs make it relatively simple to get this organised.

Level 2: Term insurance

Calculate a realistic amount which allows your dependents to finance at least short and medium-term life goals if you were to drop dead or be struck with a debilitating injury or disease. You should have adequate term insurance before you think of any savings.

Level 3: Savings for foreseeable short-term goals

This is the money needed for expenses that you plan to make within the next two to three years. Almost all of this should be in minimal risk avenues that allow you to withdraw your funds when you need to.

Level 4: Savings for long-term foreseeable goals

This is similar to level 3, except the planned expenses are more than three to five years away. To meet needs at this level, you should be invested in equity and equity-backed investments like equity mutual funds.

It is easy to imagine many levels beyond this and really, the details matter much less than the concept. Depending on your circumstances, you may even modify some of these levels. For instance, if you do not have dependents, you do not need to buy life insurance. Or you may have enough income-producing assets to make insurance relatively less important.

The goal of this framework is not to help you decide how much to invest in each need. Rather, this system aims to prevent you from going to a higher level unless the lower one is fulfilled. So if you haven't put emergency cash in a savings account, then don't buy term insurance. Or if you don't have term insurance, then don't start putting away money for your daughter's college education just yet, and so on.

This article was originally published on July 29, 2021, and last updated on November 25, 2022.

Ask Value Research ![]()