Incorporated in 2008, this professionally managed company has built India's largest online platforms for insurance and lending products. PB Fintech owns two brands - Policybazaar (68.5 per cent of FY21 revenues) and Paisabazaar (31.5 per cent of revenues). Policybazaar, the company's flagship brand, was launched in 2008 in a bid to increase awareness of insurance and provide transparent and convenient access to buying insurance policies online. As per an F&S report, it is India's largest digital-insurance platform, accounting for 65.3 per cent of all digital-insurance sales in India by volume in FY20.

Paisabazaar, on the other hand, was launched in 2014 to provide easy access to various types of credits to its users. As per an F&S report, it is India's largest marketplace for digital-consumer credit, with a market share of 53.7 per cent based on disbursals in FY21. Paisabazaar is also widely used to access credit scores and as on June 30, 2021, a total of 22.5 million customers accessed their credit scores through this platform.

The company generates revenues through commissions by selling insurance and additional services to insurer partners, as well as commissions earned from its lending partners through Paisabazaar. Besides, it provides online marketing, consulting and technology services to its insurer and lending partners. Earlier only registered as a web aggregator, Policybazaar has recently received the license to work as a direct insurance broker, which will relax certain regulations related to the company's commissions and offline-sales ability.

Strengths

- The company has a very asset-light model, as it allows its customers to buy insurance policies and get access to credit facilities through its platform. The company itself does not underwrite any insurance or provide any kind of credit. So, it does not face any kind of credit risk.

- Leveraging its brands, the company has created transparent, user-friendly platforms, thereby enabling its customers to buy insurance and credit facilities with ease.

- The company has a long list of insurance and lending partners. As on September 30, 2021, a total of 48 insurance providers sold their products on Policybazaar, constituting 84.5 per cent of all licensed insurers in India. Similarly, Paisabazaar has partnerships with 56 large banks, NBFCs and fintech lenders.

- India has a highly underpenetrated insurance market and was among the lowest in terms of sum assured as a per cent of GDP in FY21. This ratio stands at 25 per cent in India, while it is 265 per cent in the USA and 95 per cent in China.

Risks

- The company has a history of incurring losses, which can continue to run in the future.

- The fintech industry, wherein the company operates, is relatively new and business models continue to evolve.

- The company's revenue is concentrated with the four largest partners who accounted for a32.8 per cent of its revenues in FY21.

- Commissions that the company charges from its insurer partners are regulated by the Insurance Regulatory and Development Authority (IRDAI). Any changes in the rate can adversely affect the company's business.

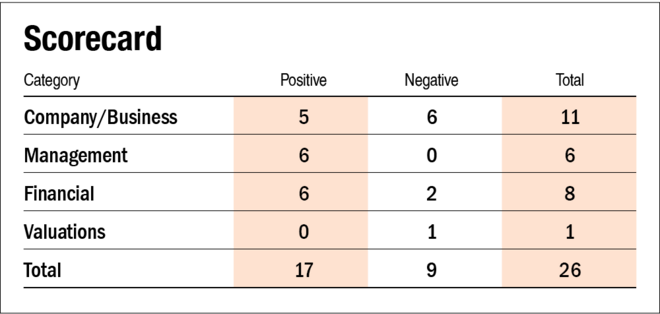

IPO questions

The company/business

1) Are the company's earnings before tax more than Rs 50 crore in the last 12 months?

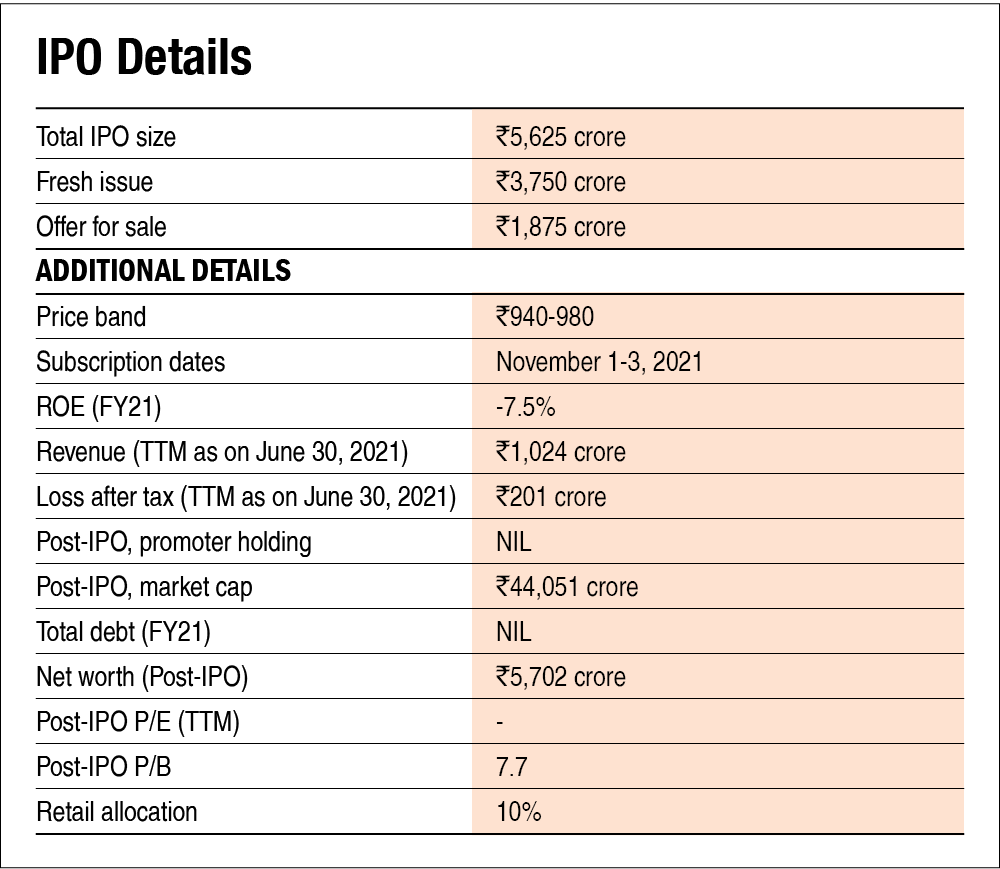

No, the company reported a loss of Rs 196 crore in the last 12 months ending June 30, 2021.

2) Will the company be able to scale up its business?

Yes, the company has an asset-light business model, which allows it to scale up its business faster than traditional businesses. COVID-19 has already propelled the demand for health insurance. Besides, the rapid digital adoption led by the growing penetration of the internet and smartphones is expected to increase the demand for digital insurance. Through its IPO proceeds, the company plans to invest significantly in marketing activities to promote its brands, attract new customers and increase its offline presence through retail stores.

3) Does the company have recognisable brand/s, truly valued by its customers?

Yes, its brands Policybazaar and Paisabazaar are highly recognised and popular brands in India in the digital insurance and lending sectors.

4) Does the company have high repeat customer usage?

Yes. Owing to the nature of the products offered by the company, renewals are quite common. So, the company enjoys long-term customer retention. As stated by the company, around 70 per cent of customers who bought health-insurance policies through its platform in 2014 have continued to renew their policy through the platform.

5) Does the company have a credible moat?

No. Although the company is a market leader in the digital-insurance space, it does not have a distinct credible moat to safeguard its business.

6) Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company's primary revenue source is the commissions it earned by selling insurance products. These commissions are regulated by the IRDAI. Therefore, any change in the maximum commissions charged can adversely affect its business.

7) Is the business of the company immune from easy replication by new players?

No. Since it is a technology-based company, its business model can be easily replicated.

8) Is the company's product able to withstand being easily substituted or outdated?

Yes, the company's products such as insurance policies and lending business cannot be substituted.

9) Are the customers of the company devoid of significant bargaining power?

Yes, as its customers are individuals, no one has significant bargaining power over the company.

10) Are the suppliers of the company devoid of significant bargaining power?

No, the company derives a significant portion of its revenue from a few major vendors. Also, insurers and lending partners can decide not to list their products on the company's platform and opt for direct selling.

11) Is the level of competition the company faces relatively low?

No, the company competes with other online independent insurance and credit-product providers, traditional offline insurance and credit companies and online direct-sales channels of insurance and credit companies.

Management

12) Do any of the company's founders still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than a 25 per cent stake in the company?

Yes, although the company is professionally managed, the company's founders will continue to hold a 5.1 per cent stake in the company, post-IPO.

13) Do the top three managers have more than 15 years of combined leadership at the company?

Yes, its CEO and founder Mr Yashish Dahiya has been associated with the company since 2008. Besides, Mr Naveen Kukreja, co-founder and CEO of Paisabazaar, has been associated with the company since 2014.

14) Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes, we have no reason to believe otherwise.

15) Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes, the company is free of any material litigation. However, a civil suit was filed against Mr Kaushik Dutta, a whole-time independent director, along with 127 others, by Satyam Computer Services in 2012 for the breaches of fiduciary, statutory and contractual obligations.

16) Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise.

17) Is the company free of promoter pledging of its shares?

Yes, since the company is professionally managed, it does not have any identifiable promoter.

Financials

18) Did the company generate a current and three-year average return on equity of more than 15 per cent and a return on capital of more than 18 per cent?

No, the company has been regularly incurring operating losses.

19) Was the company's operating cash flow positive during the three years?

No, the company has reported negative operating cash flows in the last three years.

20) Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes, the company's revenue grew at a rate of 34.2 per cent from FY19 to FY21.

21) Is the company's net debt-to-equity ratio less than one or is its interest-coverage ratio more than two?

Yes, the company was net-debt free as on June 30, 2021.

22) Is the company free from reliance on huge working capital for day-to-day affairs?

Yes, the company has a positive working capital and a working-capital cycle of around 30 days, within which, the company converts its sales into cash.

23) Can the company run its business without relying on external funding in the next three years?

Yes, the company has huge cash and cash equivalents of more than Rs 1,500 crore, along with a fresh issue of Rs 3,750 crore, which will be sufficient to run its platform businesses without relying on external funding.

24) Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes, the company is debt-free.

25) Is the company free from meaningful contingent liabilities?

Yes, the company has contingent liabilities of Rs 24.5 crore, which was 1.2 per cent of its equity as on June 30, 2021.

Stock/valuations

26) Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the company has been reporting negative operating earnings over the last three years.

27) Is the stock's price-to-earnings less than its peers' median level?

Not applicable. No other listed company is engaged in a similar business. Also, the company has reported negative earnings or losses in the last three years.

28) Is the stock's price-to-book value less than its peers' median level?

Not applicable. Post-IPO, the company's stock will trade at a P/B of 7.7 times.

Disclaimer: The authors may be an applicant in this Initial Public Offering.

Ask Value Research ![]()